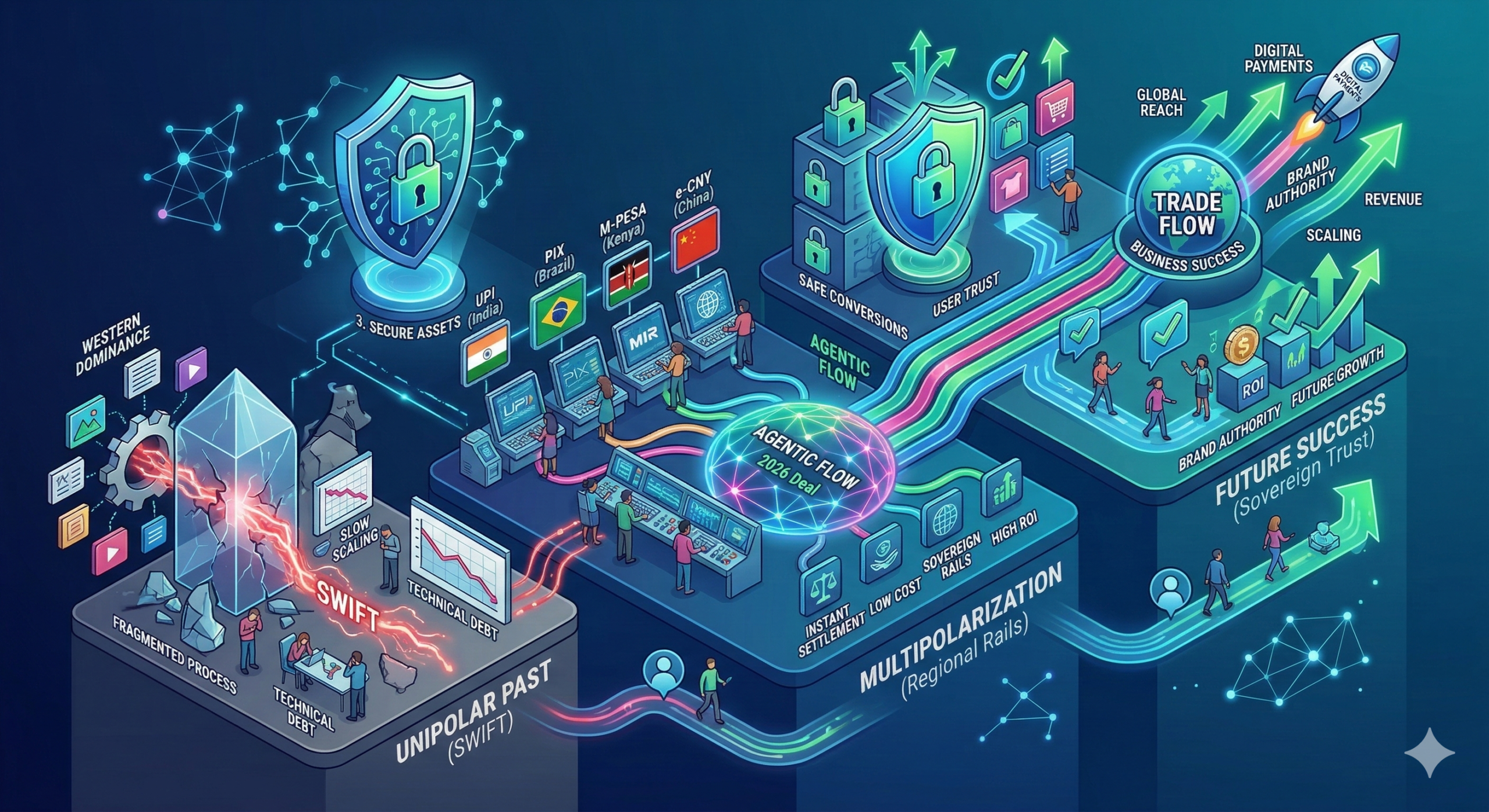

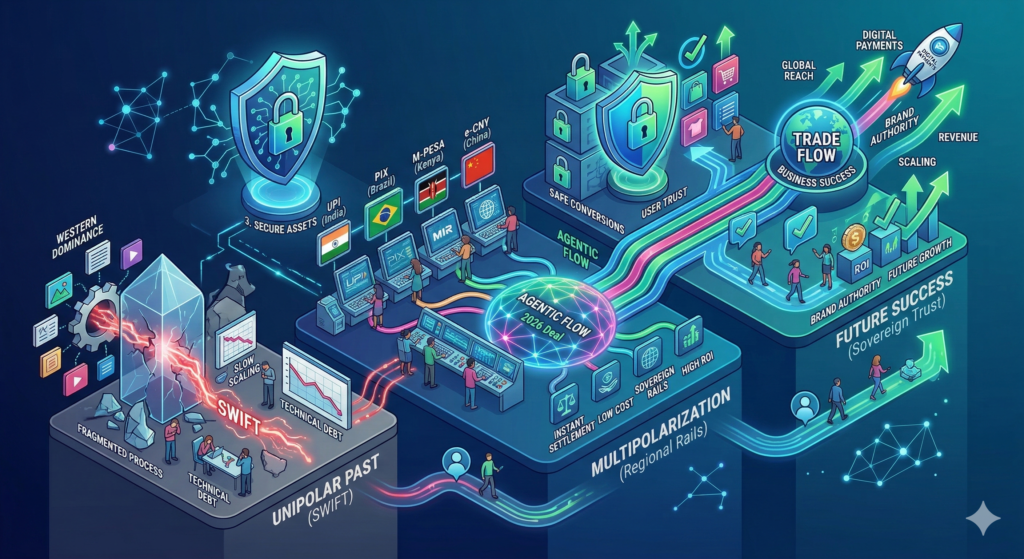

In 2026, the world of digital payments is no longer a unipolar system centered on the US dollar. For decades, the global financial plumbing relied almost exclusively on Western-led rails like SWIFT. However, we are now witnessing a “multipolarization” of money movement. Emerging economies are building their own sovereign digital bridges, allowing them to bypass traditional bottlenecks and sanctions. This shift is not just about technology; it is a fundamental rebalancing of global economic power.

The Rise of Sovereign Digital Rails

The first pillar of this shift is the explosive growth of domestic real-time payment systems. India’s upi has become the global gold standard, recently smashing records with over 21 billion transactions in a single month. Specifically, countries are no longer waiting for international permission to modernize. They are exporting their own stacks—like India’s UPI or Brazil’s Pix—to neighboring nations. Furthermore, these regional networks are now linking directly to one another. Consequently, a merchant in Singapore can accept a payment from an Indian tourist without the money ever touching a US-based clearinghouse.

CBDCs: The New Financial Architecture

Central Bank Digital Currencies (CBDCs) are the “secret weapon” in the quest for financial sovereignty. In 2026, the BRICS bloc is moving toward a unified CBDC framework. Specifically, this allows nations to settle massive trade deals in their own local digital currencies. Projects like mBridge—which connects China, the UAE, Thailand, and Saudi Arabia—demonstrate that cross-border payments can be instant and cheap. By using blockchain-based settlement, these nations reduce their reliance on the US dollar as an intermediary. Therefore, the “dollar trap” is slowly being dismantled by code and cryptography.

The Fragmentation of Global Trust

The multipolarization of digital payments is also a response to the “weaponization” of finance. When major economies are cut off from Western systems, they don’t stop trading; they build better alternatives. Specifically, we are seeing the emergence of parallel systems that prioritize autonomy over universal interoperability. This creates a “mosaic” of regional standards. While this adds complexity for global corporations, it provides a safety net for emerging markets. Your strategy must now account for this divided landscape where local trust anchors are becoming as important as global ones.

Impact on Global Trade and MSMEs

For small and medium enterprises (MSMEs), this shift is a massive win. Traditional cross-border trade was once too expensive for tiny firms due to high bank fees. Now, sovereign digital payments corridors are lowering these costs by up to 70%. Specifically, instant settlement allows a small artisan in Nairobi to sell directly to a buyer in Mumbai with near-zero friction. Furthermore, these systems are “sanction-resistant” by design, ensuring that trade can continue even during geopolitical storms. This levels the playing field for the Global South in a way never seen before.

2026: A Defining Year for Monetary Sovereignty

As India hosts the 2026 BRICS summit, the focus is squarely on “sovereign rails.” The goal is a world where no single nation can “turn off” another’s economy. Specifically, the integration of national systems into open-source protocols ensures that each country maintains its own digital node. You will find that this move toward decentralization makes the global financial system more resilient. It is a transition from a world of “financial hegemony” to a world of “financial choice.” Indeed, the right technical lead today prepares your business for a world where the dollar is just one of many options.

FAQs

1 Is the US dollar losing its value?

Specifically, no. The dollar remains a strong store of value, but it is losing its absolute monopoly as the only way to pay for international goods.

2 What is the benefit of a multipolar system?

Indeed, it leads to lower transaction fees, faster settlements, and less risk for countries that want to avoid external political pressure.

3 Will I need different apps to pay in different countries?

The goal of systems like upi is interoperability, meaning your home app should eventually work across many different national networks.

4 Are these new systems as secure as traditional banks?

Yes, most use advanced tokenization and blockchain tech, which often makes them more secure against modern AI-powered fraud.

5 How can my business prepare for this?

First, ensure your payment gateway supports international “account-to-account” (A2A) transfers and sovereign digital wallets.

Read More:

Why a global UPI network is the new South-South trade rail?

How CBDCs protect national trade in a world of sanctions?

How A Strong Payment Infrastructure Builds Global Soft Power