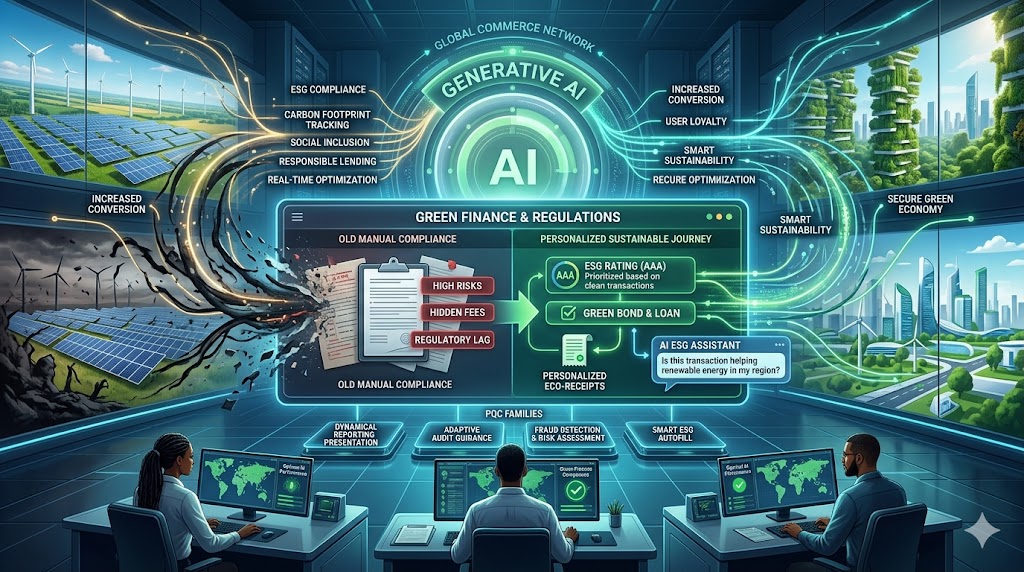

The world of money is changing to help save our planet. Today, many people care about the environment and social fairness. This is often called ESG. Because these values are so important, they are now part of global finance. Therefore, banks and payment firms must follow new green rules to stay in business. If they ignore these trends, they might face heavy fines and lose their good name. In short, the future of finance is green.

Why ESG Matters for Every Transaction

Traditional banking used to focus only on profits and speed. However, regulators now look at how money flows affect the earth. Consequently, every major player in finance must track their carbon footprint. This is because digital payments use a lot of energy in data centers. Furthermore, users want to know if their bank supports clean energy. Therefore, finance is no longer just about numbers; it is about values.

Another big issue is social fairness in the payment world. For instance, many people in poor areas still lack basic tools to pay. If a system is not inclusive, it fails the “S” in ESG. Thus, modern finance must ensure that everyone has a fair chance to use digital money. A smart strategy solves this by offering low-cost tools for every citizen. This keeps the economy healthy and builds a better society for all.

How New Regulations Change the Game

Strict green rules are a vital part of modern trade. In many regions, firms must report how much energy their systems consume. Because this transparency is required by law, it builds more trust with the public. Furthermore, a green approach in finance can lead to lower taxes for eco-friendly firms. This means that being good to the planet can actually save a company money. In short, finance wins when it aligns with the health of the world.

Green bonds and sustainable loans are also growing fast. Instead of generic funding, banks offer special deals for green projects. Because these loans are tied to ESG goals, they encourage better behavior. Therefore, finance experts are building new frameworks to track these results accurately. This ensures that the money actually helps build wind farms or solar plants. Finally, these regulations ensure that “green” is a real action and not just a marketing trick.

Staying Safe and Compliant

Security and ethics are the most important parts of green trade. Hackers are always looking for ways to exploit new systems. Luckily, new AI tools are great at spotting fraud while staying energy-efficient. If a transaction looks odd, the system stops it fast. This keeps your money and your data very safe. Because the AI is so smart, it rarely blocks real customers. Thus, finance stays strong and secure for every global user.

Additionally, digital receipts help reduce waste without making the process slow. It uses cloud tech to prove the sale is real in a second. When you use these tools, the checkout flow feels very smooth and eco-friendly. You just click and go. Therefore, the risk of a mistake or paper waste is very low. This is the future of finance in a sustainable world. Finally, safety ensures that users feel comfortable trusting their money with green firms.

The Big Future of Sustainable Money

We are only at the start of a massive green shift. Soon, every payment app will show you the carbon cost of your coffee or clothes. This means we will see a huge need for clear and honest data. Instead of a hard process, we get a tailored world of green choices. Sustainable finance makes every transaction feel like a positive step for the earth. It is the best way to shop in 2026. If you want to stay ahead, you must use these green tools now. In conclusion, ESG is the new engine for global growth.

Frequently Asked Questions

1. Does green finance make payments more expensive?

No, it often leads to better efficiency which can lower costs for the user over time.

2. How does a payment app help the planet?

By using green data centers and offering digital receipts to save millions of trees.

3. What does ESG stand for in banking?

It stands for Environmental, Social, and Governance rules that guide fair and green trade.

4. Can I choose a green bank for my store?

Yes, many banks now have special ESG ratings to show they are eco-friendly.

5. Will all finance become green soon?

Yes, most global regulators are making green rules a requirement for all firms by 2027.

Read More:

How a payment gateway Makes Virtual Shopping Seamless?