The world of finance is moving fast, and India is leading the way with new ideas. To make sure these ideas are safe, the government uses a special tool called a regulatory sandbox. This is a controlled space where fintechs can test their new products with real users. For instance, testing how to pay without internet is a top priority right now. Because the rules are flexible in this space, fintechs can learn quickly without breaking the law. In short, these sandboxes are the best way to build the future of Indian money.

Why Sandboxes Matter for New Ideas

Creating a new app for a billion people is a very hard task. Traditional rules are often too strict for tiny startups with big dreams. Consequently, many fintechs worry about failing before they even start. This is because a sandbox provides a safety net for everyone involved. Furthermore, it allows the regulator to see how new tech works in the real world. Therefore, the sandbox approach helps fintechs grow while keeping the whole system stable and secure.

Another big hurdle is the high cost of following every single rule. For instance, a small team might not have the money for a full banking license. If they can test in a sandbox first, they can prove their idea works. Thus, the government encourages fintechs to join these programs to spark more competition. A smart sandbox strategy solves the problem of slow innovation by moving at the speed of tech. This keeps India ahead in the global race for digital dominance.

Opportunities for Growth in India

Testing offline payments is a vital tool for rural success. In many parts of India, the internet is not always strong or fast. Because fintechs are building tools that work without a signal, they can reach the last mile. Furthermore, these tests show if a product is easy enough for everyone to use. This means a farmer in a remote village can pay for seeds just as easily as a city worker. In short, India wins when fintechs focus on solving real-world problems for every citizen.

Access to expert guidance is another great benefit of the sandbox. Instead of guessing the rules, firms talk directly to the central bank. Because this relationship is open and honest, it builds a lot of trust. Furthermore, a successful test in a sandbox acts like a badge of honor for fintechs looking for investors. This means they can raise money faster and expand their reach across the country. Therefore, the sandbox is more than just a test; it is a launchpad for the next big thing.

Risks and Challenges in the Sandbox

Safety is the most important part of any financial test. Even in a controlled space, things can go wrong with real money. Luckily, new AI tools are great at spotting risks before they become big problems. If a test shows a security gap, the system can be paused or fixed fast. This keeps the users and the fintechs safe from hackers and fraud. Because the regulators are watching closely, they can stop any bad behavior instantly. Thus, the sandbox stays a secure place for everyone.

Additionally, some people worry about what happens after the test ends. Moving from a sandbox to the real market is a big jump for most fintechs today. It requires more money, more staff, and a much bigger focus on safety. When a firm leaves the sandbox, the rules become much harder to follow. Therefore, the risk of a mistake is higher once the safety net is gone. This is why the journey from the sandbox to the real world must be planned very carefully. Finally, clear rules ensure that the transition is smooth for the users.

The Big Future of Indian Innovation

We are only at the start of a massive shift in how we handle money. Soon, every village in India will have access to fast and safe digital tools. This means we will see a huge boost in local businesses and family savings. Instead of a hard process, we get a tailored world of easy trade for all. Forward-thinking fintechs make every transaction feel like a step toward a digital India. It is the best way to build a strong economy in 2026. If you want to lead, you must join these sandbox programs now. In conclusion, the right balance of rules and freedom will change India forever.

Frequently Asked Questions

1. What is a regulatory sandbox for fintechs?

It is a safe testing ground where new financial tools are checked by regulators before a full launch.

2. Why is India focusing on offline payments?

Because many rural areas have poor internet, and offline tools ensure everyone can join the digital economy.

3. Is my money safe during a sandbox test?

Yes, regulators set strict limits and protections to ensure no user loses their money during the trial.

4. How long does a sandbox test usually last?

Most tests in India last between six to nine months, depending on how complex the product is.

5. Can any startup join the sandbox?

Most fintechs can apply, but they must show their idea is new, safe, and solves a real problem for India.

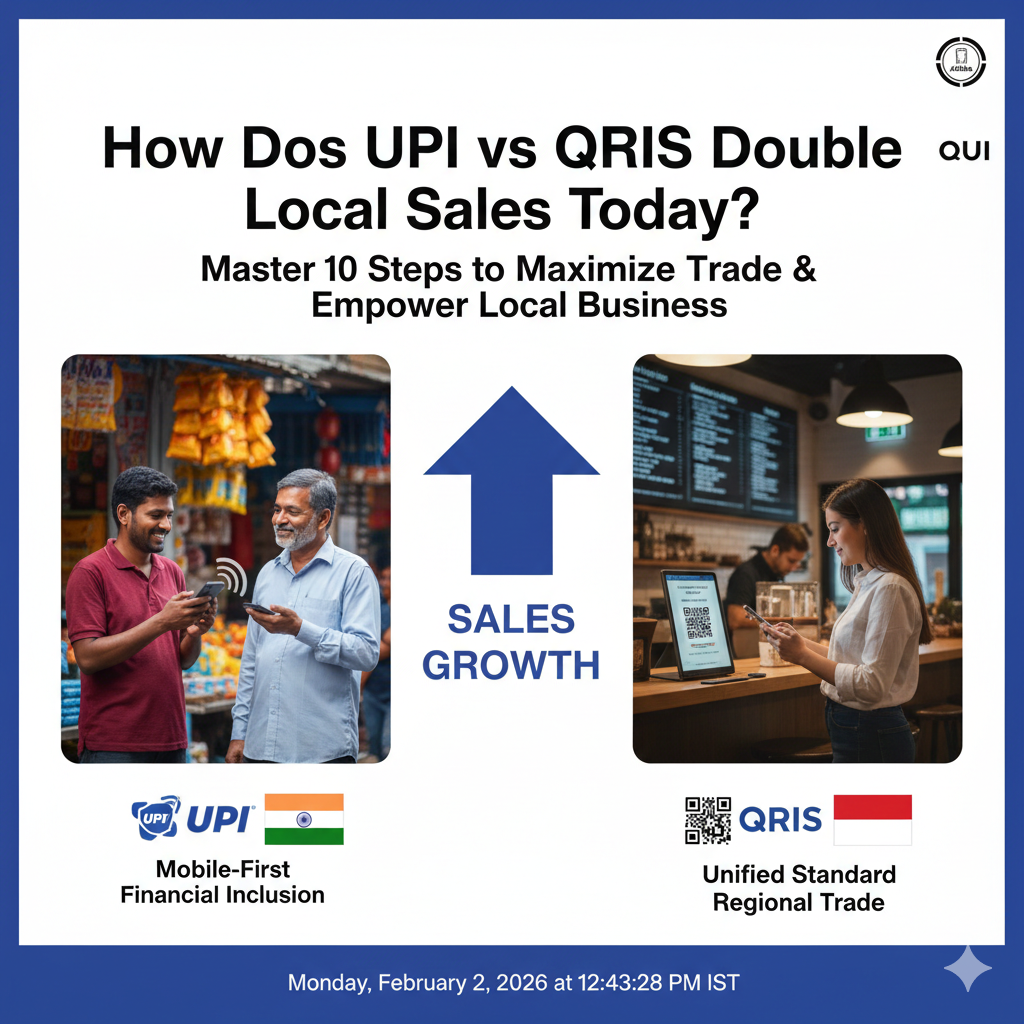

I’ve heard it a thousand times. A nation relies only on one foreign credit card firm. And yet, their local shops pay high fees. Usually, that is just a polite way of saying the country has lost its own power. Also, old bank moves take a long time. They involve too many middle men. If you build a new market on old tracks, you are building a ghost town.

In fact, a system where local tracks handle 80% of deals is worth much more. Furthermore, the biggest cost in 2026 is the lack of links between close nations. This happens when people must carry cash or pay high fees. This path creates a big gap. Because of this, users want a fast and easy way to pay.

The solution lies in a smart way to keep your money power. This turns a national rule into a solid sales tool. This isn’t just a tech shift. Instead, it is a big plan. This helps every person pay in a safe way. Once you use these rules, you will see your local market grow.

1. UPI: The Best Way to Join the Bank

If you aren’t looking at the UPI growth data, you are flying blind. Specifically, India’s UPI has won more of the market for three months in a row. You need to know why this tool works so well. For example, was it the low cost or the ease of use? Smart leaders use the UPI path to see how to reach far away areas. Then, they make mobile plans for their own folks.

Moreover, smart plans allow for a steady gain in the market. This is because they focus on a good user path. By using a top-tier plan, you help your local banks win. This leads to steady gains. It sounds simple. However, most lands are too busy guessing to look at the UPI success.

2. QRIS: Linking Asian Shops Through Scans

The move to regional QR tools is happening faster than we thought. While old tools are slow, QRIS adds cross-border links through one rule. These rules use logic to link many bank nets. These rules act like a smart helper for regional trade.

However, one-country tools are not enough for a big change. The most top-tier stage is a system for many lands. These nets handle tasks like live money swaps. These tools help many banks work as one. Consequently, they act as a smart brain for the whole Asian area.

3. Digital Euro: Keeping Europe’s Money Power

To build smart bank tools, you should not have to glue poor parts together. The Digital Euro aims to use one public coin. Specifically, this uses Europe’s strength to give safe answers to market moves. This means a person can travel with their full data ready to go.

Additionally, think of a case where your phone wallet knows your local spot. It uses safe data to help you buy things fast. This base ensures that your responses to global stress stay strong. Therefore, it stops the friction that slows down your best shops. It helps them finish big deals with fewer errors.

4. The 80/20 Rule for National Payments

If your land spends all its time on foreign nets, you have no time for local growth. You must follow an 80/20 rule. Thus, use local tracks to handle 80% of daily buys. This includes food or bus rides. This leaves the 20% of big global moves to top-tier firms.

Using fast moves helps shops stay on track without cash. AI can even set up fast replies based on simple talk. This allows your shops to work in a flow. They do not have to switch between many tools. This leads to much faster growth.

5. How to Track Your Money Success

If your bank talks about total sales but not local ownership, you need a new plan. Those are vanity marks that hide a weak spot. You can have many deals but no real power in the bank. To know if you are winning, you must track the “Dirty Four”:

Local Ratio: First, how many of your deals stay on your own tracks?

Shop Cost: Next, what is the total fee for every single scan?

Fast Speed: Then, for every coin paid, how fast does it reach the bank?

User Trust: Finally, when phone use grows, does your poor group get help?

Conclusion

How to win the money power race? It shifts from a secret to a system when you pick your goals well. You must set clear goals for the bank. Also, track gains with care using local data. Repeat this for 90 days. Then, growth becomes steady. This helps you spend your budget with trust.

Key Takeaways

First, payment sovereignty helps a nation control its own money because it removes the need for foreign tools.

Therefore, systems like UPI and QRIS serve as a bridge for trade and peace.

Specifically, the Digital Euro wants to give a public way to pay across all of Europe.

Furthermore, the QRIS model is growing fast to link Asian markets through easy scans.

Consequently, these tools allow small shops to take international money while they boost local sales.

In fact, India’s UPI has seen huge growth by making mobile phones the main way to join the bank.

For instance, having one set of rules helps lower the cost of every deal for the user.

Thus, using fast settlement stops the need for slow and very pricey old bank wires.

In addition, using live exchange rates builds quick trust when you travel to other lands.

Finally, keeping data local keeps your money safe and follows all your own laws.

FAQs

Q1: Can small lands afford their own pay tools?

Ans. Yes, tools like QRIS offer low-cost rules that work well for everyone.

Q2: How long before a new tool sees real growth?

Ans. Most systems see real gains and more users within 60 to 90 days of the start.

Q3: Is it better to focus on home use or foreign links?

Ans. Good local tracks work much better than relying on others in every test.

Q4: Will a Digital Euro take away my cash?

Ans. No, but it will act like a safe digital helper for all your phone buys.

Q5: What is the biggest risk for a big pay net?

Ans. Errors or bad data silos can be very bad, so make sure your tool has good backups.

You must watch how the world of digital money is merging today. Therefore, you should learn about PayPal and UPI integration and its global impact. Truly, sending money across borders used to be a very slow process. Consequently, you can enjoy a future where international cash moves as fast as a text.

Many people think that global banks will always charge very high fees. But, the reality is that new tech links are making payments much cheaper. Always remember, a fast payment path is a strong signal for any search engine. This ensures that your brand stays modern and your global customers stay very happy. This approach requires you to understand how these two giants work together. It helps you build a much more agile sales plan for the long term. It makes your daily international business feel much more secure and very effective.

Why This Integration is a Massive Deal

First, you must understand the scale of these two payment systems in 2026. Why is a link between PayPal and UPI such a big win for everyone? Clearly, PayPal dominates global trade while UPI is the king of instant cash in India. Therefore, linking them creates a bridge for billions of people to trade.

The Benefits of Linking PayPal with UPI

Here are several reasons why this link is a game-changer for you:

Speed: You get your international money in seconds instead of many days.

Simplicity: You can use your mobile phone to pay global sellers instantly.

Lower Cost: The integration removes many middle-man fees for every transfer.

Security: You get the protection of PayPal with the ease of a UPI scan.

Reach: Indian freelancers can now sell to the whole world much easier.

Transparency: You see the exact exchange rate before you click send today.

Truly, this link is about making the world feel like one single market. But, you must also see how this helps small creators grow their reach. This keeps your business competitive and prevents any loss of global sales. It creates a very professional and high standard for your digital store.

How the New Payment Bridge Works

So, how does the money actually travel from a US bank to an Indian app? Truly, the system uses smart digital codes to swap currencies in real-time. Consequently, you should imagine a fast lane for cash that never hits a red light. It acts as a direct link for seamless trade between different nations in 2026.

The Technology of Instant Global Cash

Here is how PayPal and UPI talk to each other right now:

Unified Interface: PayPal adds a UPI option directly inside its mobile app.

Real-Time Forex: The system picks the best exchange rate in a split second.

Virtual IDs: You use your simple UPI handle to receive global payments.

Instant Alerts: Both the sender and receiver get a message the moment it clears.

Encrypted Paths: Top-tier security protects your bank data during the swap.

Auto-Settlement: The money lands in your local bank account without extra steps.

Trust Rankings: Using modern payment links helps you keep a high search rank.

Furthermore, this improves your search engine performance by showing your site is up to date. It makes your company look very tech-savvy and ready for 2026 growth. This ensures that your valuable time is not spent chasing missing wire transfers. It creates a very fast and clear path for your professional global success.

Impact on Freelancers and E-commerce

The third phase involves looking at who gains the most from this new tech. Clearly, small business owners and digital workers will see a huge benefit today. Therefore, you should update your payment settings to include these new options.

Growing Your Brand with Better Payments

Firstly, a freelancer in India can now accept a payment from London instantly. This allows you to take on more work without worrying about high bank fees. Secondly, e-commerce stores can offer “Scan and Pay” to their international buyers in 2026.

Furthermore, you can pay for global software or tools using your local UPI balance. Also, use transition words in your invoices to keep them very clear for clients. Lastly, remember that a smooth payment flow helps your search engine authority and trust. Truly, this integration is the best tool for anyone working across borders. It allows you to focus on your craft while the money flows automatically. This is why top digital nomads are so excited about this new era.

Setting Up Your Global Payment Shield

The fourth phase is where you ensure your new payment links are safe. Clearly, you must protect your hard-earned money from digital thieves in 2026. Therefore, you must use strong security habits with your PayPal and UPI accounts.

Staying Safe in the World of Instant Money

Firstly, turn on two-step verification for both your PayPal and your banking app. This helps you stop any unauthorized access to your funds right away. Secondly, never share your UPI PIN or your PayPal password with anyone.

Furthermore, only send money to people or brands that you truly trust online. Also, use your data to track every transaction and report any errors fast. Lastly, check your search engine ranking to see if site safety helps your traffic. Truly, a safe payment path is a journey that leads to a much stronger brand. It turns a complex task into a series of smart, secure wins for your team. This ensures your business stays strong while others face digital risks.

Leading the Global Payment Wave

Finalizing your plan requires you to stay ahead of new fintech trends. It needs you to review your payment options and update your site every year. Clearly, being a leader in payments is a team effort in 2026. Therefore, follow these simple tips to keep your brand fresh and very fast.

Simple Tips for International Payment Success

Firstly, display the PayPal and UPI logos clearly on your checkout page. This helps your customers feel safe and ready to buy from you today. Secondly, offer a small discount for users who try the new instant payment path.

Furthermore, use transition words in your customer emails to explain the new speed. Also, remind your team that fast payments help the company earn more trust. Lastly, check your search engine data to see if speed helps your web traffic grow. Truly, a fast path is a journey that leads to a much better brand in 2026. It builds a path of innovation that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: Can I use UPI to send money to a US PayPal account?

Yes, the 2026 integration allows you to initiate payments via UPI to global PayPal users.

Q2: Are the fees lower than a standard bank wire?

Typically, yes, as the digital link removes several layers of traditional banking costs.

Q3: How fast does the money arrive in my account?

Most transactions through this bridge happen in real-time or within a few minutes.

Q4: Do I need a special app for this integration?

No, you just need the updated version of the PayPal app and a valid UPI ID.

Q5: Does offering UPI and PayPal help my SEO?

Yes, providing trusted and fast payment options improves user signals that search engines value.

You must watch how the world moves money in new ways today. Therefore, you should learn about India’s UPI expansion across the globe. Truly, the old rule of credit cards is facing a very big challenge. Consequently, you can stay ahead by knowing how this mobile system changes global trade for 2026.

Many people think that Visa and Mastercard will always lead the world. But, the reality is that mobile QR codes are taking over many markets. Always remember, a fast payment path is a strong signal for any search engine. This ensures that your brand stays modern and your customers stay very happy. This approach requires you to look at how instant payments lower your daily costs. It helps you build a much more resilient financial plan for the long term. It makes your daily international sales feel much more secure and very effective.

Phase 1: The Fast Rise of Instant Mobile Payments

First, you must understand why UPI is growing so fast in 2026. Why do millions of people prefer a phone scan over a plastic card? Clearly, UPI offers a direct link between bank accounts without any middle steps. Therefore, it makes every transaction feel instant and very simple for everyone involved.

Why UPI Is Gaining Ground on Card Giants

Here are several reasons why UPI is a global threat to cards:

Zero Merchant Fees: Small shops keep more of their money with every sale.

Instant Settlement: You get your cash right away instead of waiting for days.

No Plastic Needed: Your phone is the only tool you need to pay for goods.

Open Architecture: Any bank or app can join the network to help it grow.

High Security: It uses two-factor codes for every single scan today.

Offline Success: New tech allows UPI to work even without a strong signal.

Search Engine Trust: Fast sales help your site earn a better trust score.

Truly, these benefits show why India is exporting this tech to other nations. But, you must also see how Visa and Mastercard are reacting to this shift. This keeps your business flexible and prevents any sudden loss of payment options. It creates a very high and professional standard for your digital store.

Phase 2: UPI’s Global Footprint in 2026

So, where can you actually use UPI outside of India right now? Truly, the network is reaching into Europe, Asia, and the Middle East today. Consequently, you should watch for UPI signs in major cities around the world. It acts as a new bridge for global travel and digital commerce.

Countries Embracing India’s Payment Tech

Here is how UPI is expanding its reach in 2026:

Southeast Asia: Nations like Singapore and Malaysia now link to UPI fast.

The Middle East: You can pay with UPI in shops across the UAE and Qatar.

Europe: France and the UK are testing UPI for tourism and small trade.

Africa: Many nations use UPI tech to build their own local systems today.

Nepal and Bhutan: These neighbors were the first to adopt the full system.

Sri Lanka: UPI helps the local economy by making tourism payments easy.

Trust Rankings: Global reach helps your brand gain better search engine authority.

Furthermore, this improves your search engine performance by showing your global readiness. It makes your company look very smart and ready for 2026 market shifts. This ensures that you can take payments from a much wider pool of global fans. It creates a very fast and clear path for your international growth.

Phase 3: Can UPI Truly Replace Visa and Mastercard?

The third phase involves looking at the hurdles that UPI must still jump. Clearly, Visa and Mastercard have been the world leaders for over fifty years. Therefore, UPI must prove it can handle the world’s biggest and most complex deals.

The Challenges of Overtaking the Card Giants

Firstly, cards offer credit lines that UPI does not yet provide to everyone. This allows users to “buy now and pay later” with a simple swipe. Secondly, the card giants have a massive network of legal and fraud protection.

Furthermore, many Western nations still rely on old bank systems that move slowly. Also, Visa and Mastercard are launching their own “pay by bank” tools in 2026. Lastly, remember that a mix of tools helps your search engine trust and user speed. Truly, UPI is a great rival, but cards will not disappear any time soon. It allows you to offer more ways to pay, which is always good for your brand. This is why top merchants keep both cards and QR codes at their checkout.

Phase 4: Adapting Your Store for the UPI Era

The fourth phase is where you prepare your own business for these new tools. Clearly, you want to be where your customers are spending their money today. Therefore, you must add mobile and QR payment options to your website and shop.

How to Join the Global Payment Shift

Firstly, check if your payment gateway supports UPI or other instant bank tools. This helps you reach millions of new buyers from India and beyond in 2026. Secondly, use simple QR codes at your physical shop to lower your card fees.

Furthermore, train your staff on how to verify a mobile payment in seconds. Also, use transition words in your shipping guides to explain your new pay options. Lastly, check your search engine ranking to see if new pay tools help your traffic. Truly, a flexible shop is your best tool for success in the digital world. It turns a complex shift into a series of smart, profitable wins for you. This ensures your business stays running while the giants fight for the lead.

Best Practices: Choosing the Right Global Strategy

Finalizing your plan requires you to stay balanced in your payment choices. It needs you to offer the safety of cards and the speed of mobile apps. Clearly, your customers want a mix of trust and ease when they shop with you. Therefore, follow these simple tips to keep your global payments healthy and fast.

Simple Tips for Modern Payment Success

Firstly, always keep your card options for customers who want to earn rewards. This helps you keep your big spenders happy and coming back for more today. Secondly, use UPI for small, fast sales to keep your transaction costs very low.

Furthermore, use transition words in your invoices to make them easy for fans to read. Also, check the news for any new UPI links in your target markets for 2026. Lastly, check your search engine data to see if pay speed helps your sales. Truly, a smart path is a journey that leads to a much better brand. It builds a path of wealth that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: Is UPI safer than a credit card?

Both are safe, but UPI uses your bank’s own security and does not share your card number.

Q2: Does UPI work for international travel?

Yes, many countries now allow you to scan a QR code using your Indian UPI app in 2026.

Q3: Why do shops prefer UPI over Visa?

Shops prefer UPI because it usually has no fees, so they keep 100% of the sale price.

Q4: Can I get a refund on a UPI payment?

Yes, but the process depends on the shop’s own policy rather than a card bank’s rules.

Q5: How does UPI expansion help my SEO?

Offering modern, global payment tools improves user experience and builds your site’s trust.

You must understand the new ways the world moves money today. Therefore, you should learn about the battle between SWIFT, CIPS, and UPI. Truly, the old ways of sending cash across borders are changing very fast. Consequently, you can stay ahead by knowing which system works best for your global trade.

Many people think that all international bank transfers are exactly the same. But, the reality is that each system has its own rules and goals in 2026. Always remember, a fast payment system is a strong signal for any search engine. This ensures that your brand stays reliable and your global partners stay happy. This approach requires you to look at speed, cost, and political safety. It helps you build a much more resilient financial plan for the long term. It makes your daily international sales feel much more secure and very effective.

Phase 1: The Global Standard of SWIFT

First, you must look at SWIFT because it is the biggest network today. Why has it been the leader of global finance for so many decades? Clearly, it connects over 11,000 banks in almost every country on earth. Therefore, most businesses still rely on it for large, secure transfers every day.

Why SWIFT Stays at the Top of Finance

Here are several reasons why SWIFT remains a powerhouse in 2026:

Massive Reach: You can send money to almost any corner of the globe.

High Security: It uses the best tech to keep your data and cash very safe.

New Speed: The gpi system now makes many transfers happen in minutes.

Global Trust: Banks everywhere know and use this system without any doubt.

Shared Standards: It uses a common language that all bank systems understand.

Transparency: You can track your money like a package in the mail today.

Search Engine Data: Stable SWIFT flows help your business earn trust scores.

Truly, SWIFT is a very solid choice for most of your corporate needs. But, you must also consider the fees and the time it takes to clear. This keeps your costs in check and prevents any delays in your supply chain. It creates a very professional and high standard for your global trade.

Phase 2: The Rising Power of CIPS in China

So, what happens when a nation wants its own way to move money? Truly, China created CIPS to help the yuan become a global currency fast. Consequently, you should watch this system if you do a lot of business in Asia. It acts as an alternative path that does not always rely on Western banks.

How CIPS Changes the Payment Game

Here is how CIPS works differently from the old systems:

Direct Yuan Trade: It allows you to pay for goods in yuan without a middle step.

Fast Clearing: It offers real-time settlement for many types of trade deals.

Extended Hours: It stays open longer to match the working day in many zones.

Lower Costs: Using CIPS can be cheaper for firms that trade with China today.

Independent Path: It provides a safety net if other networks face political noise.

Direct Access: More banks in Europe and Africa are joining the system right now.

Trust Levels: Using local systems improves your search engine authority in Asia.

Furthermore, this improves your search engine performance by showing your reach in the East. It makes your company look very modern and ready for 2026 global shifts. This ensures that you have a backup plan for your most important trade routes. It creates a very fast and clear path for your international growth.

Phase 3: The Rapid Growth of UPI and QR Payments

The third phase involves a much newer and faster way to pay for things. Clearly, India’s UPI is changing how people and small firms send money today. Therefore, the link between UPI and other nations is a huge trend to watch.

Why UPI Is the Future of Small Cross-Border Payments

Firstly, UPI is very fast and works on your mobile phone in seconds. This allows you to pay for a meal or a small service with just a QR code. Secondly, it is very cheap because it skips many of the old bank fees.

Furthermore, many nations are now linking their own systems to the UPI network. Also, it allows for instant currency swaps at the moment of the sale today. Lastly, remember that fast mobile payments help your search engine trust and local SEO. Truly, UPI is the best tool for the small, daily needs of your global team. It allows you to move small amounts of cash without any of the old bank stress. This is why so many travelers and small shops love it in 2026.

Phase 4: Comparing the Three Systems for Your Business

The fourth phase is where you pick the right tool for your specific goal. Clearly, one system might be better for a factory order while another fits a small fee. Therefore, you must compare speed, cost, and reach for every single payment.

A Quick Look at the Payment Leaders

Firstly, use SWIFT for large, high-value deals with new partners in the West. This helps you stay secure and follows all the global banking rules today. Secondly, use CIPS if you are buying bulk goods from a supplier in China.

Furthermore, use UPI or its partners for quick travel costs or small digital tasks. Also, check the exchange rates for each system to see which one saves you the most. Lastly, check your search engine ranking to see how payment speed helps your traffic. Truly, a mix of these systems is your best tool for global success in 2026. It turns a complex task into a series of smart, fast wins for your brand. This ensures your business stays connected while the world changes its money rules.

Best Practices: Staying Safe in a Multi-System World

Finalizing your finance plan requires you to stay alert and very flexible. It needs you to know which rules apply to each system you choose to use. Clearly, you must follow all the laws to keep your accounts open and healthy. Therefore, follow these simple tips to keep your global payments safe and fast.

Simple Tips for Global Financial Success

Firstly, always verify the bank details of your partners before you hit send. This helps you avoid fraud and keeps your cash moving in the right direction. Secondly, keep your records clean so you can prove where your money came from.

Furthermore, use transition words in your invoices to make them easy for banks to read. Also, check the news for any new trade rules that might affect your chosen system. Lastly, check your search engine data to see if global fans trust your secure store. Truly, the world of finance is a journey that leads to a much better brand. It builds a path of wealth that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: Is SWIFT the same thing as a bank transfer?

SWIFT is the messaging network that banks use to send the instructions for a transfer.

Q2: Can I use UPI in every country today?

Not yet, but many nations like Singapore and the UAE now accept UPI-style payments.

Q3: Why did China create CIPS?

China wanted a system that helps more people use the yuan for global trade and deals.

Q4: Which system is the cheapest for small amounts?

UPI is usually the cheapest because it was built for small, fast mobile transactions.

Q5: Does my choice of payment system affect my SEO?

Indirectly, yes. Faster and more reliable payments lead to better user trust and site authority.

Payment gateway consulting is a specialized field. Businesses need expert help. They must pick the right payment systems. However, getting new clients can be hard. Therefore, consultants need to show their value fast. They must build trust quickly. Truly, lead magnet is powerful tool for this purpose. They offer free, valuable content. Consequently, this content helps attract potential clients.

Many consultants rely on word-of-mouth or cold outreach. Nevertheless, these methods are often slow. Furthermore, they might not show off your deep knowledge. Consequently, it is hard to stand out immediately. Always remember, lead magnets like “checklists” and “playbooks” solve this problem well. First, they give real value upfront. Next, they prove your expertise. Thus, by offering these free resources, you can attract more qualified leads. Then, you can turn them into paying clients. This builds your reputation. Additionally, it helps your consulting business grow smoothly.

The Consultant’s Challenge: Proving Expertise and Trust

First, let’s understand the core challenge for payment gateway consultants. They solve complex problems. These problems involve money, technology, and security. However, clients often do not know who to trust. They need proof of skill. Clearly, consultants must quickly show their deep knowledge. Therefore, they need smart ways to attract the right kind of attention.

Why Just Talking About Your Services Isn’t Enough

Simply listing your services on a website often does not work well. Clients need more information. Therefore, they need a reason to believe you are the best choice.

Here are some key limits of basic marketing for consultants:

Low Trust: New clients do not know you. They need to see proof of your abilities first.

Complex Topic: Payment gateways are hard to understand. Thus, clients need help breaking down the complexity.

Hard to Compare: Many consultants offer similar services. Consequently, clients struggle to see who is truly better.

No Value Upfront: Clients have to commit time or money before getting any help.

Passive Approach: Just waiting for clients to call means you might miss opportunities.

No Lead Capture: Visitors to your website leave without giving you contact info.

Lead magnets like checklists and playbooks solve all these problems. They offer immediate value. Furthermore, they demonstrate your expertise clearly. They also build trust. This helps turn interested people into real leads.

What are Lead Magnets? Your Client Attractor

So, what exactly are lead magnets for payment gateway consulting? They are free pieces of valuable content. You offer them in exchange for a potential client’s contact information. This information is usually an email address. Truly, they are designed to solve a small, specific problem for your ideal client. Thus, this proves your expertise. It also builds goodwill.

Types of Lead Magnets: Focus on Checklists and Playbooks

There are many types of lead magnets. However, “checklists” and “playbooks” are especially powerful for consultants. This is because they offer practical, actionable advice.

Here is why these are so effective:

Checklists: These are simple, step-by-step guides. They list actions a client needs to take. For example, use “PCI DSS Compliance Checklist for SaaS.” Another example is “10-Point Checklist for Choosing a New Payment Gateway.” They make complex tasks feel easy.

Playbooks: These are more detailed guides. They offer a strategy or a set of actions. The goal is to achieve a specific outcome. For example, try “The Small Business Playbook for Reducing Payment Processing Fees.” Another example is “Your Playbook for Integrating Stripe with Shopify.” They offer a full solution.

Here’s how lead magnets work:

Offer Value: You give away something genuinely helpful for free.

Solve a Small Problem: The lead magnet helps the client with an immediate pain point.

Show Expertise: It proves you know your stuff. Thus, it establishes you as an authority.

Capture Leads: In exchange for the magnet, the client gives you their email. Now, you can talk to them.

Build Trust: By helping them first, you build trust before asking for money.

Truly, lead magnets are not just freebies. Instead, they are strategic tools. They attract ideal clients. Furthermore, they start a valuable relationship.

Pillar 1: Checklists – Simple Solutions for Complex Problems

The first powerful lead magnet type is the checklist. For payment gateway consulting, checklists are perfect. This is because payment systems involve many steps and rules. Checklists simplify these complex processes. Clearly, they offer immediate, actionable value. Therefore, clients feel empowered. They also see your expertise quickly.

Making Complexity Manageable for Potential Clients

Firstly, checklists are extremely easy to use. Clients can quickly scan them. Furthermore, they can understand what needs to be done easily. This is great for busy business owners. They need quick answers. Secondly, checklists build confidence. When clients can tick off items, they feel like they are making progress. This positive feeling links back to your brand.

Furthermore, checklists demonstrate your knowledge well. By listing all the steps, you show that you know the entire process. For example, a “Payment Gateway Security Audit Checklist” shows your deep compliance understanding. Also, checklists can cover a wide range of topics:

Selecting a new payment processor.

Ensuring PCI DSS compliance.

Reducing transaction fees.

Onboarding a new e-commerce platform.

Troubleshooting failed payments.

Additionally, checklists encourage action. They are not just information. Instead, they are a call to do something. This makes them highly practical. Truly, by offering concise, helpful checklists, payment gateway consultants can attract leads. They can also provide immediate value. This establishes them as go-to experts in a clear way.

Pillar 2: Playbooks – Strategic Guides for Big Wins

Beyond simple checklists, the second powerful lead magnet type is the playbook. Playbooks offer a more comprehensive solution. They provide a step-by-step strategy to achieve a bigger outcome. Clearly, playbooks show a higher level of strategic thinking. Therefore, they attract clients looking for full solutions and long-term partnerships.

Guiding Clients to Significant Strategic Outcomes

Firstly, playbooks help clients with larger, more complex challenges. While a checklist might cover one aspect of PCI, a playbook could be “Your Complete Guide to a Secure and Scalable Payment Infrastructure.” This shows a strategic approach. Secondly, playbooks establish you as a thought leader. By providing a detailed, proven strategy, you showcase your unique method. You prove you can solve significant problems.

Furthermore, playbooks are highly shareable. A valuable playbook often gets passed around within a company. This increases your visibility. It also attracts more potential clients. Also, playbooks can tackle various strategic issues:

Optimizing payment flows to reduce cart abandonment.

Implementing a multi-currency payment strategy for global expansion.

Building a robust fraud prevention system.

Migrating from one payment gateway to another with zero downtime.

Developing a dunning management strategy to reduce churn.

Additionally, playbooks offer a deeper dive into your consulting process. They give a glimpse into how you would approach a client project. This pre-sells your services. Truly, by offering comprehensive playbooks, payment gateway consultants can attract higher-value leads. They can also demonstrate their strategic impact. This positions them for larger, more profitable engagements.

Pillar 3: Attracting, Nurturing, and Converting Leads

Lead magnets are just the start. The true power lies in how you use them to attract, nurture, and convert leads. It is a continuous process. You must get the magnet into the right hands. Then, you must build a relationship. Clearly, this strategic approach turns free downloads into paying clients. Therefore, a solid plan for promotion and follow-up is essential.

Your Strategy to Turn Downloads into Deals

Firstly, promote your lead magnets widely. Share them on your website. Use blog posts to introduce them. Post about them on LinkedIn and other relevant social media. Run targeted ads to reach your ideal clients. The more people see them, the more downloads you get. Secondly, use clear calls to action. Make it obvious how people can download your checklist or playbook. Use simple forms.

Furthermore, build an email nurturing sequence. When someone downloads your magnet, they join your email list. Send them a series of helpful emails. Share more tips. Offer case studies. Explain how your consulting services can help solve bigger problems. This builds trust over time. Also, qualify your leads. Not every download will be a perfect client. Use follow-up questions in your emails or on your form to understand their needs better.

Focus your direct outreach on the most promising leads. Lastly, offer a clear next step. At the end of your nurturing sequence, invite them to a free consultation. Offer a discovery call. Make it easy for them to take the next step towards becoming a client. Truly, by integrating lead magnets into a full marketing funnel, payment gateway consultants can consistently attract and convert ideal clients.

Best Practices: Crafting and Using Effective Lead Magnets

Creating successful lead magnets needs careful thought. It is not just about making a document. It is about understanding your audience and solving their pains. Clearly, well-designed lead magnets generate high-quality leads. Therefore, following these best practices is essential for your consulting business.

Your Blueprint for High-Converting Lead Magnets

Firstly, know your ideal client intimately. What are their biggest payment gateway problems? What questions do they ask? and What do they fear? Your lead magnet must directly address these pain points. Secondly, focus on a single, specific problem. Do not try to solve everything in one checklist or playbook. Address one clear issue. This makes the magnet more valuable. It also makes it less overwhelming.

Furthermore, make it actionable. Your lead magnet should give clients something they can do right away. Checklists are inherently actionable. Playbooks provide a plan of action. Also, design it professionally. Even though it is free, it must look good. Use clear formatting, good graphics, and your branding. This reflects well on your consulting services. Lastly, optimize for mobile. Many people will download on their phones. Ensure your PDFs are easy to read on small screens. Truly, by focusing on these best practices, payment gateway consultants can create lead magnets that truly resonate with their audience. This builds their authority. It also fills their client pipeline consistently.

Frequently Asked Questions (FAQs)

Q1: How often should I create new lead magnets for my consulting business?

You do not need new lead magnets constantly. Focus on creating a few high-quality ones that address core client pain points. Update them yearly or when industry changes occur. Promote your existing ones widely before creating many new ones.

Q2: What’s the ideal length for a checklist or playbook lead magnet?

For a checklist, keep it concise, typically one to three pages. For a playbook, aim for five to fifteen pages. The key is value, not length. Make it long enough to provide a solution but short enough to be digestible. It should not be overwhelming.

Q3: How do I know if my lead magnets are working?

Track your download rates (how many people download it). Also, track your conversion rate (how many downloaders become qualified leads or eventually clients). Monitor feedback from people who download it. High download rates and good conversion mean it is working well.

Q4: Should I gate (require email) every piece of valuable content I create?

No, not every piece. Some content, like blog posts, should be freely accessible to build general awareness and SEO. Lead magnets are specifically designed to capture leads, so they require an email. Balance free content with gated content.

Q5: What if my lead magnet gives away too much information? Will clients still hire me?

This is a common fear. A good lead magnet solves a small, specific problem. It shows how to do something. However, it does not do the doing for them. It proves your expertise and also shows them the value of your full service. It actually makes them more likely to hire you for the full implementation.

In today’s fast-paced digital economy, every transaction tells a story. Indeed, raw payment data, often overlooked, holds an extraordinary wealth of information just waiting to be uncovered. Therefore, payment analytics emerges as a critical discipline, transforming this vast stream of transaction data into actionable growth insights. Truly, it allows businesses to move beyond simple reporting, delving deep into customer behavior, operational efficiency, and revenue opportunities. Clearly, by harnessing the power of these insights, companies can make smarter decisions, optimize their payment strategies, and ultimately drive sustainable growth. Furthermore, ignoring this valuable data means leaving money and opportunities on the table.

Many businesses view payment data merely as a record of financial exchange. However, this perspective severely limits its potential. In reality, payment analytics provides a 360-degree view of your customer’s purchasing journey, from initial interest to successful checkout. This comprehensive understanding enables businesses to identify trends, predict future behaviors, and proactively address challenges. Always remember, the goal is not just to process payments, but to learn from them. This strategic approach turns every swipe, click, or tap into a valuable piece of intelligence, guiding future business decisions with precision and foresight.

The Foundation of Payment Analytics: What It Is and Why It Matters

To begin with, let’s clearly define what payment analytics actually entails. Simply put, payment analytics is the process of collecting, processing, and analyzing data generated from every financial transaction a business handles. This data includes information such as transaction amounts, payment methods, customer locations, timestamps, and even fraud attempts. Consequently, by applying various analytical techniques, businesses can uncover patterns, correlations, and anomalies that are invisible to the naked eye. This deeper understanding is paramount for making data-driven decisions that impact the bottom line.

Why Payment Analytics is Indispensable for Modern Businesses

Naturally, the importance of payment analytics cannot be overstated in the current competitive landscape. Firstly, it offers an unparalleled view into revenue optimization. By understanding which payment methods are preferred, where conversion rates drop, or how different pricing strategies impact sales, businesses can fine-tune their offerings. Secondly, it plays a vital role in fraud detection and prevention. Analyzing transaction patterns helps identify suspicious activities in real time, significantly reducing financial losses and protecting customer trust. Clearly, a robust analytics system can be your first line of defense.

Furthermore, payment analytics dramatically enhances customer experience. By knowing customer preferences and pain points in the payment journey, companies can streamline checkout processes, offer preferred payment options, and provide a seamless experience. This leads to higher customer satisfaction and loyalty. Lastly, it drives operational efficiency. Identifying bottlenecks in payment processing, understanding chargeback reasons, or optimizing vendor relationships can lead to substantial cost savings. Therefore, payment analytics moves beyond mere financial reporting, becoming a strategic tool for continuous improvement and growth.

Key Metrics and Dimensions in Payment Analytics

To truly extract value from your payment data, you must focus on the right metrics and dimensions. Indeed, simply collecting data is not enough; you need to know what questions to ask. Consequently, identifying key performance indicators (KPIs) relevant to payments allows you to measure success, pinpoint areas for improvement, and track progress over time. Therefore, a clear understanding of these metrics is fundamental to any effective payment analytics strategy.

Essential Metrics for Deeper Insights

First, consider conversion rates at various stages of the payment funnel. How many customers initiate a checkout versus how many complete it? Tracking this helps identify drop-off points. Next, examine average transaction value (ATV), which provides insights into customer spending habits. A rising ATV suggests effective upselling or a higher perceived product value. Furthermore, payment method breakdown is crucial. Understanding which payment types (credit card, digital wallet, bank transfer) are most popular among different customer segments enables you to optimize your offerings.

Moreover, chargeback rates are critical for assessing fraud and customer dissatisfaction. A high chargeback rate indicates underlying issues that need immediate attention. You should also track payment success rates, identifying any recurring errors or declines that might be deterring customers. Additionally, transaction volume and frequency over time can reveal seasonal trends and peak periods, informing staffing and inventory decisions. Finally, customer lifetime value (CLV), when viewed through the lens of payment data, offers insights into the long-term profitability of different customer segments. Truly, a holistic view of these metrics empowers businesses to make informed, impactful decisions.

Leveraging Payment Analytics for Revenue Optimization

One of the most immediate and impactful benefits of payment analytics is its ability to directly influence revenue. By scrutinizing transaction data, businesses can uncover opportunities to increase sales, improve conversion rates, and enhance profitability. Clearly, a deeper understanding of payment trends allows for targeted strategies that resonate with customer preferences and overcome potential hurdles in the buying journey. Therefore, every business aiming for growth must prioritize this area.

Strategies for Boosting Your Top Line

Firstly, use payment analytics to optimize your payment mix. By identifying the most preferred payment methods for different demographics or regions, you can ensure these options are prominently displayed and seamlessly integrated. For example, if mobile wallet usage is surging in a particular market, prioritizing that option can significantly boost conversions. Secondly, analyze data to identify and mitigate conversion bottlenecks. Perhaps a specific payment gateway consistently experiences higher failure rates, or customers abandon carts at the final payment step. Pinpointing these issues allows for targeted improvements, such as switching providers or simplifying the checkout flow.

Furthermore, payment analytics assists in dynamic pricing and promotions. Understanding how different price points or discount structures impact payment behavior and overall revenue enables businesses to tailor offers more effectively. For instance, you might discover that a specific payment method user responds better to loyalty rewards. Also, analyze subscription payment data to reduce churn. Identifying patterns in failed recurring payments, such as expired cards, allows for proactive communication and retries, thereby preserving recurring revenue. Ultimately, this strategic application of payment data ensures you’re not just processing transactions, but actively growing your revenue streams.

Enhancing Security and Fraud Prevention with Payment Analytics

In the digital landscape, where cyber threats are constantly evolving, safeguarding transactions against fraud is paramount. Payment analytics plays an indispensable role in strengthening security measures and proactively detecting suspicious activities. Consequently, by analyzing payment data patterns, businesses can build more robust fraud prevention systems, protect their financial integrity, and maintain customer trust. Clearly, neglecting this aspect can lead to significant financial losses and reputational damage.

Building Robust Fraud Detection Systems

Firstly, payment analytics enables the identification of unusual transaction patterns. Fraudulent activities often deviate significantly from normal purchasing behavior. For example, multiple small purchases from different geographic locations in a short period, or unusually high-value transactions from new customers, can be red flags. By establishing baselines of normal behavior, analytics systems can flag these anomalies for further investigation. This real-time detection is crucial for mitigating damage.

Secondly, you can use payment data to enrich fraud models. Integrating data points like IP addresses, device fingerprints, shipping addresses, and customer transaction history provides a more comprehensive picture for machine learning-based fraud detection algorithms. These algorithms learn from past fraudulent and legitimate transactions to predict future risks with high accuracy. Furthermore, analytics helps in reducing false positives. While aggressive fraud detection can block legitimate transactions, payment analytics refines the rules, ensuring that valid customers can complete their purchases without unnecessary friction, thereby improving the customer experience. Ultimately, leveraging payment analytics for fraud prevention transforms your security from a reactive measure into a proactive, intelligent defense mechanism.

Driving Operational Efficiency and Customer Experience

Beyond revenue and security, payment analytics offers profound benefits for streamlining operations and elevating the customer experience. In fact, by understanding the intricate details of how payments flow through your systems and how customers interact with them, businesses can identify inefficiencies and pinpoint areas for service improvement. Truly, an optimized payment journey directly translates into higher customer satisfaction and loyalty.

Streamlining Processes and Delighting Customers

Firstly, payment analytics helps in optimizing payment gateway performance. By monitoring success rates and latency across different providers, businesses can identify underperforming gateways or regions where specific providers excel. This allows for intelligent routing of transactions, ensuring higher success rates and faster processing times. Furthermore, analyzing transaction failure reasons—such as insufficient funds, incorrect card details, or technical errors—enables proactive communication with customers or internal system adjustments, thereby reducing abandoned carts.

Secondly, analytics provides insights into customer payment preferences, which is vital for enhancing the user experience. For instance, if a significant portion of your mobile users prefers digital wallets, making those options easily accessible and intuitive can significantly improve checkout speed and convenience. Conversely, if a particular region heavily relies on bank transfers, ensuring that option is robustly supported is crucial. Moreover, understanding chargeback reasons goes beyond fraud; it can reveal issues with product delivery, unclear billing, or poor customer service, prompting improvements across various operational touchpoints. In sum, payment analytics empowers businesses to fine-tune every aspect of their payment infrastructure, leading to smoother operations and a superior experience for every customer.

Frequently Asked Questions (FAQs)

Q1: What kind of data is included in payment analytics?

Payment analytics includes a wide range of transaction data, such as transaction amounts, timestamps, payment methods used (credit card, digital wallet, bank transfer), customer location, currency, device used for payment, success/failure status, and details related to chargebacks or refunds. It can also incorporate demographic and behavioral data if available.

Q2: How can payment analytics help reduce cart abandonment?

Payment analytics helps reduce cart abandonment by identifying common drop-off points and reasons for transaction failures. By analyzing data on where customers leave the checkout process, which payment methods fail most often, or what technical errors occur, businesses can pinpoint issues and make targeted improvements to streamline the payment flow and improve success rates.

Q3: Is payment analytics only useful for large enterprises?

Absolutely not! While large enterprises often have vast amounts of data, payment analytics is equally beneficial for small and medium-sized businesses (SMBs). Even with smaller transaction volumes, SMBs can gain valuable insights into customer preferences, identify fraud patterns, optimize payment costs, and improve their overall operational efficiency, leading to significant growth.

Q4: How does payment analytics contribute to better customer experience?

Payment analytics enhances customer experience by allowing businesses to understand and cater to customer preferences. By knowing which payment methods are preferred, which parts of the checkout process cause friction, or why transactions fail, companies can optimize their payment offerings, simplify the checkout flow, and provide proactive support, leading to smoother, more satisfying interactions.

Q5: What’s the difference between payment analytics and general financial reporting?

General financial reporting typically focuses on historical data to track overall financial health (e.g., total revenue, expenses, profits). Payment analytics, however, delves much deeper into the details of payment transactions to uncover actionable insights, predict future trends, optimize processes, and identify specific opportunities for growth, fraud prevention, and customer experience improvement.

India has seen a revolution in digital payments, mostly driven by platforms like UPI. While Tier-1 metros fully embrace this shift, true financial inclusion relies on deep penetration into the country’s heartland. Moving past the major urban centers reveals significant, unique regional challenges for digital payments. These challenges slow the journey toward a truly cashless economy. Understanding these obstacles is essential. This is crucial for policymakers and fintech companies. They want to unlock the vast potential of these emerging markets.

Infrastructure and Connectivity Deficits

One of the most persistent regional challenges for digital payments is the lack of robust infrastructure in smaller cities. Digital transactions rely entirely on uninterrupted power and consistent internet access. These are not always guaranteed outside of major cities. Frequent power outages interrupt transactions. This causes failures that quickly erode trust among merchants and consumers. Many smaller towns and remote areas suffer from poor quality internet. This low-quality service makes real-time payment applications slow. They can even be unusable during busy times. Improving this foundational digital infrastructure is a necessary first step. This step is vital for widespread digital adoption.

Low Digital and Financial Literacy

Technology adoption is only possible when users can operate it safely. In Tier-2 and Tier-3 cities, a widespread lack of digital and financial literacy remains a critical barrier. Many residents and small merchants are unfamiliar with digital payment interfaces. They are also unaware of necessary security measures. This knowledge gap creates two problems. First, there is a strong reluctance to adopt the systems. Second, there is an increased vulnerability to cyber fraud and scams. Most support materials are often only available in English. This language barrier complicates learning for a large group of people. Customized, local-language education is vital. It is needed for overcoming these regional challenges for digital payments.

Building Trust and Overcoming Security Fears

Trust is the most important currency in the financial ecosystem. Yet, it is hard to build trust in a complex, digital system. Concerns about security are high in smaller cities. News of online fraud spreads quickly here. This causes widespread skepticism. Users fear that errors will cause monetary loss. They worry the dispute resolution process will be too slow. Small merchants often prefer cash. They fear that digital records may increase their tax liabilities. Addressing these fears requires clear, simple dispute mechanisms. It also needs strict security frameworks. Awareness campaigns must focus on public reassurance.

The Merchant Adoption Hurdle

Consumers in Tier-2 and Tier-3 cities may be ready to pay digitally. However, small, fixed retail merchants may not be ready to accept it. This reluctance comes from several factors. Many merchants do not see enough customer demand. They do not want the initial effort of setup. They also avoid the minor costs of acquiring QR codes or POS terminals. Completing the necessary Know Your Customer (KYC) documents is often seen as tedious. It is also complex and time-consuming. Unless the merchant finds a clear, immediate business benefit, they often stick with cash. Incentives and simpler onboarding are needed. This must address these specific regional challenges for digital payments for businesses.

Socio-Cultural and Behavioral Inertia

Finally, deeply ingrained socio-cultural habits pose a formidable regional challenge for digital payments. In many smaller towns, cash-based transactions are a long-standing tradition. This supports close, community-based relationships. Digital transactions can feel impersonal. The human touch of handling cash is lost. This can discourage people from adopting the technology. Breaking this strong, old habit takes more than just making the technology available. It requires sustained, community-centric effort. This effort must use social norms to make digital payment the default. It must be the trusted and socially accepted way to transact for everyone.

Frequently Asked Questions (FAQs)

1 What is the primary infrastructure challenge in Tier-2 and Tier-3 cities for digital payments?

The main challenge is the inconsistent internet and poor power supply. This leads to transaction failures and quickly lowers user trust.

2 Why do merchants in smaller cities resist digital payments?

Merchants resist because they fear higher taxes, do not see enough customer demand, and find the KYC process too complex and time-consuming.

3 What is ‘digital literacy’ in the context of payments?

Digital literacy is the user’s ability to use payment apps safely. This includes spotting fraud and knowing how to resolve transaction disputes quickly and easily.

4 How does the language barrier affect adoption in these regions?

Most security warnings and instructions are often only in English. This makes it difficult for many local residents to understand the system and use it with full confidence.

5 What is a key non-technical factor slowing down digital payment growth in Tier-3 cities?

A major factor is the strong, traditional habit of using cash. This habit is deeply trusted, which makes the shift to abstract digital money slow and challenging for communities.

India’s economy is growing very fast. Therefore, businesses must adopt quick, digital payment methods. The Bharat QR Code is a major step in this direction. It is not just another payment option. Instead, it is a single, unified QR code system. The National Payments Corporation of India (NPCI) launched it. It was made with big card networks like Visa, Mastercard, and RuPay. This system helps Indian businesses accept payments easily. Furthermore, it helps businesses grow by lowering costs and speeding up transactions. This digital solution is critical for small and large businesses alike.

What Makes Bharat QR Different? (Bharat QR)

The core idea behind Bharat QR is universal compatibility. Before this, merchants needed different QR codes. They needed a different code for each mobile wallet or app. This was confusing for both the merchant and the customer. However, the Bharat QR code is an interoperable payment solution. This means one single code can accept payments from many sources.

For example, a customer can use any bank’s mobile app. They can use their linked debit card, credit card, or UPI account to pay. They simply scan the single Bharat QR code. This flexibility is a huge benefit. Consequently, merchants do not miss a sale because they do not support a customer’s specific payment app. This broad acceptance is vital for a growing business. Also, it brings a seamless experience to every customer, which builds loyalty.

Low Cost, High Security: A Win for Indian Businesses (Bharat QR)

Traditional Point-of-Sale (PoS) card machines are costly. They require a hardware purchase. Also, they have maintenance fees and paper costs. The Bharat QR code changes this completely. Merchants only need a smartphone and a printed QR sticker. This dramatically lowers the setup cost. Therefore, it makes digital payment acceptance possible for even the smallest vendor. This is a massive plus for small businesses in rural or semi-urban areas.

Furthermore, security is a key advantage. Payments go straight into the merchant’s linked bank account. This reduces the risk of cash handling, theft, or loss. The customer’s card details are never shared with the merchant. Since the customer authenticates the payment with their mPIN on their own phone, the transaction is extremely secure. Consequently, this increased security builds trust in digital payments. This trust is important for expanding your customer base.

Implementing Bharat QR for Business Growth (Bharat QR)

Implementing Bharat QR is simple and fast. First, you must have a bank account. Then, you contact your bank or a supported payment service provider. They will register you as a Bharat QR merchant. You will get a unique Merchant ID. This ID is embedded in your unique QR code. You can choose a static QR code. This is a printed sticker displayed at your counter. The customer scans it and enters the amount manually. Alternatively, you can use a dynamic QR code. This code is generated on a mobile app or screen for a specific bill amount. The customer scans it, and the amount is already filled in.

For example, a restaurant owner might use a dynamic code to print on the bill. A small shop owner might use a static sticker. In turn, both methods offer fast, instant payments. Payments are often settled immediately via IMPS. This quick turnaround improves the business’s cash flow. Good cash flow is the lifeline of a growing business. Moreover, the easy implementation allows any business to quickly participate in India’s digital economy.

Boosting Customer Experience and Revenue (Bharat QR)

Offering Bharat QR directly impacts customer experience. Customers find it convenient. They do not need to look for an ATM or carry exact change. They simply scan and pay. This speed at the counter reduces waiting times. Shorter queues lead to happier customers. Happy customers are more likely to return.

Therefore, the system directly supports business growth. The use of digital records simplifies accounting and tax filing. All transactions are recorded instantly. This saves manual labor. Furthermore, the ability to accept payments from multiple card networks and UPI through one code means fewer missed sales. The shift from cash to digital records can also help a business apply for bank loans later. Banks favor businesses with clear digital transaction histories. Ultimately, adopting Bharat QR is an essential strategy for any Indian business aiming for long-term growth and better customer service.

Frequently Asked Questions (FAQs)

1. What is the main difference between Bharat QR and UPI QR codes?

Bharat QR is a unified standard. It was created by NPCI, Visa, Mastercard, and RuPay. It can accept payments made via a linked card (debit/credit) or UPI. A simple UPI QR code primarily uses only the UPI system for payment.

2. Does a merchant need a special machine to accept Bharat QR payments?

No. This is one of the biggest benefits. Merchants do not need to invest in expensive PoS machines. All you need is a smartphone and a printed sticker of your unique Bharat QR code.

3. How do payments reach the merchant’s account?

Payments made through Bharat QR are credited directly and instantly into the merchant’s registered bank account. This uses the Immediate Payment Service (IMPS) for fast fund settlement.

4. Is Bharat QR only for large stores, or can small vendors use it too?

Bharat QR is perfect for small vendors. Because it requires minimal hardware and has low setup costs, it is a highly cost-effective solution for micro and small businesses.

5. Is it safe to use Bharat QR?

Yes, it is very secure. The customer’s card or bank details are not shared with the merchant. The customer authorizes every payment using their secure mPIN on their personal mobile device.

Is Blockchain a Revolution or Hype in Cross-Border Payments?

The world of global commerce depends entirely on the smooth movement of money. However, cross-border payments have long been plagued by high fees, frustrating delays, and a significant lack of transparency. Traditional systems, which rely on a complex network of correspondent banks, are slow and expensive. Therefore, they directly impact a business’s cash flow and profit margins. Naturally, a better solution is needed. Suddenly, blockchain technology arrived, promising to fix these exact pain points. Today, we investigate if this technology represents a true revolution or if it is merely overhyped. We must examine the core benefits to understand the future of international finance.

Understanding the Pain Points of Traditional Systems

Before discussing the solution, we should clearly understand the problem. Traditional cross-border payments, especially using the decades-old SWIFT network, involve many intermediaries. Specifically, a payment may pass through three or four banks before reaching its final destination. Therefore, each intermediary adds a fee, which quickly drives up the total cost. Furthermore, transactions often take three to five business days to settle. This delay is due to differing banking hours, time zones, and necessary manual compliance checks.

Consequently, businesses suffer from poor liquidity management and unpredictability. Moreover, tracking the payment’s exact location during this process can feel like operating in a black box, which creates uncertainty. Evidently, these legacy systems are inefficient and costly. This is where the decentralized ledger technology of blockchain steps in.

The Core Promise: Speed and Cost Reduction

The biggest appeal of blockchain in finance is its ability to bypass intermediaries. Since a blockchain is a distributed ledger, transactions move directly from the sender to the receiver on a peer-to-peer network. Therefore, this model radically simplifies the payment chain. Consequently, the transaction processing time drops from days to mere minutes or even seconds. This speed is a game-changer for international trade. Likewise, eliminating multiple correspondent banks removes the associated layering of fees. This reduction in cost is significant. For example, some blockchain-based solutions are reducing the total transaction costs by up to 80%. Clearly, the promise of near-instant and low-cost cross-border payments is highly appealing to businesses of all sizes, making it a powerful feature of the technology.

Enhanced Transparency and Security with Blockchain

In addition to speed and lower costs, blockchain delivers enhanced transparency and security. Because a transaction is recorded on a shared, immutable ledger, every authorized participant can see the payment’s status in real time. This end-to-end visibility is a stark contrast to the opaque nature of traditional systems. Therefore, this transparency significantly improves reconciliation and reduces disputes. Furthermore, the very nature of a blockchain—using cryptographic security—makes transactions highly tamper-proof. Once a block is added, it cannot be altered. Consequently, this decentralized security minimizes the risk of fraud and cyberattacks. As a result, companies gain a much higher degree of confidence in their cross-border payments. Ultimately, this trust is essential for global commerce.

Stablecoins and Liquidity Management

The volatility of cryptocurrencies is often cited as a challenge when discussing blockchain payments. However, stablecoins are solving this problem. Stablecoins are digital currencies pegged to fiat currencies like the US dollar. Therefore, they offer the speed and transparency of blockchain without the price swings of traditional crypto assets. Consequently, stablecoins are becoming the preferred rail for many modern cross-border payments. Furthermore, blockchain technology can also improve liquidity management. Banks and financial institutions often have to pre-fund accounts in various currencies across the globe to facilitate transfers. Now, blockchain’s real-time settlement capabilities and tokenized assets can reduce the need for large, trapped liquidity pools. Therefore, capital is deployed more efficiently across international markets. This optimization helps everyone.

The Role of Smart Contracts in Cross-Border Payments

The power of blockchain extends beyond simple money transfer; moreover, it introduces programmable money through smart contracts. Specifically, a smart contract is a self-executing agreement where the terms of the agreement are directly written into code. Consequently, these contracts automatically trigger a payment when certain predefined conditions are met. For example, a contract could release funds to a supplier immediately upon receiving confirmation of delivery from a logistics partner’s system. Therefore, this automation eliminates manual intervention and dramatically reduces operational risks. Furthermore, using smart contracts ensures compliance checks and regulatory reporting can be built directly into the transaction logic. Ultimately, smart contracts revolutionize the entire trade finance process, making the execution of cross-border payments faster, more reliable, and completely automated.

The Lingering Challenges: Regulation and Interoperability

Despite the numerous benefits, mass adoption of blockchain in finance is not without hurdles. Firstly, regulatory uncertainty remains a significant challenge. Different countries have varying rules regarding digital assets and distributed ledger technology. Therefore, navigating this fragmented legal landscape is complex for global financial institutions. Secondly, interoperability is a concern. Many different blockchain networks and private ledger systems exist, and they do not always communicate seamlessly with one another. Consequently, achieving a truly unified global system for cross-border payments requires significant standardization. Finally, integrating this new technology with older, legacy banking systems (the “core banking software”) requires a substantial investment in infrastructure and technical expertise. Therefore, the transition requires careful planning and a phased approach.

Hype or Revolution: The Verdict on Blockchain

When we look at the evidence, the impact of blockchain on cross-border payments is clearly more than just hype; moreover, it is a proven technology driving a revolution. While legacy systems like SWIFT are working to modernize, the core architectural advantages of decentralization, immutability, and real-time settlement offered by blockchain are fundamentally superior for global money movement. Solutions built on distributed ledger technology are already live, offering significant cuts in cost and time to businesses worldwide.

The challenges related to regulation and scalability are being actively addressed by global consortia and technology developers. Therefore, blockchain is not just a passing trend. Instead, it is the underlying technology that will redefine how money flows globally, ensuring a faster, cheaper, and more transparent future for cross-border payments.

Frequently Asked Questions (FAQs)

1. How does blockchain make cross-border payments faster?

Blockchain makes payments faster by eliminating the need for multiple intermediaries like correspondent banks. The payment is processed directly on a decentralized, peer-to-peer network. This allows for near-instant or real-time settlement, cutting transaction time from days to minutes.

2. Is using blockchain for international payments expensive?

No, in fact, it is typically much cheaper than traditional banking methods. Blockchain removes the layers of fees charged by multiple correspondent banks. The reduction in intermediaries can lead to cost savings of up to 80% on some cross-border payments.

3. What is the role of stablecoins in this process?