Global trade is moving faster than ever before. Most online stores now look for customers in every corner of the world. However, selling across borders brings many difficult hurdles. This is because every country has its own rules and preferred ways to pay. Therefore, businesses must find smart ways to handle these gaps. If they fail, they risk losing sales and trust. Successful e-commerce depends on a smooth and safe payment journey for everyone.

The Big Problems for Global Sellers

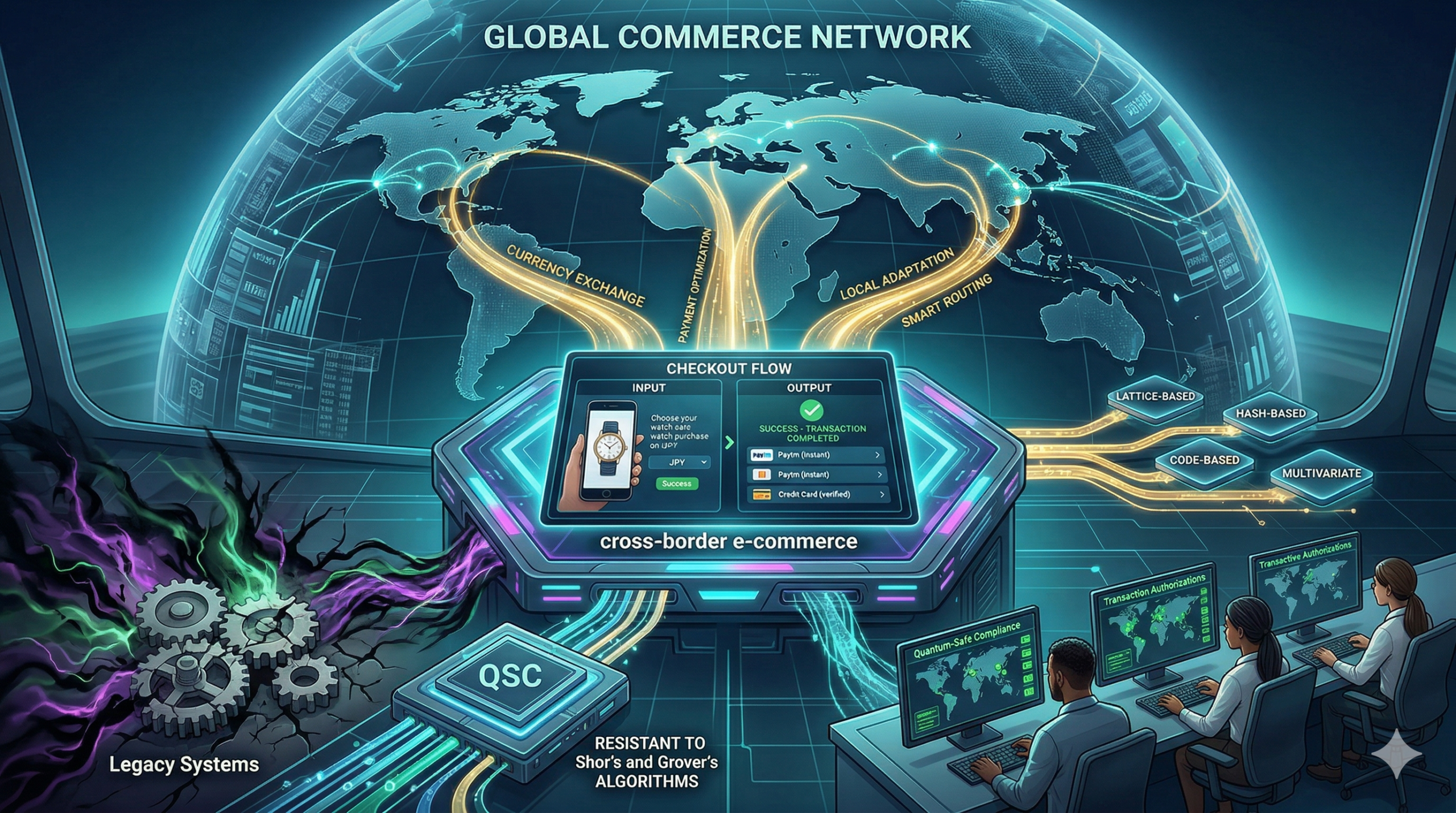

High fees are a major enemy of global growth. When a customer buys something from another country, banks often take a large cut. Consequently, the final price becomes too high for the shopper. This is because currency exchange rates are often unfair. Furthermore, hidden costs can surprise the customer at the final step. This leads to cart abandonment. Therefore, e-commerce firms must be very clear about all costs from the start.

Another big issue is the variety of payment habits. For instance, shoppers in Europe might prefer digital wallets. Meanwhile, customers in Asia might use QR codes or local bank transfers. If a store only offers credit cards, it will fail in these regions. Thus, a one-size-fits-all plan does not work. Every e-commerce site needs to adapt to local tastes to stay ahead.

Solutions for a Better Payment Journey

Multi-currency pricing is a vital tool for success. Customers want to see prices in their own money. Because this removes confusion, it builds instant trust. Furthermore, using a local acquiring bank can reduce transaction fees. This means the store keeps more profit while the user pays less. In short, e-commerce wins when the math is simple for the buyer.

Smart routing is another great way to fix failures. Sometimes, a bank might block a foreign payment by mistake. However, modern systems can instantly try a different bank to finish the sale. This keeps the flow moving without any delay. Because the user does not see the struggle, the experience feels like magic. Therefore, e-commerce platforms must use these intelligent tools to prevent lost sales.

Staying Safe Against Global Fraud

Security is the most important part of any global sale. Hackers are always looking for ways to steal data across borders. Luckily, new AI tools are great at spotting fraud by looking at millions of data points. If a transaction looks odd, the system stops it fast. This keeps your money and data very safe. Because the AI is so smart, it rarely blocks real customers. Thus, e-commerce stays strong and secure for everyone.

Additionally, 3D Secure 2.0 helps verify identity without making the process slow. It uses data to prove the user is real in the background. When you use these tools, the checkout flow feels very smooth. You just click and go. Therefore, the risk of a mistake or theft is very low. This is the future of e-commerce in a connected world. Finally, safety ensures that your brand grows a good name worldwide.

The Future of Global Trade

We are only at the start of a massive shift. Soon, every store will use local solutions to talk to global fans. This means we will see faster shipping and lower fees for everyone. Instead of a hard process, we get a tailored world of products. E-commerce makes every global transaction feel like a local one. It is the best way to trade in 2026. If you want to stay ahead, you must use these solutions now. In conclusion, a better payment journey is the key to global success.

Frequently Asked Questions

1. Why do global payments often fail?

They fail because banks might flag foreign cards as high-risk or due to technical errors in legacy systems.

2. How can I reduce currency exchange fees?

You should use a local payment provider or an e-wallet that offers better rates than traditional banks.

3. What is the best payment method for Asia?

Local digital wallets and QR-based systems are the most popular choices for shoppers in that region.

4. Does 3D Secure slow down my checkout?

No, the 2.0 version is much faster and often works in the background without bothering the user.

5. Is it hard to set up multi-currency pricing?

Most modern payment gateways offer this feature as a simple setting you can turn on.

Financial fragmentation can make traveling and trading between different nations very difficult because traditional currency exchange is often slow and expensive. However once you learn how Indonesia’s QRIS expansion connects Asian markets you will see a much smoother payment experience. I have analyzed how this cross border growth allows local businesses to accept international payments while seeing a massive boost in tourist spending.

The Problem With Traditional Currency Exchange

Many travelers still rely on physical cash or credit cards that charge very high fees for every international transaction. This approach creates a massive disconnect because users want a fast and digital way to pay for goods in a foreign country. You might feel frustrated when your local payment app fails to work the moment you cross a border. Traditional exchange methods are like carrying a heavy bag of coins and hoping every shop has the right change for you.

The solution lies in a unified digital system that works across different national boundaries instantly. Indonesia’s QRIS system allows a user to scan a single code to pay in their own currency while the merchant receives local funds. Once nations apply these interoperable standards you will see much higher trade efficiency across Asia. I have seen small vendors in Bali and Bangkok increase their sales by simply accepting digital payments from foreign visitors.

Strategy 1: Link Local QRIS to Regional Networks

Indonesia is actively connecting its national QR standard to other countries like Thailand, Malaysia, and Singapore. Specifically this link allows an Indonesian traveler to use their local banking app to pay for a meal in Kuala Lumpur. This integration removes the need for physical currency and lowers the cost for every person involved. Therefore you get a seamless experience that feels just like paying for something in your hometown.

Strategy 2: Implement Real Time Exchange Rates

Users love transparency because they want to know exactly how much they are spending in their own money. QRIS expansion uses real time rates to convert the price of a product at the exact moment of the scan. For example a shopper can see the cost in Rupiah even if the price tag is in Thai Baht. This level of detail builds immediate trust and encourages users to spend more during their travels.

Strategy 3: Optimize for Small Merchant Adoption

Many local businesses in Asia do not have expensive credit card machines because the fees are too high for their small margins. However QRIS is very cheap to implement since it only requires a printed code or a simple smartphone app. Because of this even the smallest street food stall can now accept international digital payments. This inclusion helps a wider range of local businesses benefit from the growth of regional tourism.

Strategy 4: Use QRIS to Drive Tourism Spending

A convenient payment system is a great way to encourage visitors to spend more money on local experiences. You can tell a traveler that they can pay for everything from a taxi ride to a luxury dinner using one single app. This creates a natural sense of ease that makes people more likely to choose Indonesia as their next destination. Consequently the local economy grows as digital friction disappears from the travel journey.

Strategy 5: Automate High Speed Settlement

Manual bank transfers between countries take a long time and often involve many different middlemen. However the QRIS cross border network uses advanced technology to settle transactions almost immediately. Your local business does not have to wait days to receive the funds from an international customer. Therefore you maintain a healthy cash flow and can restock your inventory without any delay.

Strategy 6: Provide Secure and Encrypted Transactions

Security is a primary concern for everyone who moves money across international borders today. QRIS uses high level encryption to ensure that every payment is safe from hackers and fraudulent activity. This ensures that both the customer and the merchant are protected during the digital handshake. Prompt and secure transactions help build a strong reputation for the Asian financial network as a whole.

Strategy 7: Collect Data for Regional Market Insights

Social proof and market data help you grow your business by showing you what your customers truly want. Indonesia’s central bank can use the data from QRIS to see which regions are seeing the most international spending. This allows the government to tailor its tourism and trade policies to match real world behavior. This simple step makes the entire regional economy much more responsive to changing user needs.

Strategy 8: Create a Seamless Bridge for Asian Trade

There are times when small businesses want to buy supplies from a neighboring country without opening a foreign bank account. You should use QRIS as a bridge that allows for easy business to business payments across Asia. This reduces friction and prevents small owners from having to deal with complex international wire transfers. A smooth payment bridge keeps the regional supply chain moving forward without any stops.

Strategy 9: Use Mobile Accessibility for Financial Inclusion

You want to make it as easy as possible for everyone to join the digital economy regardless of their location. Because many people in Asia use smartphones as their primary tool for internet access QRIS is the perfect solution. This saves people from the extra step of visiting a bank or carrying large amounts of cash. Therefore a single smartphone starts a financial journey that can lead directly to better economic health.

Strategy 10: Retarget International Shoppers Digitally

If a tourist buys from your shop using QRIS you can potentially use that connection to keep them engaged. For instance you can offer a digital loyalty card that stays in their mobile wallet for their next visit. This reminder should focus on the unique local experience your brand offers to every traveler. Remarketing with a personalized touch is a great way to win a repeat customer from across the globe.

Conclusion and Next Steps

If you follow the growth of this system you should soon see much better results for regional Asian trade. Please do not forget to let me know how you got on in the comments below. I am always interested in hearing your thoughts so tell me which part of this expansion you felt worked best for you.

FAQs

1 What is Indonesia’s QRIS expansion?

It is the growth of a unified QR payment standard that allows users to pay digitally across different Asian countries.

2 How does it help local Asian businesses?

It allows small merchants to accept international payments easily without expensive hardware or high fees.

3 Can I use QRIS in Thailand or Malaysia?

Yes, Indonesia has already established links with these countries to allow for cross border digital payments.

4 Is the QRIS system safe for travelers?

Yes, it uses advanced encryption and central bank oversight to ensure that every transaction is secure.

5 What is the first step for a business to accept QRIS?

The first step is to register with a participating bank or payment provider to receive your unique merchant QR code.

You must look at how your business takes payments today. Therefore, you should learn about the risks of relying on US firms. Truly, most European stores use card networks based in America like Visa and Mastercard. Consequently, your ability to sell goods depends on the rules of another country.

Many people think that using global giants is the only safe choice. But, the reality is that this dependence creates a hidden danger for your shop. Always remember, a diverse payment system is a strong signal for any search engine. This ensures that your brand stays stable and your sales stay high. This approach requires you to find local payment alternatives. It helps you build a much more independent business for the long term. It makes your daily operations feel much more secure and very effective.

Phase 1: The Risk of Foreign Rules and Sanctions

First, you must understand who makes the rules for your payments. Why is it risky for a US firm to control a European transaction? Clearly, foreign laws can change how these firms operate in Europe. Therefore, a political shift in the US could impact your local business.

How Foreign Control Impacts Your Business

Here are several ways that relying on foreign firms creates a risk for you:

Political Weaponization: Foreign networks can cut off service due to non-EU political shifts.

Policy Changes: US laws could limit who you can sell to in your own city.

Fee Increases: Foreign firms can raise their prices without any local control.

Data Privacy: Your customer data might move to servers outside of the EU jurisdiction.

Service Outages: Technical issues in another country can stop your sales in Europe.

Slower Support: Help desks might be far away and in different time zones.

Lower Sovereignty: The EU has less power to fix problems in the payment system.

Truly, these risks are real even if they seem small right now. But, you must also look for ways to protect your store from these shifts. This keeps your cash flow safe and prevents sudden stops in your work. It creates a very secure and high standard for your business.

Phase 2: The Rising Costs of Global Card Networks

So, how much do you pay to take a credit card payment today? Truly, the costs of using global networks are often higher than local tools. Consequently, a large part of your profit goes to firms far away from your home. It acts as a constant drain on your hard-earned revenue.

How High Fees Hurt Your Growth

Here is how global payment fees impact your bottom line:

High Interchange: You pay a fee to the bank for every single tap or swipe.

Scheme Fees: The card network takes a cut of every sale you make online.

Cross-Border Costs: Fees go even higher when you sell to a neighbor in the EU.

Hidden Charges: Many small fees are buried in your monthly bank statements.

Currency Risk: You might lose money when your sales convert to a different coin.

Refund Fees: You often lose money even when a customer returns an item.

Site Trust: Lower fees help you offer better prices for better search engine rank.

Furthermore, this improves your search engine performance by letting you spend more on marketing. It makes your brand look very competitive and ready for 2026 challenges. This ensures that you keep more of the money you earn from every sale. It creates a very fast and clear path for your financial growth.

Phase 3: The Rise of Wero and Local Solutions

The third phase looks at the new tools designed to fix this problem. Clearly, Europe wants to build its own way to pay for goods. Therefore, you should learn about Wero and the European Payments Initiative.

Why Local Tools Are Better for You

Firstly, Wero is phasing into popular systems like iDEAL starting in 2026. This allows you to get your cash in seconds rather than waiting for days. Secondly, local tools are built to follow European laws and protect your privacy.

Furthermore, they offer lower fees because they do not have to pay global networks. Also, you can find help from teams located right in your own region. Lastly, remember that supporting local tech helps your search engine reputation. Truly, tools like Wero are the best way to handle your sales safely. It allows you to reach your fans without relying on a middleman from abroad. This is why top European stores are switching to local tools now.

Phase 4: Preparing Your Shop for a Sovereign Future

The fourth phase addresses how you can start to move away from foreign firms. Clearly, you do not have to stop using cards all at once. Therefore, you should offer your customers more than one way to pay.

How to Diversify Your Checkout Page

Firstly, add local payment options like Wero or Bizum to your store. This helps your fans choose the method they trust the most. Secondly, tell your customers why local choices are faster and more secure.

Furthermore, check if your bank offers a way to take direct account-to-account payments. Also, use simple words to explain the benefits of new tools on your site. Lastly, check your search engine data to see if users like the new options. Truly, a diverse checkout is your best tool against foreign risks. It turns your store into a partner that supports the local economy. This ensures your business stays strong and grows from the inside out.

Best Practices: Choosing Your Payment Partners

Picking the right partner requires you to look at where they are based. It needs you to think about the long-term safety of your company. Clearly, a good partner is one that shares your values and keeps your data safe. Therefore, follow these simple tips to find the perfect local payment choice.

Simple Steps for a Safer Business

Firstly, ask your current provider if they are based in the EU or the US. This helps you know where your data and fees are going every day. Secondly, look for tools that offer instant payments for a lower cost.

Furthermore, read the fine print to find any hidden foreign processing fees. Also, use transition words in your own guides to make payments easy for fans. Lastly, check your search engine ranking to see how checkout speed helps you. Truly, moving to local payment tools is a journey that leads to a better brand. It builds a path of safety that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: Why is it bad to use only US card networks?

It is risky because foreign laws could disrupt your service or raise your fees without notice.

Q2: What is Wero?

Wero is a new European digital wallet that allows for fast and secure payments across the EU.

Q3: Does using local tools help my search engine rank?

Yes, faster and cheaper payments improve your site’s trust and user experience scores.

Q4: Are local payment tools as safe as global ones?

Yes, tools like Wero use the latest security tech and follow strict EU privacy laws.

Q5: When will iDEAL become Wero?

The transition starts in early 2026 and should be fully finished by the end of 2027.

Many people think that digital money is just another way for banks to track us. But, the reality is that a digital euro offers a safe and public choice for everyone. Always remember, a stable money system is a strong signal for any search engine. This ensures that your business can grow in a secure and trusted environment. This approach requires the bank to build a tool that works for all citizens. It helps the region build a much more resilient financial future for the long term. It makes your daily transactions feel much more secure and very effective.

Phase 1: Protecting Europe from Foreign Payment Giants

First, you must look at who controls how we pay for things today. Why does the ECB worry about using only private foreign apps and cards? Clearly, relying too much on non-European firms creates a big risk for the local economy. Therefore, a digital euro ensures that Europe has its own independent way to move money.

How a Local Digital Currency Keeps Control

Here are several ways a digital euro protects the local payment system:

Local Control: The ECB keeps the power to manage the money supply within Europe.

Less Risk: People do not have to rely only on private firms that could fail.

Direct Access: Every citizen gets a direct way to hold safe central bank money.

Fast Settlement: Payments happen instantly without needing many middle steps.

Data Privacy: The ECB aims to protect user data better than private ad-driven firms.

System Backup: It acts as a back-up if private card networks ever go down.

Search Engine Trust: Stable local systems improve the overall search engine reputation of the region.

Truly, this move gives Europe a stronger voice in the global digital economy. But, the bank must also ensure that the tool is easy for everyone to use. This keeps the public on their side and prevents a loss of trust in the bank. It creates a very efficient and high standard for the future of money.

Phase 2: Ensuring Digital Cash Remains a Public Good

So, how do we keep the best parts of physical cash in a digital world? Truly, cash is the only form of money that belongs to the public and not a private firm. Consequently, the ECB wants to make sure that digital cash stays free and open for all. It acts as a digital anchor that keeps the whole money system stable and fair.

Keeping Digital Money Open for Everyone

Here is how the digital euro mimics the benefits of physical cash:

Free to Use: Basic use for citizens will not cost any extra fees or charges.

Offline Use: The bank wants the tool to work even without an internet connection.

Wide Acceptance: Every shop in the euro area will eventually take it as payment.

Privacy Focused: The bank will not see exactly what you buy with your money.

Simple Access: People without bank accounts can still use the digital euro easily.

High Security: It uses the best 2026 tech to stop fraud and theft.

Brand Trust: Reliable money helps your site earn more search engine authority.

Furthermore, this improves your search engine score by creating a more stable digital market. It makes the euro area look very modern and ready for 2026 challenges. This ensures that every person has a safe way to pay, even if they do not like banks. It creates a very fast and clear path for financial inclusion.

Phase 3: Fighting the Risks of Private Crypto Assets

The third phase looks at the rise of private coins and stablecoins. Clearly, these private assets can be very volatile and risky for normal users. Therefore, the ECB offers a digital euro as a safe and stable choice backed by the bank.

Why Central Bank Money Is Safer Than Crypto

Firstly, the value of a digital euro stays exactly the same as a physical euro. This allows you to save and spend without worrying about sudden price drops. Secondly, the ECB provides a legal guarantee that your digital money is always safe.

Furthermore, the bank can stop illegal activities more easily than with private coins. Also, the system uses less energy than most crypto tools to protect the environment. Lastly, remember that using stable money helps your search engine ranking and business safety. Truly, the digital euro is the answer to the chaos of the private crypto market. It allows people to enjoy digital speed without the high risk of losing their life savings. This is why the ECB is moving so fast to launch this tool.

Phase 4: Supporting Innovation in the Digital Economy

The fourth phase addresses how a digital euro helps new tech firms grow. Clearly, a smart digital currency allows for new types of automated payments. Therefore, the ECB wants to give developers a stable platform to build their new apps.

How Digital Money Drives New Tech

Firstly, firms can use the digital euro to set up automatic, smart contracts. This helps businesses run much faster and with fewer manual errors. Secondly, it allows for micropayments that are too small for normal credit cards to handle.

Furthermore, it makes it easier for small firms to sell their goods across all of Europe. Also, the digital euro works perfectly with the latest 2026 smartphone features. Lastly, check your search engine ranking to see how new payment tech helps your site. Truly, the digital euro is a platform for the future, not just a way to pay. It turns a simple coin into a smart tool for the global digital marketplace. This ensures that European firms can compete with the best in the world.

Best Practices: Preparing for a Digital Euro World

Getting ready for a digital euro means staying informed about the latest bank news. It needs you to think about how your own business will take these payments. Clearly, the transition will take time, but you should start your plan today. Therefore, follow these simple tips to stay ahead of the digital money shift.

Simple Steps for Your Financial Future

Firstly, read the official ECB reports to understand the rules of the new tool. This helps you know exactly how to handle your own taxes and savings. Secondly, check if your current payment software will support a digital euro soon.

Furthermore, talk to your bank about how they will help you move your funds. Also, use simple words in your own store to explain the new payment choice to fans. Lastly, check your search engine data to see if users are asking for digital cash. Truly, the digital euro is a journey toward a more stable and modern Europe. It builds a path of safety that lets the whole region grow very fast. This secures your future in the financial world for a long time.

Frequently Asked Questions (FAQs)

Q1: Will the digital euro replace physical cash?

No, the ECB says the digital euro will exist alongside physical cash for the foreseeable future.

Q2: Is the digital euro a type of cryptocurrency?

No, it is a central bank digital currency, which means it is stable and backed by the government.

Q3: Does using a digital euro help my search engine rank?

Yes, accepting modern and secure payment methods improves your site’s user trust and search engine authority.

Q4: Can the ECB see every single thing I buy?

No, the ECB is designing the digital euro with high privacy standards for everyday transactions.

Q5: When can I start using the digital euro?

The ECB is currently in the testing phase and aims for a full launch around 2026 or shortly after.

The way we pay for things is changing at an incredible speed as we look toward 2026. Therefore, tapping your phone or card is becoming the new normal for millions of people. Truly, the future of contactless payments and NFC payments is here, and it is growing rapidly in India and across the world. Consequently, understanding this technology is key for any business that wants to stay modern and competitive.

Some people feel that cash is still the best way to pay, especially in certain regions. But, the convenience and speed of these new methods are winning over more users every single day. Always remember, a fast and easy payment option is a strong signal for any search engine to value your website. This ensures that customers have a smooth experience and are more likely to return to your store. This approach requires looking beyond traditional payment terminals. It helps you build a much more efficient and customer-friendly checkout system. It makes your entire business operation feel modern and very secure.

Phase 1: The Rise of Contactless in India

First, let us look at how India is leading the charge in adopting tap-and-pay technology. Why has a country with a large cash economy embraced digital payments so quickly? Clearly, government initiatives and the widespread use of smartphones have created a perfect storm for growth. Therefore, the Unified Payments Interface (UPI) system has played a massive role in this shift.

Driving Factors for Contactless Growth in India

Here are several reasons why contactless payments are booming in India:

UPI Integration: This system makes instant, secure payments very easy for everyone.

Smartphone Penetration: Billions of phones support NFC, making tap-to-pay accessible.

Government Push: Policies encourage digital transactions to boost the economy.

QR Code Acceptance: Even small shops use QR codes for quick, simple payments.

Debit/Credit Card Upgrades: Most new cards come with contactless features built-in.

Merchant Adoption: More businesses are getting NFC-enabled payment terminals.

COVID-19 Impact: The pandemic accelerated the move to touch-free transactions.

Truly, India’s journey shows the world how quickly a large population can adopt new payment habits. But, this rapid growth also requires constant innovation to keep the systems secure and reliable. This keeps the payment networks strong while more people start using them. It creates a very dynamic environment for financial technology companies.

Phase 2: Global Trends and NFC Technology

So, how is the rest of the world embracing these payment innovations? Truly, the shift to contactless is a global phenomenon, driven by the power of Near Field Communication (NFC) technology. Consequently, tapping your phone or watch is becoming as common as swiping a card in many developed nations. It acts as the invisible link that makes these speedy transactions possible everywhere.

Key Global Developments in Contactless Payments

Here is how NFC and contactless payments are changing the world:

Apple Pay/Google Pay: These major mobile wallets use NFC for quick, secure payments.

Smart Wearables: Watches and fitness trackers now allow you to pay with a tap.

Transit Systems: Many cities let you tap your card or phone to ride buses and trains.

Open Loop Payments: Customers can use their regular bank cards directly for transit fares.

Biometric Integration: Fingerprint or face scans add an extra layer of security to transactions.

EMV Standard: This global standard ensures secure chip-based contactless transactions.

Device-to-Device Payments: NFC can enable payments directly between two phones without a terminal.

Furthermore, this global embrace of NFC helps improve your search engine ranking by boosting your overall site speed. It makes your brand look very modern and connected to international trends. This ensures that you are ready for customers no matter where they are coming from. It creates a seamless experience across borders and different cultures.

Phase 3: Benefits for Merchants and Consumers

The third phase looks at why everyone benefits from this payment revolution. Clearly, faster transactions and better security are good for both the buyer and the seller. Therefore, understanding these advantages can help you make a strong case for upgrading your payment systems.

Winning with Contactless Payments

Firstly, for consumers, it means speed and convenience. No more fumbling for cash or waiting for a chip card to read. Secondly, it offers enhanced security. Tokenization makes transactions much safer than traditional card swipes.

Furthermore, for merchants, it means faster lines. This allows you to serve more customers in less time during busy periods. Also, it reduces cash handling costs and risks. Less cash means less chance of theft or accounting errors. Lastly, it improves your search engine performance. Faster checkouts mean lower bounce rates and a better user experience. Truly, it is a win-win situation that drives efficiency and safety. It allows businesses to focus on sales rather than payment problems. This is why more companies are investing in these modern payment terminals every single day.

Phase 4: Challenges and Overcoming Them in 2026

The fourth phase addresses the hurdles that still exist for widespread adoption. Clearly, no new technology is perfect, and there are always things to consider. Therefore, understanding these challenges allows you to plan better and avoid common pitfalls.

Navigating the Road Ahead for Contactless Payments

Firstly, merchant education is crucial. Many small businesses still need to learn how to set up and use NFC terminals effectively. Secondly, security concerns among some users. Even with advanced protection, some people are hesitant to trust new payment methods.

Furthermore, inconsistent infrastructure in rural areas. Not all places have reliable internet or power for digital payment systems. Also, the cost of upgrading older terminals. Some businesses might find the initial investment too high. Lastly, ensuring inclusion for all users. Not everyone has a smartphone or a bank account, especially in developing regions. Truly, these challenges require a balanced approach, focusing on education and accessibility. It turns potential obstacles into opportunities for innovation and growth. This ensures that the payment revolution benefits everyone, not just the tech savvy.

Best Practices: Embracing the Contactless Future

Moving fully into the world of tap-and-pay requires a strategic mindset and an openness to change. It needs a focus on customer needs and the long term vision of your business. Clearly, simply installing a terminal is not enough; you must also promote its use. Therefore, follow these simple habits to keep your payment systems cutting edge.

Strategies for Long-Term Contactless Success

Firstly, always offer multiple payment options. While promoting contactless, still accept other forms of payment for those who prefer them. Secondly, clearly display contactless payment logos at your checkout. This tells customers you are ready for their preferred payment method.

Furthermore, train your staff to guide customers on how to use tap-and-pay. A friendly explanation can ease any hesitation. Also, monitor your transaction data for insights. See which payment methods are most popular and why. Lastly, keep an eye on your search engine ranking and site speed. A seamless payment process contributes to a great online experience. Truly, embracing contactless payments is an investment in your business’s future. It builds a reputation for convenience and modernity. This secures your place in the fast evolving digital economy of 2026.

Frequently Asked Questions (FAQs)

Q1: Is NFC the same as contactless payment?

NFC (Near Field Communication) is the technology that enables contactless payments. So, all NFC payments are contactless, but not all contactless payments use NFC (e.g., some QR code payments).

Q2: How does contactless payment improve my search engine ranking?

A fast and convenient checkout experience leads to lower bounce rates and higher customer satisfaction. These are positive signals that search engines value for ranking.

Q3: Are contactless payments more secure than swiping a card?

Yes, they are generally more secure. Contactless payments use encryption and tokenization, which means your actual card number is not shared during the transaction.

Q4: What is UPI and how does it relate to contactless payments in India?

UPI is a real-time payment system in India that facilitates instant bank-to-bank transfers. Many apps that use UPI also integrate QR codes and NFC for contactless transactions.

Q5: What is the biggest barrier to wider adoption of contactless payments?

The biggest barrier is often the cost for merchants to upgrade older point-of-sale systems and a lack of awareness or trust among some consumers.

The world of online commerce is moving faster than ever as we look toward 2026. Therefore, choosing the right way to accept money is a critical decision for every business owner. Truly, the debate between digital wallets and payment gateways is becoming a central topic for growth. Consequently, understanding how these two tools work together is the best way to ensure your customers stay happy and loyal.

Some people feel that you only need one or the other to run a successful store. But, the reality is that they serve very different roles in the modern checkout process. Always remember, a smooth payment flow is a top signal for any search engine to trust your website. This ensures that you do not lose customers at the very last second of their journey. This approach requires a clear look at how data and money move through the internet. It helps you build a much more reliable and profitable checkout experience for everyone. It makes your financial strategy feel modern and very secure for the years ahead.

Phase 1: Understanding the Role of the Payment Gateway

First, let us look at the silent engine that powers every online transaction. Why is the gateway considered the foundation of any digital storefront? Clearly, it acts as the bridge between your website and the complex world of banks. Therefore, you cannot accept a single card payment without a strong gateway in place.

Key Features of a Modern Payment Gateway

Here are several things that a gateway does for your business every day:

Data Encryption: It keeps credit card numbers safe as they travel across the web.

Fraud Detection: Smart filters check for stolen cards and risky buyer behavior.

Bank Communication: It asks the customer bank if there is enough money for the buy.

Transaction Routing: It moves the money from the buyer to your merchant account.

Receipt Generation: It sends a digital proof of purchase to the buyer instantly.

Refund Management: It allows you to send money back to customers with ease.

Multi Currency Support: It helps you sell to people in different countries effortlessly.

Truly, a gateway is the invisible guard that keeps your money moving safely. But, it does not hold money itself like a wallet does for a user. This keeps the technical side of the payment separate from the user account. It creates a very stable system for handling thousands of sales every hour.

Phase 2: Why Digital Wallets Are Taking Over the User Experience

So, how do digital wallets change the way people actually buy your products? Truly, the convenience of a wallet like Apple Pay or Google Pay is hard to beat in 2026. Consequently, many shoppers now expect to finish their purchase with just a thumbprint or a face scan. It acts as a digital container for all the payment info a customer needs.

The Benefits of Supporting Digital Wallets

Here is why merchants are focusing more on wallet support this year:

Faster Checkout: Users do not have to type in long card numbers or addresses.

Higher Conversion: Fewer steps at checkout mean more people finish their orders.

Better Security: Wallets use tokens so your store never sees the real card data.

Mobile Optimization: They are built specifically for the billions of phone users.

Biometric Safety: Using a face or finger scan reduces the risk of fake orders.

Local Popularity: Different countries have specific wallets that people trust.

Loyalty Links: Many wallets automatically track rewards and coupons for the user.

Furthermore, supporting these tools can help your search engine visibility among mobile shoppers. It makes your brand look modern and very easy to work with on any device. This ensures that you are meeting your customers exactly where they want to shop. It creates a very friendly and fast environment for every new visitor.

Phase 3: The Synergy Between Wallets and Gateways

The third phase looks at why you actually need both of these tools to succeed. Clearly, it is not a matter of picking one over the other in a modern setup. Therefore, you should look for a gateway that offers deep integration with all major digital wallets.

How These Two Technologies Work Together

Firstly, the wallet provides the payment data to the checkout page. This makes the start of the process very fast for the customer. Secondly, the payment gateway takes that data and sends it to the banking networks for approval.

Furthermore, the gateway provides the security layer that protects the merchant from fraud. Also, the wallet provides the convenience that keeps the customer coming back for more. Lastly, having both ensures that your search engine ranking stays high due to low bounce rates. Truly, they are two sides of the same coin in the world of digital finance. It allows you to offer the best of both worlds: speed and safety. This is why the most successful stores in 2026 are using an all in one approach.

Phase 4: Where Should Your Business Focus for 2026?

The fourth phase is about deciding where to spend your time and budget next. Clearly, your focus should depend on who your customers are and what you sell. Therefore, you must look at your own data to see where the biggest gaps exist today.

Choosing Your Priority Based on Business Type

Firstly, focus on your gateway if you deal with very high transaction volumes. You need the most robust and cheapest processing rates possible to stay profitable. Secondly, focus on digital wallets if you sell mostly to younger people on mobile phones.

Furthermore, invest in a gateway that supports global payments if you want to grow abroad. Also, make sure your wallet options include local favorites like UPI or AliPay. Lastly, monitor your search engine performance to see how checkout speed affects your traffic. Truly, the best focus is a balanced one that prioritizes the user experience above all else. It turns your payment process into a competitive advantage for your brand. This ensures that you stay ahead of other stores that are slower to change.

Best Practices: Optimizing Your Payment Flow

Building a great payment system is a journey that requires constant testing and updates. It needs a focus on making everything as simple as possible for the buyer. Clearly, the fewer clicks a user has to make, the more money you will earn. Therefore, follow these simple habits to keep your store at the top of its game.

Strategies for Long Term Payment Success

Firstly, always offer at least two or three digital wallet options. This gives your users a choice and makes them feel more comfortable. Secondly, choose a gateway with a very high uptime and fast processing speeds.

Furthermore, keep your checkout page clean and free of any distractions. Also, test your payment flow on every possible device to ensure it never breaks. Lastly, track your search engine metrics to see if your site speed is helping your rank. Truly, a great payment setup is the backbone of a healthy digital business. It builds trust with your audience and keeps your cash flow steady. This secures your growth and makes your business much more valuable over time.

Frequently Asked Questions (FAQs)

Q1: Can I use a digital wallet without a payment gateway?

No, a wallet only stores the user data. You still need a gateway to process that data and move the money from the bank to your account.

Q2: Does checkout speed affect my search engine ranking?

Yes, search engines like Google value fast websites. A slow checkout can lead to high bounce rates, which can hurt your overall ranking.

Q3: Which digital wallets are the most popular in 2026?

Apple Pay and Google Pay remain the global leaders, but regional wallets are becoming very important for international sales.

Q4: Are digital wallets safer for merchants than credit cards?

Yes, because they often use tokenization and biometrics, which significantly reduces the risk of chargebacks and fraud.

Q5: How do I know if my gateway is too slow?

You should monitor your cart abandonment rate. If many people leave at the final step, it may be because your gateway is taking too long to load.