Cryptocurrencies have become one of the most talked-about topics in the world of finance, with Bitcoin leading the charge since its creation in 2009. Over the years, cryptocurrencies have expanded far beyond being a speculative investment vehicle and have begun to play an increasingly important role in the realm of digital payments. As the world moves toward a more cashless and digital economy, cryptocurrencies are emerging as an alternative form of payment that offers numerous advantages over traditional systems.

In this article, we will explore the role of cryptocurrencies in digital payments, how they work, their advantages, the challenges they face, and what the future holds for them in the global payment ecosystem.

What Are Cryptocurrencies?

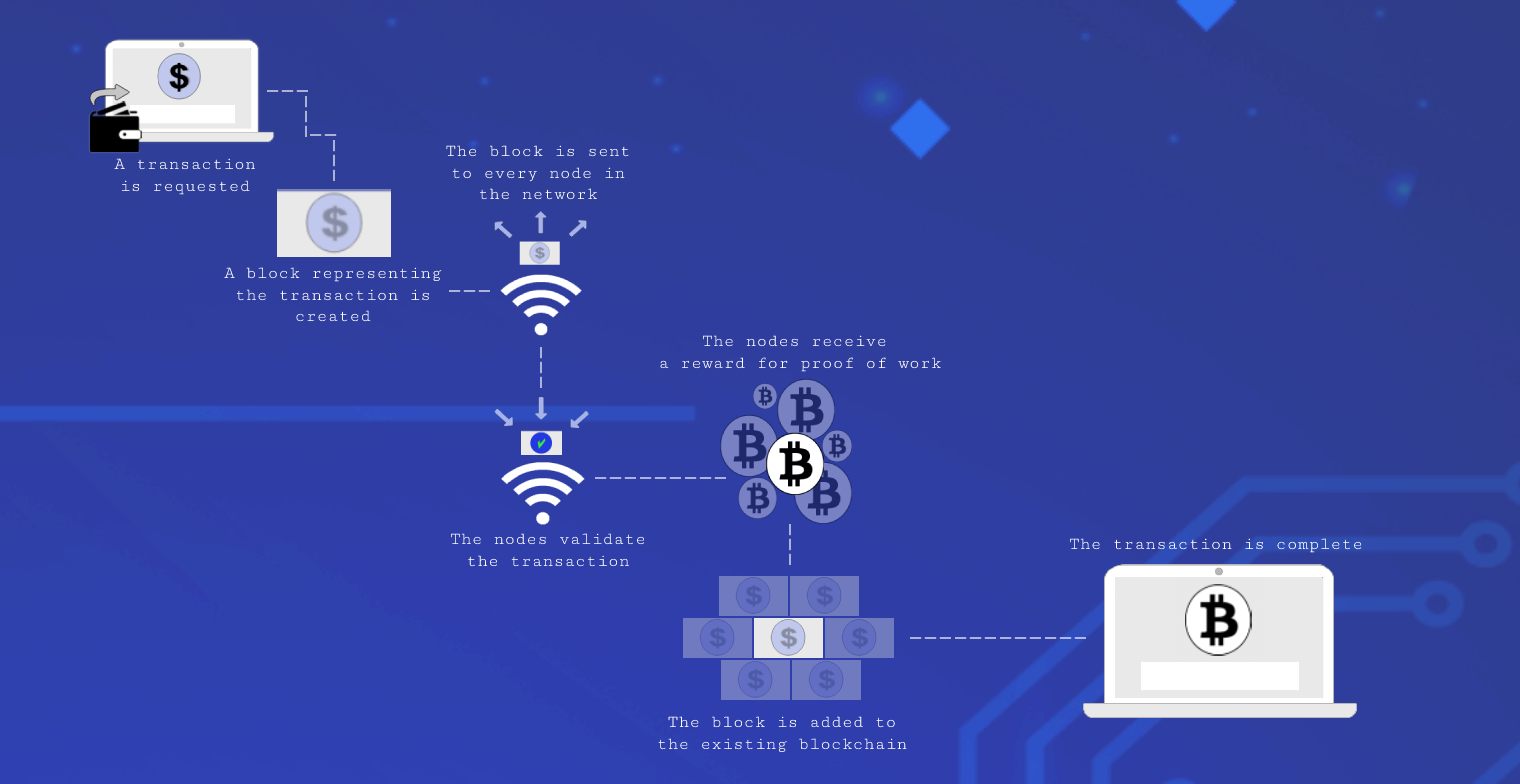

Before diving into how cryptocurrencies are used for digital payments, it’s important to understand what they are. Cryptocurrencies are digital or virtual currencies that use cryptography for security, making them difficult to counterfeit or double-spend. Unlike traditional currencies issued by central banks (fiat currencies like the US dollar or the euro), cryptocurrencies are typically decentralized and operate on a peer-to-peer network using blockchain technology.

Blockchain is the underlying technology behind most cryptocurrencies. It is a distributed ledger that records transactions across multiple computers, ensuring that the information is transparent, and secure, and cannot be altered retroactively without the consensus of the network.

Some of the most popular cryptocurrencies include:

Bitcoin (BTC): The first and most widely recognized cryptocurrency.

Ethereum (ETH): Known for its smart contract functionality.

Ripple (XRP): Focuses on fast and low-cost cross-border payments.

Litecoin (LTC): Designed as a lighter, faster version of Bitcoin.

Stablecoins: Cryptocurrencies pegged to the value of a fiat currency like the US dollar

The Role of Cryptocurrencies in Digital Payments

The rise of cryptocurrencies has brought about a new era of digital payments, where individuals, businesses, and even governments are exploring their potential. Here’s a closer look at how cryptocurrencies fit into the broader digital payment landscape:

Decentralization and Financial Inclusion

One of the key benefits of cryptocurrencies is their decentralized nature. Unlike traditional banking systems, which rely on central authorities such as banks and payment processors, cryptocurrencies operate on decentralized networks. This means that anyone with an internet connection can access these payment systems, regardless of their location or financial status.

In regions where access to banking infrastructure is limited or non-existent, cryptocurrencies offer a viable alternative. They can empower individuals in developing countries, where traditional banking services are often expensive or out of reach, to participate in the global economy. By providing an easy and cost-effective means to send and receive money, cryptocurrencies are contributing to greater financial inclusion.

Speed and Cost Efficiency

Traditional payment systems, especially cross-border transfers, often involve intermediaries such as banks and payment processors, which can lead to delays and high transaction fees. Cryptocurrencies, on the other hand, can streamline these processes. Payments made in cryptocurrencies, such as Bitcoin or Ethereum, are typically faster and cheaper than traditional methods.

For example, a cross-border transaction using a cryptocurrency can be completed in a matter of minutes, as opposed to several days with traditional banking systems. Additionally, cryptocurrencies can significantly reduce transaction fees, which are often a burden for businesses and consumers when using traditional payment methods like credit cards or wire transfers.

Transparency and Security

Cryptocurrencies offer a level of transparency that traditional payment systems cannot match. Every transaction is recorded on the blockchain, creating a permanent, immutable ledger that can be publicly verified. This not only enhances security but also provides businesses and consumers with a high degree of confidence in the system.

Furthermore, blockchain technology ensures that cryptocurrencies are secure and resistant to fraud. The decentralized nature of cryptocurrencies makes it difficult for malicious actors to manipulate or alter transaction records, which is a significant advantage over centralized systems prone to hacking or errors.

Privacy and Anonymity

While cryptocurrencies are transparent, they also offer enhanced privacy compared to traditional payment systems. Transactions on the blockchain do not require users to reveal personal information such as names, addresses, or account details. Instead, users transact using cryptographic addresses, which provides a degree of anonymity.

For individuals who value privacy, cryptocurrencies can be an attractive option. However, it’s worth noting that certain cryptocurrencies, such as Monero and Zcash, are designed specifically to enhance privacy and anonymity by using advanced cryptographic techniques to obfuscate transaction details.

Advantages of Cryptocurrencies for Digital Payments

The rise of cryptocurrencies is fueled by their potential to offer various benefits over traditional payment methods. Let’s explore some of these advantages in more detail:

Lower Transaction Costs

Traditional payment methods, such as credit cards or wire transfers, can be costly due to the fees charged by banks and payment processors. These fees can add up, especially for businesses that rely on international payments. Cryptocurrencies significantly reduce these costs by eliminating intermediaries.

For example, Bitcoin transactions typically have lower fees compared to credit card payments or bank wire transfers. Cryptocurrencies like Ripple (XRP) and Stellar (XLM) are specifically designed for fast and low-cost cross-border payments, making them an ideal choice for businesses that need to send money internationally.

Security and Fraud Prevention

Cryptocurrency transactions are secured by cryptographic algorithms that make them virtually impossible to tamper with. Once a transaction is recorded on the blockchain, it is permanent and cannot be altered, providing a high level of security. This makes cryptocurrencies less susceptible to fraud compared to traditional payment methods, where chargebacks and fraud are common.

The decentralized nature of cryptocurrencies also means that there is no central authority that can be compromised or hacked. This enhances the overall security of the payment system.

Accessibility and Inclusion

Cryptocurrencies have the potential to bring financial services to underserved populations. In countries where access to traditional banking is limited, cryptocurrencies provide an alternative means for individuals to store, send, and receive money. This financial inclusion is especially important for those who do not have access to traditional banking infrastructure but have access to mobile phones and the Internet.

Cross-Border Payments

Cross-border payments have historically been slow and expensive due to the involvement of multiple intermediaries, currency conversion, and high transaction fees. Cryptocurrencies, particularly stablecoins and digital assets like Ripple (XRP), can facilitate faster and cheaper cross-border payments by bypassing intermediaries.

For businesses that operate globally, cryptocurrencies can significantly reduce the costs and time associated with sending money internationally. This is particularly beneficial for small and medium-sized enterprises (SMEs) that need to manage cross-border payments efficiently.

Challenges Facing Cryptocurrencies in Digital Payments

Despite their many advantages, cryptocurrencies face several challenges that hinder their widespread adoption as a mainstream form of payment.

Volatility

One of the biggest challenges facing cryptocurrencies is their price volatility. Cryptocurrencies, particularly Bitcoin and Ethereum, have been known to experience dramatic price fluctuations. While this volatility creates opportunities for investors, it poses a significant challenge for businesses looking to use cryptocurrencies for everyday transactions.

If the value of a cryptocurrency can fluctuate by 10% or more in a single day, it becomes risky for merchants to accept it as payment. The lack of price stability makes it difficult for businesses to set prices and for customers to use cryptocurrencies as a reliable store of value.

Regulatory Uncertainty

Cryptocurrency regulation varies significantly from one country to another. While some countries have embraced cryptocurrencies and established clear regulations, others have banned or heavily restricted their use. The lack of consistent regulatory frameworks creates uncertainty for businesses and consumers, making it difficult for cryptocurrencies to gain mainstream acceptance.

Governments are still figuring out how to regulate cryptocurrencies, especially regarding taxation, anti-money laundering (AML), and combating the financing of terrorism (CFT). Until these regulatory challenges are resolved, cryptocurrencies may face significant hurdles to widespread adoption.

Scalability

Another challenge for cryptocurrencies, particularly Bitcoin and Ethereum, is scalability. As the number of transactions on a blockchain network increases, the speed and efficiency of processing these transactions can slow down. This is because blockchains have limited block sizes and transaction throughput.

Several solutions are being explored to address scalability, such as the development of second-layer solutions like the Lightning Network for Bitcoin and Ethereum’s transition to Ethereum 2.0. However, until these scalability issues are resolved, cryptocurrencies may face challenges in handling a large volume of transactions.

Lack of Merchant Adoption

While cryptocurrencies have gained traction in certain sectors, their adoption as a payment method by merchant’s remains limited. Many businesses are still hesitant to accept cryptocurrencies due to concerns about volatility, regulatory uncertainty, and the technical challenges associated with integrating cryptocurrency payments into existing payment systems.

However, as awareness grows and solutions are developed to address these challenges, it’s likely that more merchants will begin to accept cryptocurrencies as a legitimate form of payment.

The Future of Cryptocurrencies in Digital Payments

The future of cryptocurrencies in digital payments looks promising, but there are still several hurdles to overcome. As blockchain technology matures and regulatory frameworks are established, cryptocurrencies are expected to play an increasingly important role in the global payment ecosystem.

Some of the potential developments include:

Integration with traditional financial systems: As cryptocurrencies become more widely accepted, we may see increased integration between traditional payment networks and blockchain-based systems. This could create a hybrid system where cryptocurrencies coexist with fiat currencies.

Stablecoins and Central Bank Digital Currencies (CBDCs): Stablecoins, which are pegged to the value of fiat currencies, offer a way to reduce volatility and improve the usability of cryptocurrencies for everyday payments. Additionally, many governments are exploring the development of their own digital currencies (CBDCs), which could further legitimize the use of digital payments.

Improved scalability and transaction speeds: As blockchain technology evolves, scalability and transaction speeds are expected to improve, making cryptocurrencies more viable for high-volume payments.

Conclusion

Cryptocurrencies are revolutionizing digital payments by offering a decentralized, secure, and cost-efficient alternative to traditional payment systems. While there are challenges to their widespread adoption, the benefits they bring to financial inclusion, cross-border payments, and security make them an attractive option for the future of payments.

As technology continues to evolve, cryptocurrencies are likely to become an integral part of the global financial ecosystem. Whether you are a consumer, business owner, or investor, it’s clear that cryptocurrencies have a significant role to play in shaping the future of digital payments.