Digital payments in India have gone from a novelty to a necessity. Today, millions of people send money to friends, pay shopkeepers, and split bills — all within seconds, right from their phones. Three platforms stand at the center of this shift: WhatsApp Pay, Google Pay, and UPI Lite. Each one brings something different to the table. So, which one actually deserves a spot on your home screen?

In this blog, we break down these three P2P payment ecosystems side by side. Whether you care about speed, security, offline access, or just ease of use — this guide covers it all.

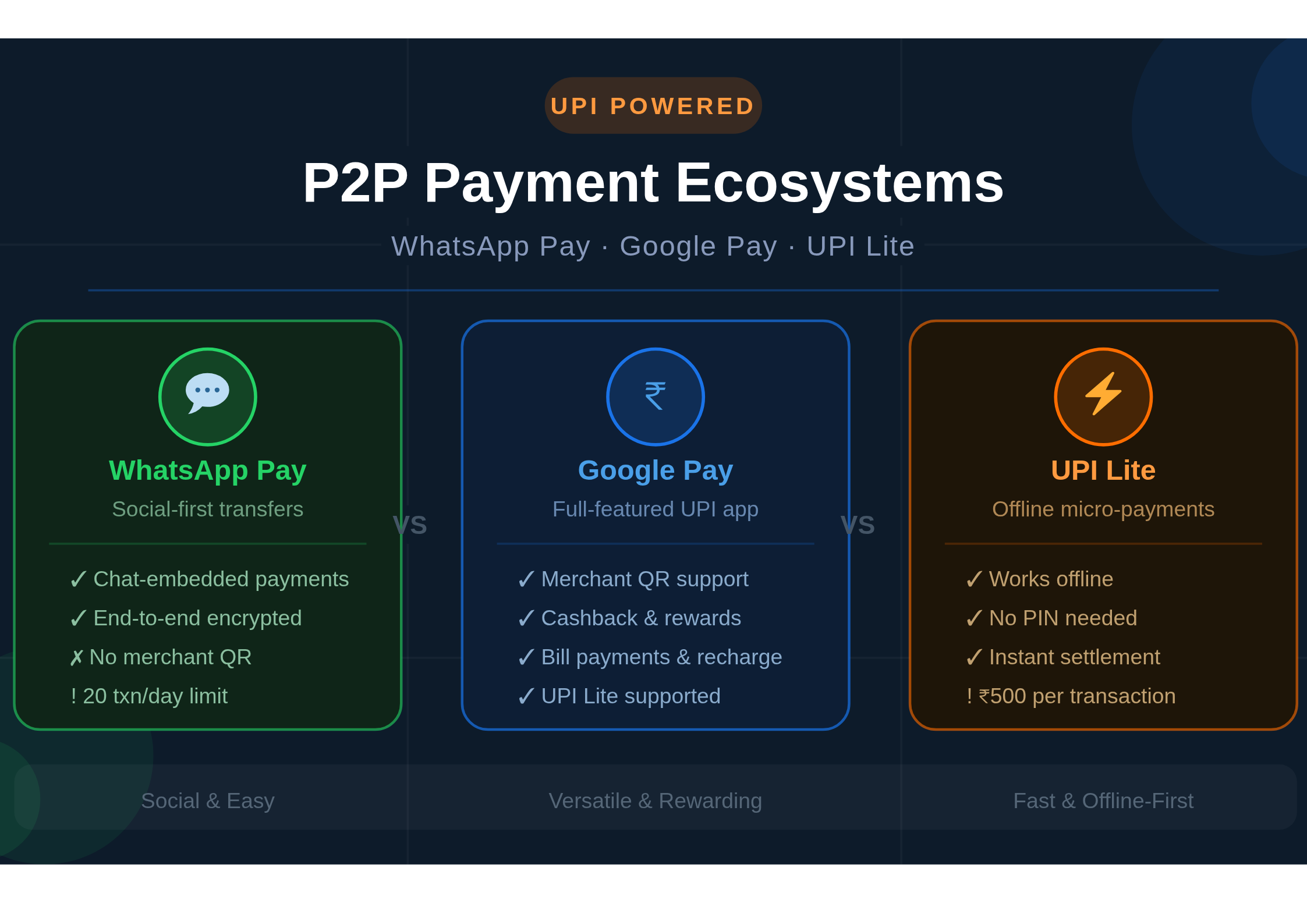

What Is a P2P Payment Ecosystem?

Peer-to-peer (P2P) payments allow users to transfer money directly from one bank account to another — no middleman, no waiting, no paperwork. In India, the Unified Payments Interface (UPI) powers most of these transactions. It is built and regulated by the National Payments Corporation of India (NPCI).

Therefore, apps like WhatsApp Pay and Google Pay do not move money on their own. Instead, they ride on top of the UPI infrastructure. UPI Lite, however, is a distinct layer that handles smaller, low-value transactions differently. Understanding this difference is key to choosing the right tool.

Google Pay: The Power Player

Google Pay (formerly Tez) launched in India in 2017. It quickly became one of the most downloaded UPI apps in the country. Even today, it holds a massive market share — and for good reason.

Key Features

Google Pay supports multiple UPI IDs and bank accounts. Users can link up to four bank accounts at once. Consequently, switching between accounts during a payment is easy. The app also supports bill payments, mobile recharges, and merchant QR code scanning.

Moreover, Google Pay uses a layered security model. Every transaction requires a UPI PIN. The app also features a “Safe” area that hides your payment history and account details behind an extra lock. This gives cautious users an added sense of control.

Additionally, the Nearby feature lets users discover and pay nearby businesses quickly. The rewards program — with scratch cards and cashback offers — has long been a crowd-pleaser. Furthermore, Google Pay integrates neatly with other Google services like Gmail and Google Assistant.

Limitations

On the downside, Google Pay requires internet access for every transaction. It also does not support in-app chat or social features. For users who want a more all-in-one experience, this can feel limiting.

WhatsApp Pay: The Social Payment Shortcut

WhatsApp Pay entered the Indian market after a long regulatory battle. Launched fully in 2020, it is now available to over 500 million WhatsApp users in India. The core idea is simple — pay someone directly inside a chat window.

Key Features

WhatsApp Pay is deeply embedded in the messaging experience. To send money, you simply open a chat, tap the attachment icon, and select Payment. As a result, paying someone feels as natural as sending a sticker or a voice note.

The platform supports all major Indian banks and uses UPI for fund transfers. Notably, it also stores transaction history within the chat thread — so you always know who paid whom and when. This makes it especially useful for splitting expenses among friends or family.

From a security standpoint, WhatsApp Pay is compliant with NPCI’s data localization norms. It uses end-to-end encryption for messages and a separate UPI PIN for payments. Nevertheless, some privacy advocates remain cautious about Meta’s data practices.

Limitations

WhatsApp Pay currently caps total UPI transactions at 20 per day, which is lower than Google Pay. It also lacks support for merchant QR codes at the moment. Similarly, advanced features like scheduled payments or bill splitting tools are absent. Still, for casual money transfers within a social circle, it is hard to beat.

UPI Lite: The Offline Game-Changer

UPI Lite is not exactly an app — it is a feature within UPI-enabled apps. Launched by NPCI in 2022, it addresses one of the biggest pain points of digital payments in India: poor network connectivity.

How It Works

UPI Lite works by pre-loading a small amount of money — up to ₹2,000 — into an on-device wallet. From there, you can make payments of up to ₹500 per transaction without needing internet access or a UPI PIN. Each transaction settles instantly on the device, and bank reconciliation happens later in the background.

Consequently, UPI Lite is perfect for small, everyday purchases — a chai at a roadside stall, a newspaper, an auto-rickshaw fare. Because it skips the usual server verification step, transactions process much faster than standard UPI payments.

Availability

Currently, UPI Lite is supported within Google Pay, Paytm, and several bank apps. WhatsApp Pay does not yet offer UPI Lite support, which is a notable gap. However, NPCI plans to expand compatibility across more platforms in the near future.

Limitations

The wallet cap of ₹2,000 limits its use for higher-value transactions. Additionally, users must manually top up the wallet, which can be a minor inconvenience. That said, for micro-transactions in low-connectivity areas, UPI Lite is a genuine breakthrough.

Head-to-Head Comparison

Here is a quick snapshot of how the three platforms stack up against each other:

| Feature | Google Pay | WhatsApp Pay | UPI Lite |

| UPI Support | ✅ Full | ✅ Full | ✅ Lite Only |

| Offline Payments | ❌ No | ❌ No | ✅ Yes |

| Social Integration | ❌ Limited | ✅ Strong | ❌ None |

| Merchant QR | ✅ Yes | ❌ No | ✅ Yes |

| Transaction Limit | ₹1 Lakh/day | ₹1 Lakh/day | ₹500/txn |

| Daily Txn Count | Unlimited | 20 per day | Unlimited |

| PIN Required | ✅ Yes | ✅ Yes | ❌ No |

| Cashback/Rewards | ✅ Yes | ❌ Limited | ❌ No |

Security: How Safe Is Your Money?

Security is a top concern for any digital payment user — and rightfully so. Fortunately, all three platforms operate under RBI and NPCI guidelines, which means they follow strict data handling and fraud prevention standards.

Google Pay uses device-level security, including fingerprint and face recognition. WhatsApp Pay benefits from end-to-end encryption at the messaging layer. UPI Lite, meanwhile, removes the PIN requirement for small transactions — which speeds things up but also shifts responsibility to the user. Therefore, always keep your phone locked when not in use.

Regardless of which app you use, never share your UPI PIN with anyone. Be cautious of collect requests from unknown contacts. And always verify the recipient’s name before hitting confirm.

Which One Should You Use?

The best P2P payment app depends entirely on your lifestyle and needs. Here is a simple breakdown:

Choose Google Pay if you want a full-featured UPI app with cashback rewards, bill payments, and merchant support. It is the most versatile option overall.

Choose WhatsApp Pay if you frequently transfer money to friends and family who are already on WhatsApp. The conversational payment flow is smooth and social.

Use UPI Lite if you make lots of small, everyday payments and live in an area with spotty internet. It is the fastest and most friction-free option for micro-transactions.

In practice, many users rely on more than one. For example, you might use UPI Lite for buying street food, Google Pay for utility bills, and WhatsApp Pay to split dinner with friends. There is no rule that says you must pick just one.

The Future of P2P Payments in India

India’s digital payment sector is growing at a breakneck pace. UPI processed over 13 billion transactions in a single month in 2024. As a result, competition among payment apps is intensifying. Going forward, expect to see smarter AI-driven fraud detection, expanded UPI Lite limits, and deeper integration with e-commerce platforms.

WhatsApp Pay is likely to roll out merchant payment features as Meta expands its Commerce ecosystem in India. Similarly, Google Pay is investing heavily in credit products and BNPL (Buy Now Pay Later) integrations. Meanwhile, NPCI is working on UPI One World — a version designed for foreign visitors to India.

Ultimately, the winner of this race will not be determined by features alone. Trust, simplicity, and network reach will decide which app becomes the default choice for the next billion users.

Final Thoughts

P2P payments are no longer just a convenience — they are the backbone of everyday financial life in India. WhatsApp Pay brings payments into conversations. Google Pay brings rewards and versatility. UPI Lite brings speed and offline access to places that were previously left out. Each platform has carved out its own niche. Together, they are reshaping how a billion people think about money. So go ahead — try all three, see what fits, and take full advantage of India’s world-class digital payments infrastructure.

Read More:

Everything You Need to Know About Payment Gateway Before Launching Your Subscription Box

Regulatory Sandboxes for Fintechs: Opportunities & Risks in India