Cart abandonment is a massive problem for online stores. Studies consistently show that checkout friction is one of the top reasons shoppers leave without buying. One of the biggest friction points is the checkout type you offer. Guest checkout and account-based checkout each come with real trade-offs. One prioritizes speed. The other prioritizes relationship-building. Knowing which one converts better for your store depends on several factors. This guide breaks down both options clearly. You will understand the conversion impact of each, when to use them, and how to optimize your checkout experience to increase revenue.

Understanding Guest Checkout

Guest checkout allows shoppers to complete a purchase without creating an account. They enter their details, pay, and they are done. There is no password to set. No profile to fill out. No confirmation email asking them to verify an account. This process is fast. It is also frictionless by design. For first-time buyers, especially impulse shoppers, this is ideal. Research from the Baymard Institute has shown that requiring account creation is one of the leading causes of checkout abandonment. Furthermore, many shoppers simply distrust creating accounts with brands they have never purchased from before. Guest checkout removes that barrier entirely. It puts the transaction first and the relationship second. For many ecommerce businesses, that sequence converts better.

Understanding Account-Based Checkout

Account-based checkout requires the shopper to log in or register before completing a purchase. This process captures customer data. It enables personalization. It makes repeat purchases easier through saved addresses and payment methods. For businesses focused on long-term customer lifetime value, this model has clear advantages. Similarly, loyalty programs, wishlist features, and personalized recommendations all depend on account data. Without it, delivering a tailored experience becomes harder. However, the trade-off is friction at the moment of purchase. A shopper who hits a mandatory registration wall may simply leave and buy from a competitor. That is a real conversion cost. Therefore, the business goal must be weighed carefully against the checkout experience.

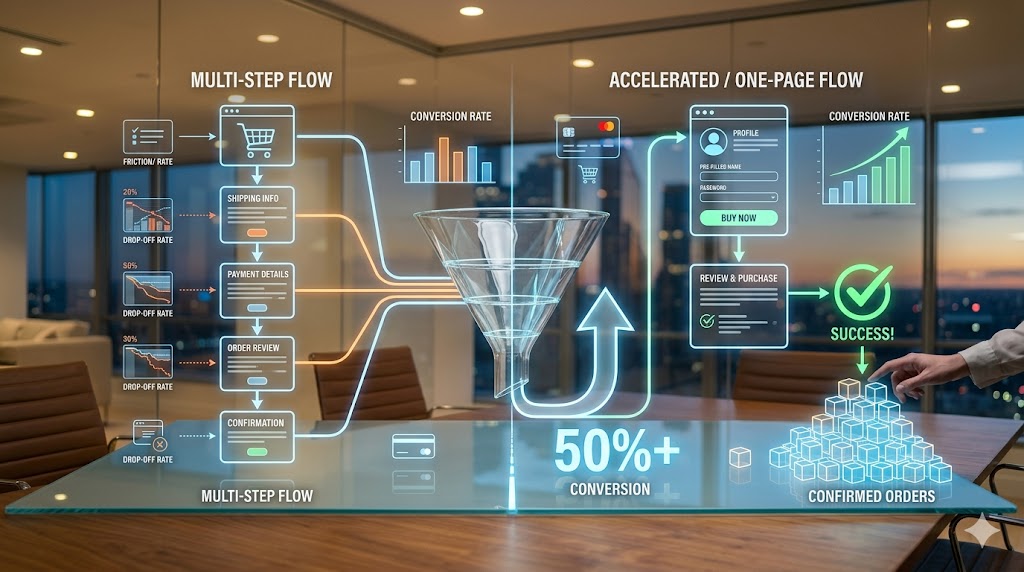

What the Conversion Data Shows

Multiple studies point to the same conclusion. Guest checkout typically wins on first conversion rate. Allowing guest checkout reduces abandonment and increases completed transactions, especially for new visitors. However, account-based checkout tends to win on customer lifetime value. Returning customers who have accounts spend more over time. They benefit from faster checkouts on repeat visits. They are also easier to re-engage through email marketing. As a result, the answer is not simply one or the other. The smarter approach is a hybrid model. Let shoppers choose their path. Offer guest checkout as the default. Then present a soft option to create an account after the purchase is complete. This sequence reduces friction while still building your customer database.

How to Implement a Hybrid Checkout Strategy

A hybrid checkout strategy balances conversion rate with long-term retention. Here is how to do it effectively. First, make guest checkout the default option. Place it prominently. Do not hide it behind a login form. Second, use a social login option. Allowing customers to sign in with Google or Apple reduces friction significantly. Many shoppers are comfortable with this. Third, after checkout, send a post-purchase email. Include a one-click option to set a password and activate an account. This converts guest buyers into account holders without adding checkout friction.

Additionally, offer a clear value exchange. Tell shoppers exactly what they get by creating an account. Faster future checkouts, order tracking, exclusive deals. Give them a reason to register. Consequently, more of your guest buyers will convert to account holders over time.

Factors That Influence Which Checkout Type Works Best

Your audience matters enormously. Younger, mobile-first shoppers often prefer guest checkout. They shop quickly and impulsively. Older shoppers who return frequently may prefer the convenience of an account. Product type also plays a role. High-consideration purchases, like electronics or furniture, attract shoppers who research carefully. These buyers are often more comfortable creating accounts. In contrast, commodity purchases like clothing or home goods attract impulsive buyers who want speed. Furthermore, your marketing strategy matters. If you rely heavily on email campaigns and remarketing, account data is essential. If your acquisition is mostly one-time campaign traffic, guest checkout may serve you better. Always test both options with your specific audience before drawing conclusions.

Optimizing Checkout for Maximum Conversion

Regardless of checkout type, the checkout experience itself must be clean and fast. Here are proven optimization principles. Keep the checkout to as few steps as possible. Each additional step costs conversions. Use progress indicators so shoppers know how close they are to finishing. Offer multiple payment options including digital wallets. Apple Pay and Google Pay are trusted and fast. Moreover, display security badges clearly. Trust signals reduce anxiety at the payment stage. Make sure your checkout works perfectly on mobile. More than half of ecommerce traffic now comes from mobile devices. Test your checkout regularly. Run A/B tests on button text, form length, and page layout. Small changes often produce significant conversion improvements.

Conclusion

Guest checkout vs account-based checkout is not a simple either/or decision. Both serve different purposes at different stages of the customer relationship. Guest checkout wins on first-time conversion. Account-based checkout wins on long-term customer value. The most effective ecommerce businesses use both. They offer guest checkout by default and invite account creation after the sale. This approach reduces friction at the point of purchase while building a valuable customer database for retention and personalization. Optimize your checkout experience continuously. Test, measure, and improve. Your checkout page is one of the highest-impact areas of your entire ecommerce operation.

Frequently Asked Questions

1 Does guest checkout really improve conversion rates?

Yes. Guest checkout consistently reduces cart abandonment. Removing mandatory registration lowers friction and increases completed purchases, especially from first-time visitors.

2 What are the downsides of guest checkout for ecommerce stores?

Guest checkout limits your ability to build a customer database. Without account data, personalization, loyalty programs, and targeted email marketing become harder to execute.

3 How can I convert guest buyers into account holders?

Send a post-purchase email with a one-click account setup option. Highlight clear benefits like faster checkout and order tracking. This approach converts many guests without adding friction at checkout.

4 Should I force account creation for high-value purchases?

No. Even for high-value purchases, mandatory registration increases abandonment risk. Instead, offer optional account creation after the sale is complete.

5 What is the best checkout strategy for a new ecommerce store?

Start with guest checkout as the default option alongside optional social login. After purchase, invite customers to create an account. This hybrid approach maximizes both conversion and customer data collection.

Read More:

Payment UX Audit Checklist for Better Results