The global financial map is shifting as physical cash turns into digital code. Central Bank Digital Currencies are no longer a future dream but a present reality. Specifically, the race to build a digital currency is a high-stakes game of power. Nations are moving away from old systems to gain a strategic edge. Therefore, understanding the rise of CBDCs is vital for any global observer. This change will redefine how countries trade and interact for decades. You will see a clear shift in influence by following this deep and technical trend.

China’s Lead and the Digital Yuan Push

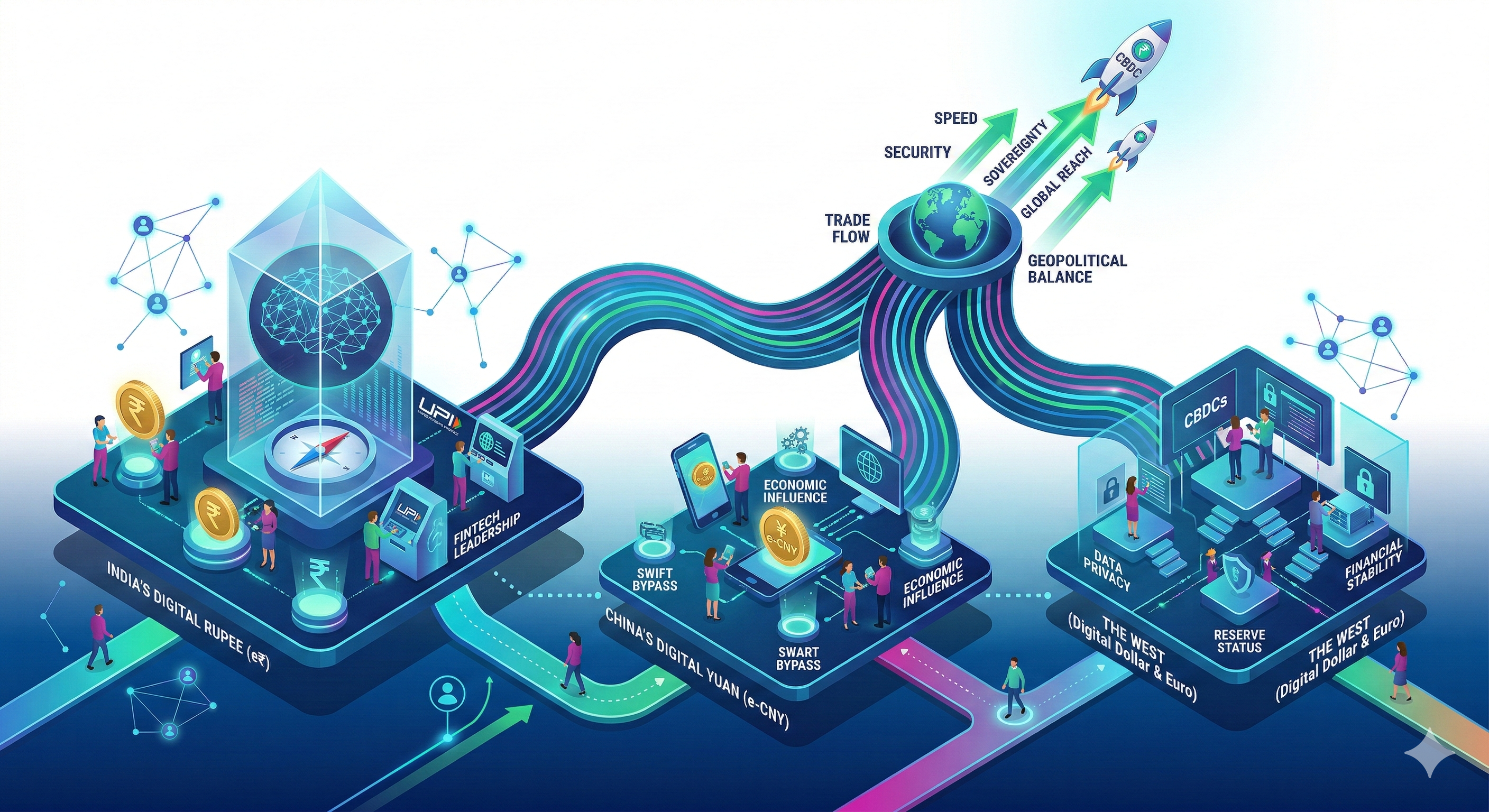

China is currently leading the race with its digital yuan, also known as the e-CNY. Specifically, the goal is to create a model for CBDCs that rivals the US dollar. By moving first, China can set the rules for how digital money flows across borders. Furthermore, this system allows them to bypass traditional Western banking networks like SWIFT. You might see a future where regional trade is settled entirely in digital yuan. This puts their economic growth on a very fast and independent path. Similarly, it acts as a tool of soft power to bring partners into their digital sphere.

India’s Digital Rupee and the UPI Success

India is taking a very smart and calculated path with its Digital Rupee. Building on the massive success of UPI, India seeks a strategy for CBDCs that balances innovation with safety. The Digital Rupee aims to reduce the high cost of printing and managing physical cash. Specifically, it offers a secure way for millions to join the formal economy instantly. Furthermore, India’s tech strength ensures that their system is both scalable and highly efficient. You should know that this move strengthens India’s spot as a global fintech leader. It ensures that the nation stays sovereign in a world of digital assets.

The West and the Struggle for the Digital Dollar

The West, led by the US and the Eurozone, is moving with more caution. There is a deep worry about how a shift toward CBDCs might affect privacy and bank stability. However, the risk of doing nothing is far too high for these major powers. If the US dollar loses its digital edge, it could lose its status as the world’s reserve currency. Therefore, the Federal Reserve and the ECB are testing systems that protect user data while staying fast. Specifically, they want a digital dollar that remains the gold standard for global trade. This journey is key to maintaining Western influence in the coming years.

The Impact on Global Trade and Sanctions

The rise of digital money changes how nations use economic pressure. In the past, blocking a country from global banks was a final and heavy blow. Now, a multi-polar world of CBDCs makes those blocks less effective. If two nations use a shared digital ledger, a third party cannot easily stop the flow. Furthermore, this leads to faster and cheaper cross-border payments for everyone. You will find that these tools reduce the friction of old money rules. Consequently, it sparks a new era of trade where speed is the ultimate advantage. This shift turns digital code into a real shield against foreign pressure.

FAQs

1 What exactly is a CBDC?

It is a digital form of a country’s national currency, issued and backed by the central bank.

2 How does it differ from Bitcoin?

Specifically, CBDCs are centralized and stable, while Bitcoin is private and its value changes often.

3 Can these digital coins replace the US dollar?

Indeed, if enough nations use different CBDCs for trade, the dollar’s global power could shrink.

4 Is my privacy safe with a digital rupee?

Central banks are building CBDCs that aim to balance your privacy with the need to stop financial crime.

5 Why is the race for these tools so fast?

Nations want to reduce their reliance on foreign systems and lead the future of global finance.

Read More:

How A Strong Payment Infrastructure Builds Global Soft Power