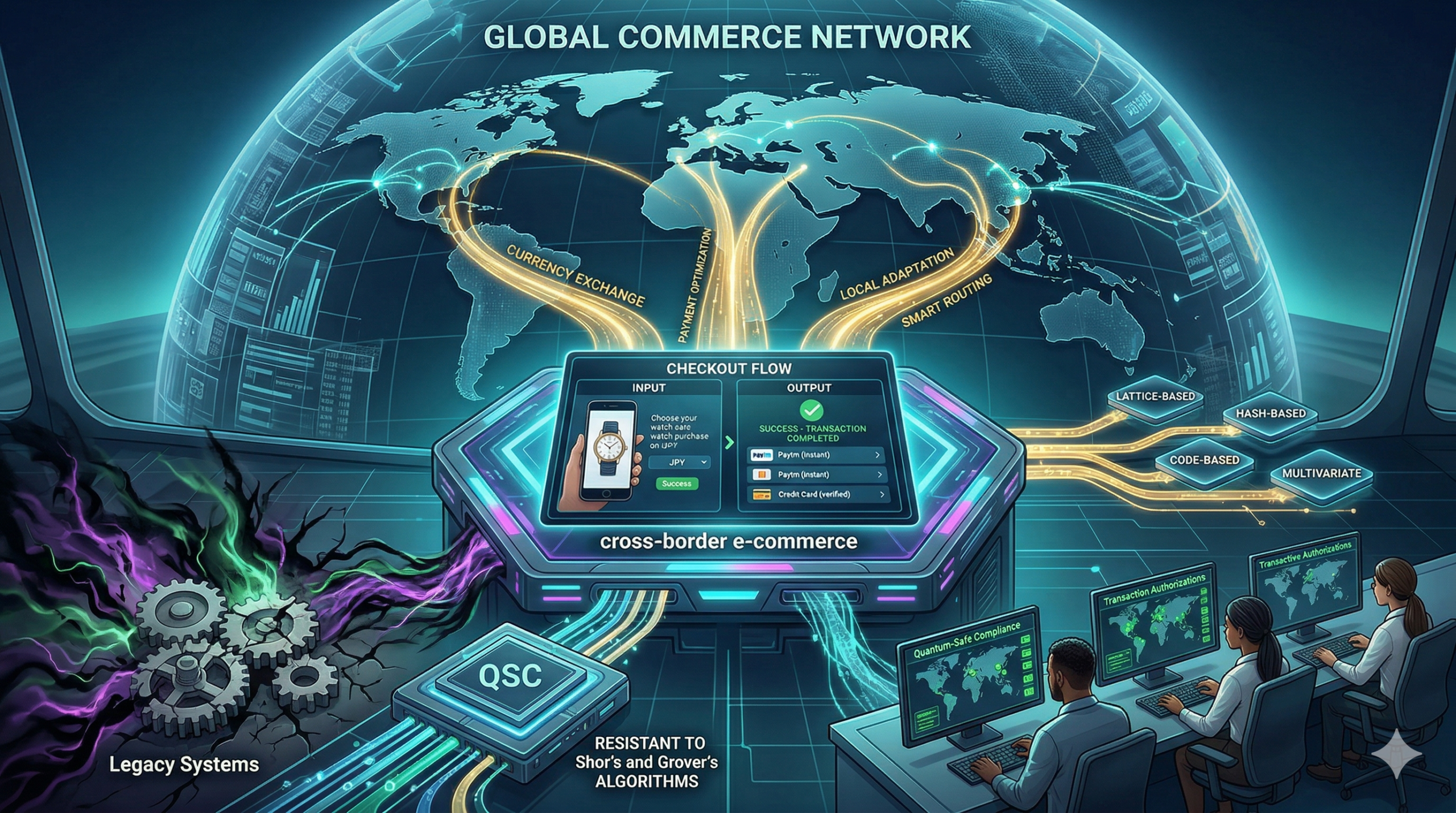

Global trade is moving faster than ever before. Most online stores now look for customers in every corner of the world. However, selling across borders brings many difficult hurdles. This is because every country has its own rules and preferred ways to pay. Therefore, businesses must find smart ways to handle these gaps. If they fail, they risk losing sales and trust. Successful e-commerce depends on a smooth and safe payment journey for everyone.

The Big Problems for Global Sellers

High fees are a major enemy of global growth. When a customer buys something from another country, banks often take a large cut. Consequently, the final price becomes too high for the shopper. This is because currency exchange rates are often unfair. Furthermore, hidden costs can surprise the customer at the final step. This leads to cart abandonment. Therefore, e-commerce firms must be very clear about all costs from the start.

Another big issue is the variety of payment habits. For instance, shoppers in Europe might prefer digital wallets. Meanwhile, customers in Asia might use QR codes or local bank transfers. If a store only offers credit cards, it will fail in these regions. Thus, a one-size-fits-all plan does not work. Every e-commerce site needs to adapt to local tastes to stay ahead.

Solutions for a Better Payment Journey

Multi-currency pricing is a vital tool for success. Customers want to see prices in their own money. Because this removes confusion, it builds instant trust. Furthermore, using a local acquiring bank can reduce transaction fees. This means the store keeps more profit while the user pays less. In short, e-commerce wins when the math is simple for the buyer.

Smart routing is another great way to fix failures. Sometimes, a bank might block a foreign payment by mistake. However, modern systems can instantly try a different bank to finish the sale. This keeps the flow moving without any delay. Because the user does not see the struggle, the experience feels like magic. Therefore, e-commerce platforms must use these intelligent tools to prevent lost sales.

Staying Safe Against Global Fraud

Security is the most important part of any global sale. Hackers are always looking for ways to steal data across borders. Luckily, new AI tools are great at spotting fraud by looking at millions of data points. If a transaction looks odd, the system stops it fast. This keeps your money and data very safe. Because the AI is so smart, it rarely blocks real customers. Thus, e-commerce stays strong and secure for everyone.

Additionally, 3D Secure 2.0 helps verify identity without making the process slow. It uses data to prove the user is real in the background. When you use these tools, the checkout flow feels very smooth. You just click and go. Therefore, the risk of a mistake or theft is very low. This is the future of e-commerce in a connected world. Finally, safety ensures that your brand grows a good name worldwide.

The Future of Global Trade

We are only at the start of a massive shift. Soon, every store will use local solutions to talk to global fans. This means we will see faster shipping and lower fees for everyone. Instead of a hard process, we get a tailored world of products. E-commerce makes every global transaction feel like a local one. It is the best way to trade in 2026. If you want to stay ahead, you must use these solutions now. In conclusion, a better payment journey is the key to global success.

Frequently Asked Questions

1. Why do global payments often fail?

They fail because banks might flag foreign cards as high-risk or due to technical errors in legacy systems.

2. How can I reduce currency exchange fees?

You should use a local payment provider or an e-wallet that offers better rates than traditional banks.

3. What is the best payment method for Asia?

Local digital wallets and QR-based systems are the most popular choices for shoppers in that region.

4. Does 3D Secure slow down my checkout?

No, the 2.0 version is much faster and often works in the background without bothering the user.

5. Is it hard to set up multi-currency pricing?

Most modern payment gateways offer this feature as a simple setting you can turn on.

Read More: