Shopping has changed. Customers buy on websites, apps, smart TVs, voice assistants, and even in-store kiosks. Traditional ecommerce platforms struggle to keep up. Headless commerce solves this problem. It separates the front end from the back end, giving brands the freedom to build any experience they want.

When you add headless payments to the mix, checkout becomes just as flexible as the rest of the store. The result is a faster, smoother, more customizable buying journey.

What Is Headless Commerce?

Traditional ecommerce platforms bundle everything together. The storefront, the cart, the checkout, and the back-end logic all live in one system. Changing one part often breaks another.

Headless commerce breaks this bundle apart. The front end, what customers see, connects to the back end through APIs. Developers can build any front-end experience without touching the commerce engine underneath.

Therefore, brands gain creative freedom. They can design unique storefronts for every channel. They can update the look without disrupting business logic. This separation is the core of headless architecture.

Why Payments Needed to Go Headless Too?

For years, checkout was the last thing brands customised. Payment forms were rigid. Styling was limited. Adding new payment methods took months of development work. This mattered because checkout is where buyers convert or abandon. A clunky payment experience kills sales. Even a one-second delay raises cart abandonment rates significantly.

Consequently, headless payments emerged as a natural extension of headless commerce. By decoupling the payment layer, brands control every pixel of the checkout experience. The also integrate new payment methods in days, not months.

How Headless Payments Work?

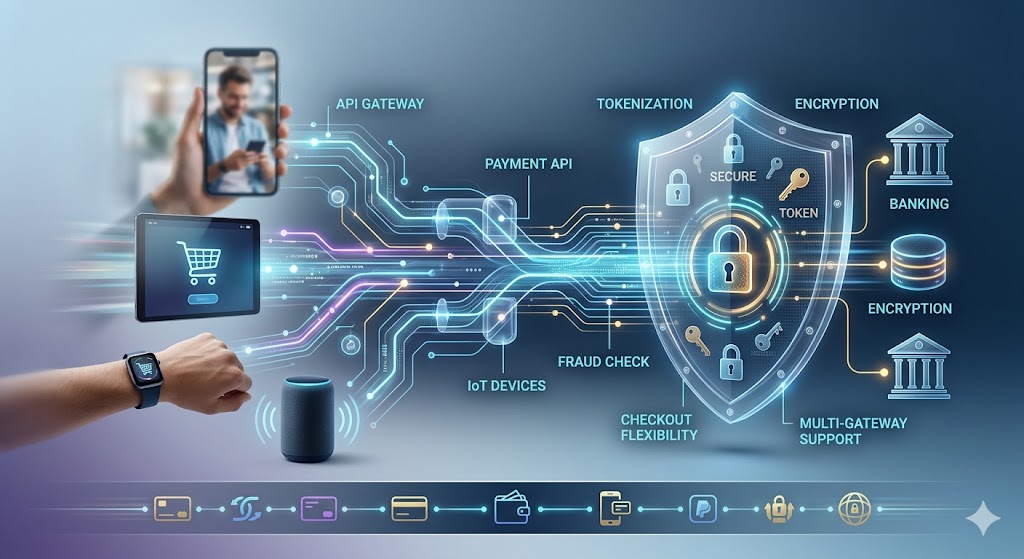

Headless payment solutions expose payment functionality through APIs. The brand builds its own checkout UI. The payment processor handles the sensitive data underneath.

Tokenisation keeps cardholder data secure. The front end never actually sees raw card numbers. Instead, it passes a token to the payment processor, which completes the transaction.

Additionally, webhooks notify the front end when a payment succeeds or fails. This allows real-time feedback without a page refresh. The result feels fast and modern to the customer.

Key Benefits of Decoupling Checkout

First, speed improves dramatically. Custom-built checkout pages load faster than bloated, all-in-one platform templates. Faster pages mean higher conversion rates.

Second, localisation becomes easy. Different markets want different payment methods. Brazil favours Boleto. Germany prefers SEPA. The Netherlands uses iDEAL. Headless architecture lets you plug in local methods for each region.

Third, A/B testing checkout flows becomes straightforward. You can test button colours, form layouts, and step sequences without touching the payment engine. Data drives optimisation.

Furthermore, brand consistency extends all the way through checkout. No more jarring redirects to generic payment pages. The customer stays in your branded environment from browse to buy.

Popular Headless Payment Providers

Stripe leads the field. Its Payment Intents API gives developers granular control over the payment flow. Stripe Elements provides pre-built, customisable UI components.

Adyen serves enterprise brands. It supports over 200 payment methods and provides deep reporting tools. Its Checkout API enables fully custom experiences. Braintree, owned by PayPal, focuses on flexibility and developer experience. It supports cards, PayPal, Venmo, and local payment methods through a single integration.

Moreover, newer players like Primer and Gr4vy act as payment orchestration layers. They sit above multiple payment processors, routing transactions to the best provider for each situation.

Composable Commerce: The Bigger Picture

Headless commerce and headless payments are part of a larger movement called composable commerce. Instead of one monolithic platform, composable commerce assembles best-of-breed solutions.

A brand might use Contentful for content management, Commerce tools for commerce logic, Stripe for payments, and Algolia for search. Each piece excels at its function. APIs connect them all.

This approach follows the MACH architecture principles: Microservices, API-first, Cloud-native, and Headless. MACH brands move faster, innovate more, and adapt to market changes without major re-platforming projects.

However, composable commerce also adds complexity. More vendors mean more integrations to maintain. Strong engineering teams and clear governance are therefore essential.

Challenges of Going Headless

Headless is powerful but not simple. Building a custom front end requires skilled developers. Maintaining API integrations demands ongoing effort. Costs can rise quickly without careful planning.

Security is another concern. More API connections create more potential attack surfaces. Each integration point needs proper authentication, encryption, and monitoring.

PCI DSS compliance also needs attention. Payment card industry standards govern how cardholder data is handled. Headless architectures must still meet these requirements, even when data never touches the front end directly.

Despite these challenges, the benefits typically outweigh the costs for brands at scale. Smaller brands may prefer managed headless solutions that reduce engineering overhead.

Conversion Optimisation Through Headless Checkout

One-page checkout reduces friction. Progressive disclosure only shows form fields when needed. Auto-fill speeds up the process for returning customers.

Buy Now Pay Later (BNPL) options like Klarna and Afterpay increase average order values. Adding them to headless checkout is a simple API call. The brand does not need to manage credit risk.

Express checkout options also matter greatly. Apple Pay, Google Pay, and PayPal Express let customers skip form filling entirely. Conversion rates rise sharply when fewer steps stand between desire and purchase.

Additionally, smart payment routing improves authorisation rates. Sending a transaction to the processor most likely to approve it reduces false declines. Every false decline is a lost sale.

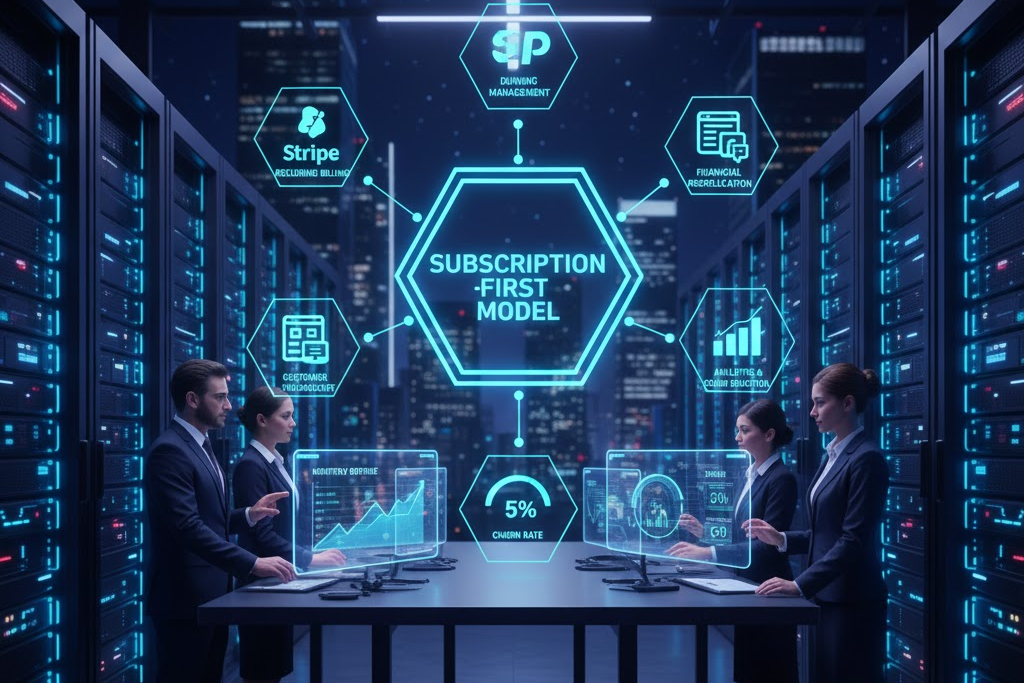

Subscription and Recurring Payments in Headless Architecture

Subscription commerce is booming. Software, groceries, beauty products, and media all use recurring billing models. Headless architecture supports subscriptions elegantly.

Payment processors like Stripe Billing and Recurly handle the subscription logic. The headless front end simply calls the API to create, update, or cancel subscriptions.

Dunning management, the process of retrying failed payments, happens automatically in the background. Customers see a smooth experience. Finance teams see fewer failed charges.

Furthermore, subscription analytics feed back into the front-end experience. Churn prediction data can trigger personalised retention offers at exactly the right moment.

The Future of Headless Commerce and Payments

Embedded finance is the next frontier. Soon, brands will offer banking, insurance, and credit products directly within their own platforms. Headless architecture makes this possible without rebuilding from scratch.

Artificial intelligence will personalise checkout in real time. Dynamic payment method presentation will show each customer the option they are most likely to use. Fraud scoring will happen invisibly in milliseconds.

Cryptocurrency and digital wallets continue to grow. Headless payment layers can integrate these new methods without disrupting existing checkout flows.

Ultimately, the brands that invest in headless commerce and payments today are building the infrastructure for tomorrow’s retail landscape.

Conclusion

Headless commerce and payments give brands something traditional platforms never could: true flexibility. Every channel, every market, and every customer segment gets an experience built specifically for it.

The technical investment is real. However, the commercial return is compelling. Faster checkout, higher conversion, and seamless localisation all flow from a well-executed headless strategy.

Start small if needed. Decouple one part of your stack. Learn. Then expand. The journey to composable commerce is worth every step.

Read More:

Fintech Relies on Microservices-Based Infrastructure Now