Every failed payment costs money. It costs the transaction, the customer, and sometimes the relationship. Smart payment routing logic changes that. It sends each transaction through the best possible path — automatically and in real time.

This blog explains how routing logic works, why it matters, and how businesses use it to dramatically improve payment success rates.

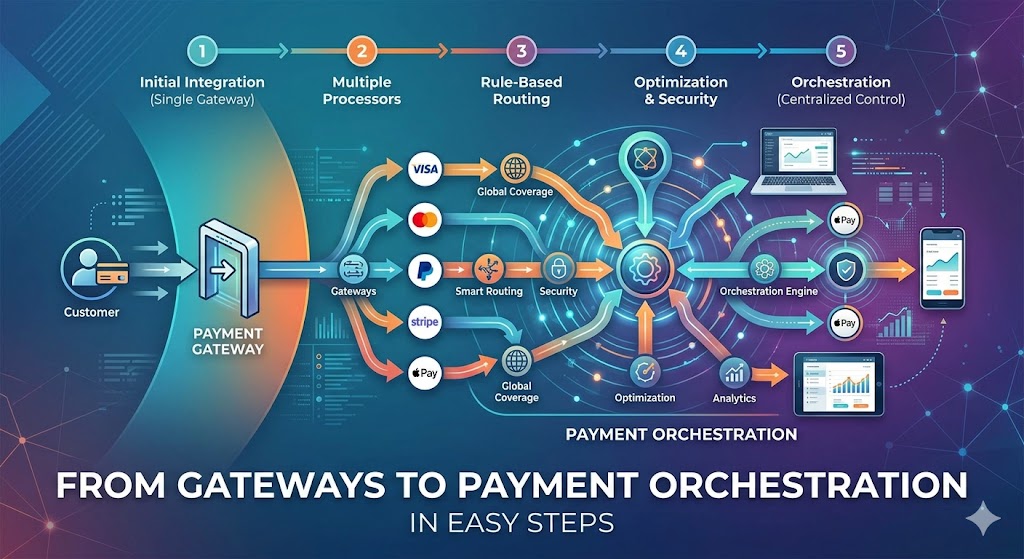

What Is Payment Routing Logic?

Payment routing logic is the set of rules that determines which payment processor handles a given transaction. Every payment involves multiple parties — the merchant, the payment gateway, the processor, the card network, and the issuing bank. When a transaction fails, it usually fails at one of these points.

Smart routing logic evaluates each transaction before sending it. Furthermore, it considers factors like card type, geography, transaction size, and processor performance history. Based on these factors, it selects the processor most likely to approve the payment.

Think of it like GPS for payments. Instead of always taking the same route, it calculates the fastest, most reliable path in real time. Consequently, more payments reach their destination successfully.

Why Payment Failures Happen

Understanding failures is essential before solving them. Payments fail for several reasons. Soft declines happen when the issuing bank temporarily rejects a transaction. These include insufficient funds, suspected fraud flags, or processor downtime. Importantly, soft declines can often be recovered with a retry on a different processor.

Hard declines are permanent rejections. Expired cards, closed accounts, and confirmed fraud fall into this category. No amount of rerouting will recover these. Processor-side failures occur when a payment gateway or processor experiences outages or connectivity issues. Consequently, perfectly valid transactions get rejected for technical reasons unrelated to the customer.

Network routing issues happen when card networks route transactions sub-optimally. Different networks have different approval rates for different card types and geographies. Smart routing logic addresses the first and third categories most effectively. As a result, it can recover a significant percentage of failed transactions.

How Smart Routing Logic Works

Smart routing systems operate in real time. The decision happens in milliseconds — before the customer even sees a response. Here is the basic flow:

Step 1: Transaction data collection.

The system collects key data points — card BIN (Bank Identification Number), transaction amount, currency, country, device type, and merchant category.

Step 2: Rule-based evaluation.

Pre-configured rules filter the available processors. For example, certain processors handle international cards better. Others excel with high-value transactions. Therefore, the system narrows options based on these rules.

Step 3: Machine learning scoring.

Advanced systems apply ML models trained on historical approval data. They score each processor for this specific transaction type. Furthermore, they update these scores continuously as new data arrives.

Step 4: Processor selection.

The system routes to the highest-scoring processor. If that processor fails, automatic failover triggers instantly and retries through the next best option.

Step 5: Feedback loop.

The outcome — approval or decline — feeds back into the model. Consequently, the system learns and improves with every transaction.

Key Factors in Routing Decisions

No two transactions are identical. Smart routing systems evaluate dozens of variables simultaneously. Here are the most impactful ones.

Processor performance by card type: Visa approvals may be higher on one processor while Mastercard performs better on another. Routing logic matches card type to the best-performing processor.

Geographic routing: International transactions often fail because processors lack relationships with certain issuing banks. Therefore, routing to a processor with strong regional coverage improves approval rates significantly.

Transaction amount thresholds: High-value transactions carry higher fraud risk. Some processors have lower approval rates for large amounts. Routing logic directs these to processors with better high-value performance.

Processor uptime data: If a processor has experienced downtime in the last hour, the system deprioritizes it. This prevents routing to a degraded system.

Time of day patterns: Approval rates vary by time of day and day of week. Smart systems factor in temporal patterns to optimize routing timing.

Cascading Failover: Recovering Failed Transactions

Cascading failover is one of the most powerful features of smart routing. It automatically retries declined transactions through alternative processors. Here is how it works in practice. A transaction is sent to Processor A. Processor A declines it due to a technical issue. Instead of showing the customer an error, the system silently retries through Processor B. If Processor B succeeds, the customer never knows anything went wrong.

This recovery mechanism can save between 3% and 15% of transactions that would otherwise be lost. For high-volume businesses, that represents significant recovered revenue. However, cascading must be configured carefully. Not all declines should trigger a cascade. Hard declines — fraud flags, closed accounts — should not be retried. Retrying these can increase fraud risk or invite additional decline fees. Therefore, routing logic must distinguish between recoverable and non-recoverable failures before triggering a cascade.

Cost Optimization Through Routing

Smart routing does more than improve approval rates. It also optimizes processing costs. Different processors charge different interchange fees. Additionally, fees vary by card type, transaction type, and volume tier. A smart routing system can factor in cost alongside approval probability.

For example, two processors may have similar approval rates for a given transaction. However, one charges 0.1% less in interchange. Routing to the cheaper processor — without sacrificing approval likelihood — reduces processing costs over millions of transactions.

Currency routing is another cost lever. Processing payments in the cardholder’s local currency often reduces decline rates and avoids dynamic currency conversion fees. Consequently, routing systems can detect cardholder currency preferences and route accordingly.

Furthermore, some processors offer volume discounts. Routing logic can be configured to consolidate volume on preferred processors to hit discount thresholds faster.

How to Implement Smart Routing

Implementation depends on your current payment infrastructure. Here are the main approaches.

Option 1: Payment orchestration platforms.

Platforms like Spreedly, Primer, and Gr4vy sit on top of your existing processors. They provide routing logic, failover, and analytics without requiring you to rebuild your payment stack. This is the fastest path for most businesses.

Option 2: Build in-house routing logic.

Larger businesses with engineering resources sometimes build custom routing layers. This offers maximum control but requires significant investment. Furthermore, it demands ongoing maintenance as processor APIs and performance data change.

Option 3: Use a payment processor with built-in smart routing.

Some processors — like Stripe with its Smart Retries feature or Adyen with its revenue optimization tools — offer routing logic as part of their service. This is the simplest option. However, it limits routing to processors within that ecosystem.

Regardless of approach, start with clear goals. Define the metrics you want to improve — approval rate, cost per transaction, or chargebacks. Then, configure routing rules that address those specific goals.

Measuring the Impact of Smart Routing

Implementing routing logic without measurement is guesswork. These metrics tell you whether it is working.

Authorization rate: The percentage of attempted transactions that are approved. This is the primary metric. A well-tuned routing system should lift this by 2% to 10% depending on your baseline.

Decline recovery rate: Of all declined transactions, how many does your failover system recover? This measures the effectiveness of your cascading logic specifically.

Cost per transaction: Are you routing efficiently from a cost perspective? Track this alongside approval rate to ensure you are not sacrificing margins for volume.

Processor reliability score: How often does each processor fail or underperform? Use this to continuously refine your routing hierarchy.

Chargeback rate by processor: Some processors have better fraud detection tools. Routing high-risk transactions to those processors can reduce chargebacks. Track this metric to validate that hypothesis.

Review these metrics monthly. Furthermore, A/B test routing configurations to identify improvements. Treat routing logic as a product — iterate and optimize continuously.

The Future of Payment Routing

Payment routing is evolving rapidly. Several trends are shaping its future. AI-driven routing: Machine learning models are becoming more sophisticated. They now factor in hundreds of variables simultaneously and update in near real time. As a result, routing decisions are becoming more accurate than any rule-based system could achieve.

Open banking integration: With open banking APIs, routing logic can access real-time account data. This allows systems to route to the most appropriate payment rail — card, bank transfer, or digital wallet — based on what will most likely succeed.

Real-time payments: As instant payment networks like RTP and FedNow expand, routing systems will need to handle new rails alongside traditional card networks. Consequently, routing logic must become more sophisticated to manage this complexity.

Biometric authentication: Payments combined with biometric verification reduce fraud flags and improve approval rates. Routing systems will increasingly factor in authentication method when making routing decisions.

The businesses that invest in smart routing infrastructure today will be better positioned for these shifts. Furthermore, the cost of not optimizing — lost revenue, higher processing costs, worse customer experience — only grows with transaction volume.

Conclusion

Payment routing logic is not a luxury for large enterprises. It is a necessity for any business that processes payments at scale.

Every declined transaction is recoverable revenue. Every inefficient routing decision is a cost you are paying unnecessarily. Smart routing — with cascading failover, cost optimization, and machine learning — addresses all of these issues simultaneously. It improves approval rates, reduces costs, and delivers a better checkout experience.

Start with the metrics that matter most to your business. Then, choose a routing approach that fits your technical resources. Above all, treat routing as an ongoing investment — not a one-time setup.

The difference between a 92% and a 97% approval rate is enormous at scale. Smart payment routing logic is how you close that gap.

Read More:

AWS-SDK for Payments: What Businesses Must Know Full Guide