Choosing the right payment setup shapes your entire customer experience. This is why the local payment methods vs global gateways question matters so much today.

Businesses expanding into new markets face this decision constantly. Should you support local payment methods vs global gateways only? Or should you combine both approaches?

This guide explains the differences clearly. We will cover costs, customer trust, conversion rates, and practical recommendations. By the end, you will know exactly what to prioritize.

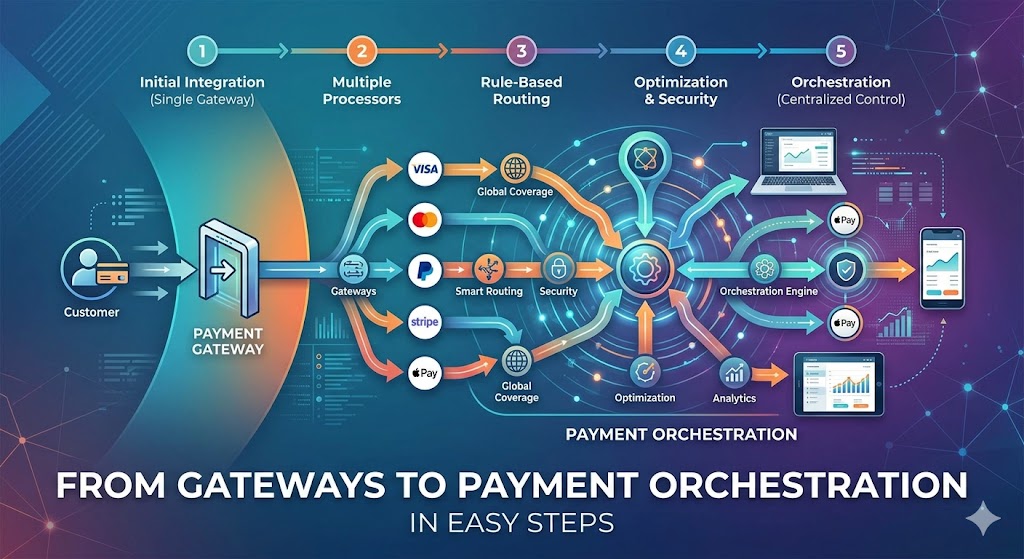

Understanding Local Payment Methods vs Global Gateways

Global gateways include well-known providers like Stripe, PayPal, and Adyen. They support credit cards and work across many countries.

Local payment methods, however, are region-specific. Examples include UPI in India, iDEAL in the Netherlands, and Pix in Brazil.

Many customers outside the United States rarely use credit cards. Instead, they prefer bank transfers, mobile wallets, or cash-based systems.

Therefore, relying only on global gateways can limit your reach significantly. Some customers simply cannot complete checkout without local options.

Meanwhile, global gateways offer simplicity and broad coverage. One integration often works across dozens of countries at once.

Why Local Payment Methods Matter for Conversion

Conversion rates depend heavily on payment familiarity. Customers trust payment methods they already use daily.

For instance, a shopper in Germany may abandon checkout without seeing SEPA transfer options. Similarly, Indonesian customers often expect e-wallet choices like GoPay.

As a result, ignoring local preferences can hurt sales directly. Studies consistently show higher cart abandonment when preferred methods are missing.

Additionally, local payment methods often reduce fraud risk. Bank-linked transfers require stronger identity verification than typical card payments.

Local methods also tend to settle faster in some regions. This improves cash flow for growing businesses significantly.

The Case for Global Gateways

Global gateways remain valuable for several reasons. They simplify technical integration across multiple markets.

Instead of connecting to dozens of local providers, you manage one system. This saves engineering time and reduces long-term maintenance work.

Global gateways also provide strong fraud protection tools. Their scale allows for advanced machine learning fraud detection.

Furthermore, they support recurring billing and subscription models smoothly. This matters greatly for SaaS companies and subscription services.

However, transaction fees can be higher with global providers. Currency conversion costs also add up for cross-border sales.

Local Payment Methods vs Global Gateways: Cost Comparison

Cost is a major factor in this decision. Global gateways typically charge a flat percentage per transaction.

Local payment methods often have lower fees within their home country. Bank transfers, for example, cost less than card processing.

Nevertheless, integrating many local methods can raise development costs upfront. You may need local partnerships or region-specific compliance work.

Consequently, businesses must weigh short-term integration costs against long-term savings. High transaction volume often justifies the initial investment.

Smaller businesses might start with a global gateway first. Then, they can add local options as specific markets grow.

How to Decide: Local Payment Methods vs Global Gateways

Start by analyzing your customer base carefully. Identify which countries generate the most traffic and revenue.

Next, research the dominant payment methods in those regions. Payment preference reports and industry data can guide this research.

Prioritize Local Options When

Your business targets specific high-growth markets. Local trust and conversion matter more than technical simplicity here.

Also prioritize local methods when card usage is low. Many Southeast Asian and Latin American markets fit this pattern.

Prioritize Global Gateways When

You need fast market entry across many countries at once. Simplicity and speed outweigh deep localization needs early on.

Global gateways also work well for subscription-based businesses. Recurring billing features save significant development time.

Consider a Hybrid Approach

Most successful global businesses use both options together. They start with a global gateway for broad coverage.

Then, they add popular local payment methods in key markets. This hybrid strategy balances simplicity with strong local conversion.

Payment orchestration platforms can help manage this hybrid setup. They route transactions intelligently between multiple providers automatically.

Regional Payment Preferences Worth Knowing

Different regions show very different payment habits. Understanding these patterns helps you prioritize correctly for each market.

Europe

European customers often prefer bank-based payments. iDEAL in the Netherlands and SEPA transfers across the region remain highly popular.

Additionally, Klarna and other buy-now-pay-later options continue growing quickly. These local preferences directly affect conversion rates.

Asia-Pacific

Mobile wallets dominate much of Asia-Pacific. Alipay and WeChat Pay lead in China, while GrabPay is common across Southeast Asia.

Meanwhile, UPI has become the standard in India for everyday transactions. Ignoring these options often means losing significant market share.

Latin America

Cash-based vouchers and installment payments remain popular across Latin America. Boleto in Brazil and OXXO in Mexico are common examples.

Pix has also grown rapidly as an instant payment method in Brazil. Businesses entering this region should prioritize these local options early.

Measuring the Impact of Payment Choices

Once you implement changes, track results carefully. Compare conversion rates before and after adding local payment methods.

Also monitor cart abandonment rates by country. A sudden drop after adding a local option confirms its value quickly.

Additionally, review customer support tickets related to payment issues. Fewer complaints often signal a smoother checkout experience.

Over time, this data helps refine your local payment methods vs global gateways strategy. You can double down on what works and remove what does not.

Conclusion

The local payment methods vs global gateways debate rarely has one universal answer. Your ideal strategy depends on your target markets and growth stage.

Global gateways offer speed, simplicity, and strong subscription support. Local payment methods build trust and boost conversion in specific regions.

Therefore, most growing businesses benefit from a hybrid approach eventually. Start broad, then localize where the data shows real demand.

Track conversion rates and abandonment closely after any change. This data will guide your next payment strategy decision effectively.

Working With Payment Providers Effectively

Building strong relationships with payment providers pays off long term. Ask providers directly about their local coverage and settlement times.

Additionally, negotiate transaction fees as your volume grows. Many providers offer better rates for higher processing volumes.

Request clear reporting dashboards from every provider you use. This makes it easier to compare performance across regions.

Also review provider uptime and reliability history. Payment failures during high traffic periods can cost significant revenue quickly.

Finally, revisit your provider mix annually. Markets change, and new local payment methods emerge regularly.

Future Trends in Global Payments

Payment preferences continue evolving rapidly worldwide. Real-time payment networks are expanding across more countries each year.

Meanwhile, regulatory changes continue shaping how businesses handle cross-border transactions. Staying informed helps you adapt quickly.

Digital wallets are also gaining ground even in previously card-dominant markets. This trend suggests local preferences will keep diversifying further.

Businesses that monitor these shifts closely will maintain a competitive edge. Flexibility remains essential in the payments landscape.

Security and Trust Signals at Checkout

Trust badges and recognizable payment logos improve customer confidence. Display these clearly near the checkout button.

Additionally, communicate your data protection practices briefly during checkout. This reassurance can reduce last-minute hesitation for new customers.

Handling Currency and Localization Details

Beyond payment methods, currency display matters greatly. Show prices in local currency whenever possible to reduce confusion.

Additionally, localize checkout language and support messaging. Small details like these build trust alongside the right payment options.

Consider local tax and invoicing requirements as well. Some markets expect specific receipt formats for business compliance.

Building a Checklist Before Launch

Before launching in a new market, create a simple checklist. List the top three payment methods customers expect locally.

Verify settlement currencies and timelines with each provider in advance. Confirm that refund and dispute processes work smoothly too.

Test the checkout flow thoroughly on both mobile and desktop devices. A smooth, fast checkout experience often matters as much as payment choice itself.

Frequently Asked Questions

1. What is the main difference between local payment methods and global gateways?

Local payment methods are region-specific options like bank transfers or e-wallets. Global gateways are broad platforms that support cards across many countries.

2. Do local payment methods really improve conversion rates?

Yes, customers convert more often when they see familiar payment options. Missing local methods frequently leads to cart abandonment.

3. Are global gateways more expensive than local payment methods?

Often, yes. Global gateways typically charge higher transaction fees, especially for cross-border and currency conversion transactions.

4. Should small businesses use global gateways or local payment methods first?

Most small businesses start with a global gateway for simplicity. They add local payment methods once specific markets show strong demand.

5. Can a business use local payment methods and global gateways together?

Yes, a hybrid approach is common and often recommended. It combines broad reach with strong local market conversion.

Read More:

Payment Localization: A Simple Breakdown for Stores