Every second counts in financial transactions. Slow payments frustrate customers, delay cash flow, and drive revenue losses. Reducing payment latency is no longer just a technical concern. It is a core business strategy. Companies that process payments faster gain a clear advantage. They close more sales, keep more customers, and manage cash more effectively. This guide explains what payment latency is, why it matters, and what businesses can do about it.

What Is Payment Latency and Why Does It Matter?

Payment latency refers to the time delay between when a payment is initiated and when it is confirmed or settled. In simple terms, it is the wait time in a transaction. This delay can happen at multiple points in the payment process.

For consumers, latency means waiting for a payment to go through. For businesses, it means waiting for funds to appear in their accounts. Additionally, long wait times at checkout can cause customers to abandon their purchases entirely.

Studies show that even minor delays in payment processing affect conversion rates. A one-second delay in checkout can reduce conversions by up to 7 percent. Therefore, payment speed directly ties to revenue performance. Businesses that ignore latency risks are quietly losing money.

How Payment Latency Affects Customer Experience

Customer experience is shaped by convenience and speed. When payments are fast and seamless, customers feel confident. When payments are slow or fail, frustration sets in quickly.

Slow checkouts are one of the top reasons for cart abandonment in e-commerce. Customers expect instant results. If a payment takes too long to process, they may assume something went wrong. As a result, they cancel the transaction or go elsewhere.

Loyalty is also affected. A customer who experiences repeated payment delays is unlikely to return. In contrast, businesses that offer fast, frictionless payment experiences see higher repeat purchase rates. Furthermore, positive payment experiences drive word-of-mouth referrals, which are among the most valuable forms of marketing.

Mobile payments have raised expectations even higher. Users expect tap-to-pay to work instantly. Any lag feels like a system failure. Consequently, reducing latency in mobile payment channels is now a priority for businesses serving digital-first customers.

The Revenue Cost of Slow Payment Processing

Payment latency has a direct and measurable impact on revenue. First, it causes transaction failures. When processing takes too long, session timeouts occur. Customers are forced to re-enter payment details, and many do not bother.

Second, delayed settlement affects cash flow. When funds take days to appear in a business account, that business cannot invest or operate as efficiently. Small businesses are especially vulnerable. Slow settlement can mean delayed payroll, missed supplier payments, or missed investment opportunities.

Third, high latency increases the cost of payment operations. When transactions fail or require manual review, staff time and resources are consumed. Moreover, failed transactions often lead to customer service calls, increasing operational costs further.

Real-time payment systems solve many of these problems. They settle transactions in seconds rather than days. Businesses gain access to funds immediately, which improves their financial agility. Similarly, customers receive instant confirmation, which builds trust and encourages repeat business.

Technology Solutions for Reducing Payment Latency

Several modern technologies help businesses reduce payment latency significantly. Understanding these options helps companies choose the right approach for their needs.

Real-Time Gross Settlement systems, or RTGS, allow large-value payments to be settled instantly. Many central banks now offer real-time payment rails that businesses can access through their banking partners. These systems eliminate the batch processing delays common in traditional banking.

Application Programming Interfaces, or APIs, also play a key role. Payment APIs connect merchants directly to payment networks, reducing intermediary steps. Fewer intermediaries mean fewer points of delay. Additionally, API-based payment systems are easier to update and optimize.

Tokenization speeds up recurring payments. It replaces sensitive card data with a unique identifier. When a returning customer pays, the system uses the stored token instead of asking for card details again. Consequently, checkout is faster and more secure.

Edge computing brings data processing closer to the end user. Instead of sending payment data to a central server far away, edge computing processes it locally. This dramatically reduces the time it takes to complete a transaction.

The Role of Fintech in Payment Speed

Fintech companies are pushing the boundaries of what is possible in payment processing. They build solutions specifically designed to eliminate friction and reduce latency. Many traditional banks have partnered with fintechs to modernize their payment infrastructure.

Buy Now Pay Later platforms, digital wallets, and instant bank transfers are all fintech innovations that prioritize speed. Furthermore, blockchain-based payment systems offer near-instant cross-border settlement without the traditional three-to-five day wait.

For merchants, choosing the right payment processor is critical. Not all processors are equal in speed or reliability. Some prioritize throughput and real-time settlement. Others are built for high transaction volumes but sacrifice speed. Therefore, businesses should evaluate processors based on their specific revenue and cash flow needs.

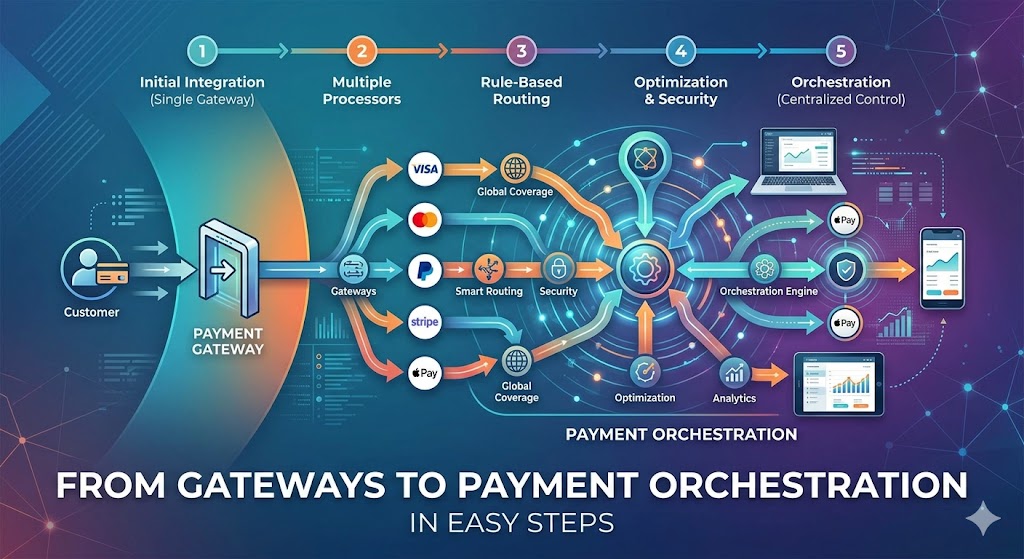

Payment orchestration platforms are another emerging solution. They route transactions through the best available payment gateway based on speed, cost, and success rate. This reduces latency without requiring businesses to manage multiple payment integrations themselves.

Best Practices to Reduce Payment Latency

Reducing payment latency requires both technology and process improvements. Here are the most effective strategies businesses use today.

First, upgrade payment infrastructure. Legacy systems are often the biggest source of latency. Moving to modern, cloud-based payment platforms reduces delays significantly. Additionally, cloud systems are more scalable and easier to maintain.

Second, minimize payment steps. Every extra step in the checkout process adds time and increases drop-off risk. Streamline the payment flow by reducing required fields and offering one-click payment options for returning customers.

Third, use intelligent payment routing. Route transactions through the fastest and most reliable gateway available. Payment orchestration tools do this automatically. As a result, merchants see higher approval rates and lower failure rates.

Fourth, monitor transaction performance continuously. Use analytics to track payment processing times, failure rates, and bottlenecks. When issues appear, address them immediately. Furthermore, regular performance audits help businesses stay ahead of latency problems before they affect revenue.

Fifth, offer multiple payment methods. Different payment methods have different processing speeds. Giving customers options ensures they can choose the fastest path to completion.

Conclusion

Payment speed is a revenue driver, not just a technical metric. Reducing payment latency improves customer experience, boosts conversion rates, and strengthens cash flow. The technology to achieve this is widely available and increasingly affordable. Businesses that invest in faster payment systems gain a real competitive edge. The cost of inaction is clear: slower payments mean fewer completed transactions, frustrated customers, and lost revenue. Act now to make payment speed a strategic priority.

Frequently Asked Questions

- What causes payment latency in businesses?

Payment latency is caused by factors such as legacy payment systems, multiple intermediaries in the transaction chain, network delays, batch processing schedules, and insufficient payment infrastructure. - How does payment latency affect e-commerce revenue?

Slow payment processing leads to cart abandonment, transaction failures, and poor customer experience, all of which directly reduce e-commerce sales and long-term customer retention. - What is real-time payment processing?

Real-time payment processing refers to transaction systems that initiate, authorize, and settle payments within seconds, giving both businesses and customers instant confirmation of completed transfers. - Which technologies best reduce payment latency?

Real-time payment rails, payment APIs, tokenization, edge computing, and payment orchestration platforms are among the most effective technologies for reducing payment processing delays. - How can small businesses reduce payment latency on a limited budget?

Small businesses can start by choosing a modern payment processor with fast settlement times, simplifying their checkout process, and using digital wallets or mobile payment options that are built for speed.

Read More:

Conversion Rate Secrets Hidden in Payment Methods