India’s subscription box market is booming. From beauty products to books, pet care to gourmet snacks — more Indian consumers are signing up for curated monthly boxes than ever before. But here’s the thing. Running a subscription box business is not just about great packaging or handpicked products. It’s also about getting paid — reliably, automatically, and on time, every single month. That’s exactly where a payment gateway becomes your most important business tool.

In this guide, we’ll walk you through everything you need to know. So, whether you’re just starting out or scaling fast, you’ll find the right payment solution for your subscription brand.

Why Payment Gateways Matter More for Subscription Boxes

First, let’s understand why this topic deserves special attention.

A standard e-commerce business collects a one-time payment. Simple. But a subscription box business collects recurring payments — weekly, monthly, or quarterly. That changes everything.

You need a gateway that supports:

- Automatic recurring billing

- Failed payment retries

- Subscription plan management

- Smooth UPI and wallet integration

- RBI-compliant e-mandate flows

Without these features, you’ll spend hours every month chasing payments manually. That’s not scalable. And it’s certainly not how successful brands operate.

Understanding How Recurring Payments Work in India

Before picking a gateway, it helps to understand the rules.

The Reserve Bank of India (RBI) introduced e-mandate guidelines for recurring transactions. Under these rules, customers must give explicit consent before auto-debits happen. For transactions above ₹15,000, additional authentication is required each time.

This framework protects customers. But it also means your payment gateway must be fully compliant with these regulations.

Fortunately, the top gateways in India have already built this into their systems. So, as long as you choose wisely, compliance won’t be a headache.

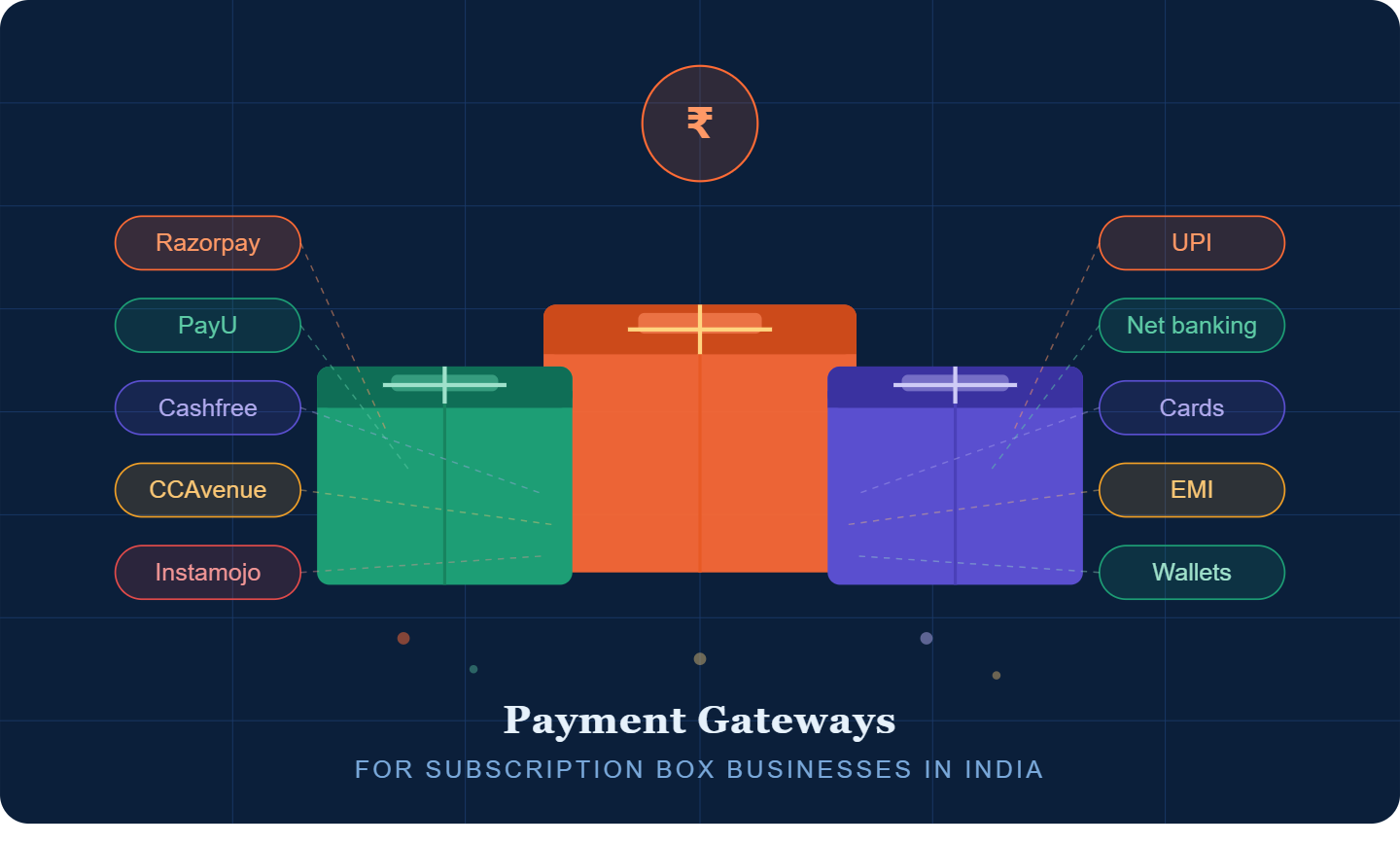

Top Payment Gateways for Subscription Box Businesses in India

Now, let’s get into the real comparison.

1. Razorpay — Best Overall for Subscription Businesses

Razorpay is arguably the most popular choice among Indian D2C brands. And for good reason.

It offers a dedicated Subscriptions API that lets you create flexible billing plans easily. You can set weekly, monthly, or annual cycles. Moreover, Razorpay handles failed payment retries automatically — a feature that dramatically reduces churn.

It also supports UPI AutoPay, which is a big deal in India right now. UPI AutoPay lets customers set up auto-debits without needing to enter their card details. This increases sign-up conversions significantly.

Additionally, Razorpay’s dashboard gives you clear visibility into active subscribers, upcoming renewals, and failed transactions. For growing brands, that kind of data is gold.

Transaction fees start at around 2% per transaction. For high-volume businesses, they offer custom pricing.

2. PayU — Great for Established Brands

PayU is another strong contender. It’s been in the Indian market for years, so its reliability is well-established.

PayU supports recurring billing through its subscription management tools. It also integrates smoothly with most popular e-commerce platforms like WooCommerce, Shopify, and Magento.

Furthermore, PayU offers one of the widest coverage of banks for net banking. This is useful if your customer base skews toward older demographics who prefer traditional banking over UPI.

However, PayU’s interface is not as modern as Razorpay’s. That said, its backend stability makes it a trusted choice for businesses processing higher volumes.

3. Cashfree Payments — Best for Fast Settlements

If cash flow is a priority — and for most small subscription brands, it absolutely is — then Cashfree deserves serious attention.

Cashfree offers same-day and next-day settlement options. That means the money your customers pay today can be in your account by tomorrow. For businesses with tight operating margins, this makes a real difference.

Cashfree also has strong subscription billing capabilities, including support for UPI AutoPay and e-NACH (electronic National Automated Clearing House) mandates. Its API is clean and developer-friendly, too.

In terms of pricing, Cashfree is competitive and transparent. It also offers a free plan for early-stage startups — something worth noting if you’re just launching.

4. CCAvenue — Best for Multiple Payment Options

CCAvenue has one of the widest arrays of payment options among Indian gateways. It supports over 200 payment modes. These include all major credit and debit cards, UPI, net banking across 58+ banks, EMI options, and digital wallets.

For subscription box businesses targeting a broad customer base — including tier 2 and tier 3 cities — this kind of coverage matters. Not everyone in India uses UPI or has a premium credit card. CCAvenue fills those gaps effectively.

Its recurring billing feature handles automated deductions. Moreover, it provides multi-currency support, which is useful if you plan to expand internationally.

One downside is that CCAvenue’s onboarding process can be slower compared to Razorpay or Cashfree. But once it’s set up, it’s a solid, stable platform.

5. Instamojo — Best for Small and Early-Stage Businesses

If you’re just starting your subscription box journey, Instamojo is worth exploring. It’s simple to set up. It requires minimal technical knowledge. And it’s designed specifically for small Indian businesses.

Instamojo lets you create payment links and basic subscription plans without writing a single line of code. So, for solopreneurs or bootstrapped founders, it offers a low-barrier entry point.

That said, it’s not ideal for high-volume or technically complex subscription models. As you scale, you’ll likely need to migrate to a more robust platform.

Key Features to Look for in a Subscription Payment Gateway

Beyond brand names, here are the features that truly matter when evaluating any gateway:

Recurring billing support. This is non-negotiable. Make sure the gateway handles automatic renewals without manual intervention.

RBI e-mandate compliance. Your gateway must support the latest RBI guidelines for recurring debit transactions. Non-compliant gateways create legal and operational risk.

UPI AutoPay integration. UPI is India’s dominant payment rail. AutoPay on UPI removes friction from the subscription sign-up process.

Retry logic for failed payments. Every subscription business deals with failed payments. Smart retry logic — where the system automatically reattempts the charge — dramatically reduces involuntary churn.

Webhook and API access. If you use a custom platform or CRM, you’ll need clean webhook support to sync payment events in real time.

Transparent pricing. Hidden fees eat into margins. Always read the fine print before committing to a gateway.

Common Mistakes to Avoid

Even experienced founders make avoidable payment mistakes. Here are a few to watch out for.

Many businesses underestimate failed payment rates. On average, 5–10% of recurring payments fail each cycle due to expired cards, insufficient funds, or bank issues. Without a retry mechanism, that’s revenue lost permanently.

Another common mistake is ignoring the checkout experience. A clunky, slow, or unfamiliar payment screen kills conversions. Always A/B test your checkout flow.

Finally, some brands delay setting up proper e-mandates. If you launch recurring billing without proper mandates in place, you risk RBI non-compliance — and that can freeze your payment processing entirely.

Which Gateway Should You Choose?

Here’s a quick way to think about it.

If you want an all-round solution with great subscription tools and UPI AutoPay, go with Razorpay and if cash flow is critical and you want fast settlements, choose Cashfree. But if you serve a wide, diverse customer base across India, CCAvenue covers more payment options or if you’re a small brand just starting out, Instamojo is the simplest entry point.

Ultimately, there’s no single right answer. The best payment gateway is the one that fits your business stage, tech stack, and customer base.

Final Thoughts

Running a subscription box business in India is exciting. The market is growing. Consumers are warming up to the model. And the tools available to founders today are better than ever.

But none of that matters if your payments fail, your billing is broken, or your customers churn because the renewal process is frustrating.

Your payment gateway is not a background tool. It’s the engine that keeps your subscription business alive.

So, choose it carefully. Set it up properly. And revisit the decision as your business grows.

Because when payments work seamlessly, everything else becomes a little easier.

Found this guide helpful? Share it with a fellow subscription brand founder who’s still figuring out their payment gateway stack.

Read More:

Regulatory Sandboxes for Fintechs: Opportunities & Risks in India