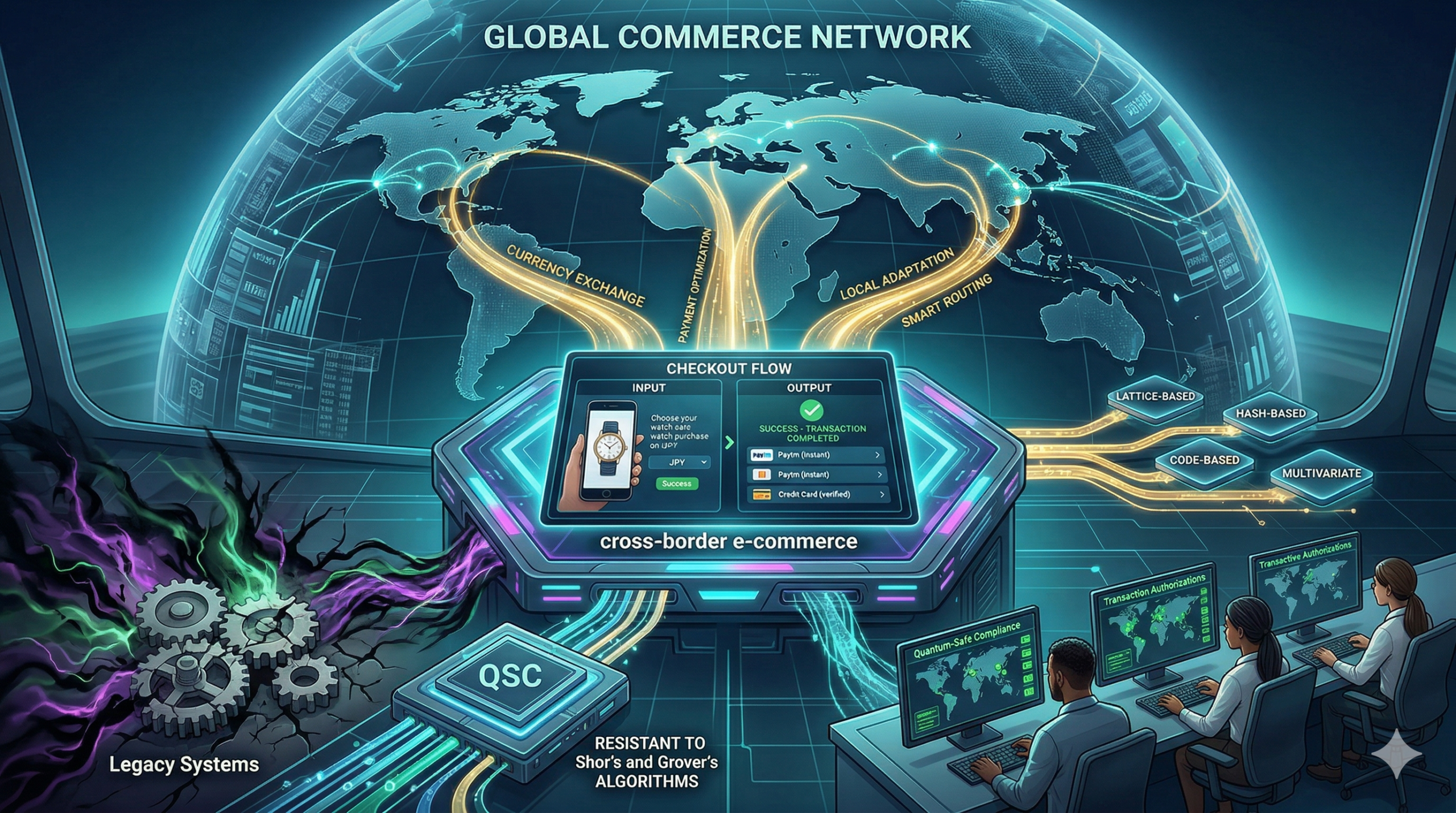

Global trade is moving faster than ever before. Most online stores now look for customers in every corner of the world. However, selling across borders brings many difficult hurdles. This is because every country has its own rules and preferred ways to pay. Therefore, businesses must find smart ways to handle these gaps. If they fail, they risk losing sales and trust. Successful e-commerce depends on a smooth and safe payment journey for everyone.

The Big Problems for Global Sellers

High fees are a major enemy of global growth. When a customer buys something from another country, banks often take a large cut. Consequently, the final price becomes too high for the shopper. This is because currency exchange rates are often unfair. Furthermore, hidden costs can surprise the customer at the final step. This leads to cart abandonment. Therefore, e-commerce firms must be very clear about all costs from the start.

Another big issue is the variety of payment habits. For instance, shoppers in Europe might prefer digital wallets. Meanwhile, customers in Asia might use QR codes or local bank transfers. If a store only offers credit cards, it will fail in these regions. Thus, a one-size-fits-all plan does not work. Every e-commerce site needs to adapt to local tastes to stay ahead.

Solutions for a Better Payment Journey

Multi-currency pricing is a vital tool for success. Customers want to see prices in their own money. Because this removes confusion, it builds instant trust. Furthermore, using a local acquiring bank can reduce transaction fees. This means the store keeps more profit while the user pays less. In short, e-commerce wins when the math is simple for the buyer.

Smart routing is another great way to fix failures. Sometimes, a bank might block a foreign payment by mistake. However, modern systems can instantly try a different bank to finish the sale. This keeps the flow moving without any delay. Because the user does not see the struggle, the experience feels like magic. Therefore, e-commerce platforms must use these intelligent tools to prevent lost sales.

Staying Safe Against Global Fraud

Security is the most important part of any global sale. Hackers are always looking for ways to steal data across borders. Luckily, new AI tools are great at spotting fraud by looking at millions of data points. If a transaction looks odd, the system stops it fast. This keeps your money and data very safe. Because the AI is so smart, it rarely blocks real customers. Thus, e-commerce stays strong and secure for everyone.

Additionally, 3D Secure 2.0 helps verify identity without making the process slow. It uses data to prove the user is real in the background. When you use these tools, the checkout flow feels very smooth. You just click and go. Therefore, the risk of a mistake or theft is very low. This is the future of e-commerce in a connected world. Finally, safety ensures that your brand grows a good name worldwide.

The Future of Global Trade

We are only at the start of a massive shift. Soon, every store will use local solutions to talk to global fans. This means we will see faster shipping and lower fees for everyone. Instead of a hard process, we get a tailored world of products. E-commerce makes every global transaction feel like a local one. It is the best way to trade in 2026. If you want to stay ahead, you must use these solutions now. In conclusion, a better payment journey is the key to global success.

Frequently Asked Questions

1. Why do global payments often fail?

They fail because banks might flag foreign cards as high-risk or due to technical errors in legacy systems.

2. How can I reduce currency exchange fees?

You should use a local payment provider or an e-wallet that offers better rates than traditional banks.

3. What is the best payment method for Asia?

Local digital wallets and QR-based systems are the most popular choices for shoppers in that region.

4. Does 3D Secure slow down my checkout?

No, the 2.0 version is much faster and often works in the background without bothering the user.

5. Is it hard to set up multi-currency pricing?

Most modern payment gateways offer this feature as a simple setting you can turn on.

The world of money is changing very fast. Many nations want to build their own systems, free from old ways. However, the path to a new global order is complex and full of big choices. Because of this, staying ahead means looking toward fresh tech and strong partnerships. Specifically, BRICS and digital payments are now a key topic for leaders worldwide. This offers a clear map for new trade, faster work, and a very modern way to pay. This move is not just about tools for a few banks. In fact, it is a smart strategy for many lands to gain more power. Consequently, understanding this impact helps you see why it matters.

The Current Landscape: Visa and Mastercard’s Dominance

For a long time, two names have ruled how the world pays. Visa and Mastercard have built vast networks across the globe. They process billions of deals every single day with ease. These systems are reliable and trusted by many people everywhere. However, this power also means control rests in just a few hands. Some nations worry about this strong hold on their money flows. They feel that vital services should not be tied to just one or two firms. Furthermore, geopolitical events can sometimes affect these global payment channels. This makes some countries very eager to find new ways to pay. Therefore, the search for an independent path grows stronger.

The BRICS Alliance: A Push for Economic Independence

BRICS is a group of five big nations: Brazil, Russia, India, China, and South Africa. These countries represent a huge part of the world’s people and wealth. They often work together to boost their trade and influence. A key goal for BRICS is to create more economic freedom for its members. They want to reduce their reliance on systems built and run by other blocs. This desire extends to how money moves between them. The idea of a shared payment system is very appealing. It would help them trade more easily without outside interference. Consequently, BRICS and digital payments are a natural fit for their goals. This alliance seeks to build a new financial backbone.

The Rise of Digital Payments and Central Bank Digital Currencies (CBDCs)

Digital payments are quickly changing how we use money. Apps on phones, online wallets, and instant transfers are common now. This shift makes it easier to imagine new global systems. A big part of this trend is the rise of Central Bank Digital Currencies (CBDCs). Many BRICS nations, like China and India, are actively working on their own CBDCs. These are digital forms of a country’s money, issued by its central bank. If BRICS countries can link their CBDCs, it would create a powerful new network. This would allow fast, cheap, and direct payments between their economies. Such a system could bypass older networks entirely. Thus, BRICS and digital payments could form a new standard.

Challenges to Building a Unified BRICS Payment System

Creating a brand new global payment system is not easy. First, there are many technical hurdles to overcome. Each country has its own rules, tech, and banking laws. Making these all work together perfectly takes huge effort. Furthermore, building trust among member states is vital. They must agree on how data is shared and how disputes are handled. There are also security concerns; any new system must be very safe from cyber-attacks. Finally, getting people and businesses to adopt a new method takes time. They are used to the ease of Visa and Mastercard. Despite these challenges, the motivation for a BRICS digital payment alternative is very high.

Potential Impact: A New Global Financial Order?

If BRICS succeeds in creating its own payment system, the impact could be huge. It would give these nations more control over their own money flows. They could reduce fees and speed up cross-border trade. It might also encourage other developing countries to join or adopt the system. This could lead to a more diverse and multi-polar global financial world. Visa and Mastercard would still be very important. However, they would face a serious new competitor. This competition could even push existing systems to innovate more. Consequently, BRICS and digital payments could reshape how we think about international finance. The shift could truly impact global power dynamics.

Conclusion: The Road Ahead

The idea of an alternative to Visa and Mastercard from the BRICS bloc is gaining traction. The rise of digital payments and CBDCs makes this vision more possible than ever. While big challenges remain, the desire for economic independence is a strong driving force. This development is worth watching closely. It could signal a major shift in how global money moves and who controls it. The future of international payments might be far more diverse than it is today.

FAQs

1 What is BRICS?

It’s a group of major emerging economies: Brazil, Russia, India, China, South Africa.

2 Why do BRICS nations want a new payment system?

They want more economic independence and less reliance on existing global payment networks.

3 What are CBDCs?

Central Bank Digital Currencies are digital forms of a country’s national money, issued by its central bank.

4 Could a BRICS system replace Visa/Mastercard?

It might not replace them entirely but could emerge as a significant alternative, especially for cross-border transactions among BRICS and allied nations.

5 What are the biggest challenges?

Technical integration, regulatory harmonization, security, and user adoption across diverse nations.

In the rapidly evolving world of global finance, traditional banking routes are facing significant challenges. For instance, the trade relationship between Russia and China has undergone a massive transformation recently. As a result, both nations are exploring digital assets to maintain their economic ties today. Specifically, stablecoins have emerged as a powerful tool for a sanctions workaround. This shift is not just a trend but a strategic move to ensure trade continuity. Understanding how this system works is essential for anyone following global economic shifts. Russia–China trade in digital assets: stablecoins as a sanctions workaround is a vital topic now.

The Rise of Digital Assets in Cross-Border Trade

Sanctions have largely cut off traditional financial channels between these two major economies lately. Consequently, businesses have turned to alternative methods to settle payments quickly. Digital assets, particularly stablecoins, provide a seamless way to move value across borders. Because these assets are not tied to the Western banking system, they offer independence. Furthermore, the speed of transactions is much faster than conventional wire transfers. This efficiency is vital for maintaining the flow of goods and services. As a result, digital assets are now a cornerstone of modern trade. Russia–China trade in digital assets: stablecoins as a sanctions workaround keeps the economy moving.

Why Stablecoins Are the Preferred Workaround

Stablecoins are unique because they are pegged to a stable asset like gold. Therefore, they do not suffer from the extreme volatility of other coins. This stability makes them ideal for large commercial transactions. For example, a Russian exporter can receive payment in a dollar-pegged stablecoin. Similarly, Chinese importers can settle debts quickly using these digital tokens. In fact, stablecoins act as a bridge that bypasses the SWIFT system. This allows trade to continue even under the strictest financial restrictions. Russia–China trade in digital assets: stablecoins as a sanctions workaround provides needed financial safety.

The Role of Central Bank Digital Currencies (CBDCs)

In addition to private stablecoins, both nations are developing their own digital currencies. Russia is testing the digital ruble while China is expanding the digital yuan. These state-controlled assets aim to provide a regulated alternative for settlements. By using CBDCs, both countries can ensure that their financial data remains private. Moreover, these digital currencies can be directly exchanged between central banks. This eliminates the need for intermediary banks located in third countries. Consequently, the reliance on the US dollar is further reduced. Russia–China trade in digital assets: stablecoins as a sanctions workaround is a long-term goal.

Navigating the Legal and Regulatory Landscape

The use of digital assets for trade is still a relatively new frontier. Thus, both countries are working to create clear legal frameworks for these activities. Russia has recently passed laws to allow the use of crypto for payments. In contrast, China maintains strict domestic bans but shows pragmatism in international trade. Therefore, businesses must navigate a complex web of regulations to stay compliant. However, the drive to maintain trade volume often outweighs the regulatory hurdles. As these laws mature, we can expect more structured trade corridors. Russia–China trade in digital assets: stablecoins as a sanctions workaround requires careful legal study.

Future Implications for Global Finance

The shift toward digital assets marks a significant turning point in global finance. Specifically, it demonstrates that nations can build parallel financial systems when needed. This decentralization reduces the power of traditional financial hubs. Consequently, other countries facing similar pressures may look to this model as a blueprint. The success of stablecoins as a sanctions workaround proves the resilience of blockchain. Furthermore, it highlights the growing importance of digital sovereignty. As more trade moves on-chain, the global landscape will become increasingly fragmented. Russia–China trade in digital assets: stablecoins as a sanctions workaround is just the beginning.

Economic Resilience Through Digital Innovation

Nations must adapt when they face exclusion from the global banking grid. For instance, Russia and China are proving that technology can bridge the gap. Digital assets offer a way to keep supply chains active and stable. Moreover, this innovation helps small businesses engage in international trade without fear. Because the blockchain is transparent, it also helps in tracking large shipments. Therefore, the adoption of these tools is a sign of economic resilience. It is a bold move toward a multipolar financial world. Russia–China trade in digital assets: stablecoins as a sanctions workaround shows how tech solves problems.

Reducing Dependency on Western Financial Tools

For a long time, the global economy relied heavily on Western systems. However, this dependency is now viewed as a risk by some nations. Using stablecoins allows for a shift away from traditional currency traps. This means that trade can occur without the need for dollar conversion. Similarly, it protects local currencies from external shocks and sudden policy changes. This movement is gaining momentum across the Asian continent. Therefore, we may see more countries joining this digital trade alliance. Russia–China trade in digital assets: stablecoins as a sanctions workaround is a major part of this shift.

Security and Privacy in Digital Trade

Security is a top priority for any business conducting cross-border deals. Fortunately, blockchain technology provides a high level of encryption for every transaction. This ensures that the payment data is safe from hackers and prying eyes. Furthermore, the decentralized nature of these assets means there is no single point of failure. This makes the entire trade network more robust and reliable. Consequently, more companies are feeling confident about using digital tokens. It is a safer way to conduct business in a volatile world. Russia–China trade in digital assets: stablecoins as a sanctions workaround ensures secure transfers.

The Strategic Importance of Stablecoin Liquidity

Liquidity is essential for any currency used in international trade today. Because stablecoins are widely available, they provide the necessary liquidity for big deals. This means that businesses can convert their tokens back into local cash easily. Moreover, the presence of various stablecoins gives traders more choices and flexibility. This competition keeps transaction costs low for everyone involved. Therefore, the growth of the stablecoin market is a win for global trade. It provides the fuel needed for the digital economy to run. Russia–China trade in digital assets: stablecoins as a sanctions workaround relies on this liquidity.

FAQs

1 Why are stablecoins used for trade instead of Bitcoin?

Stablecoins offer price stability which is essential for business contracts. Consequently, they do not have the high risk of price changes.

2 Are these digital transactions legal in both countries?

Russia has legalized digital assets for international trade specifically to bypass sanctions. Similarly, China allows their use for cross-border settlements despite domestic bans.

3 How do stablecoins bypass traditional sanctions?

They operate on independent blockchain networks rather than the SWIFT system. Therefore, they do not need approval from Western banks to function.

4 What is the role of the digital yuan in this trade?

The digital yuan allows for direct state-to-state payments without using dollars. Thus, it strengthens the financial bond between the two nations.

5 Can small businesses use this method for trade?

Yes, digital assets are accessible to businesses of all sizes. Moreover, they offer a faster and cheaper way to move money globally.

I’ve heard it a thousand times. A nation relies only on one foreign credit card firm. And yet, their local shops pay high fees. Usually, that is just a polite way of saying the country has lost its own power. Also, old bank moves take a long time. They involve too many middle men. If you build a new market on old tracks, you are building a ghost town.

In fact, a system where local tracks handle 80% of deals is worth much more. Furthermore, the biggest cost in 2026 is the lack of links between close nations. This happens when people must carry cash or pay high fees. This path creates a big gap. Because of this, users want a fast and easy way to pay.

The solution lies in a smart way to keep your money power. This turns a national rule into a solid sales tool. This isn’t just a tech shift. Instead, it is a big plan. This helps every person pay in a safe way. Once you use these rules, you will see your local market grow.

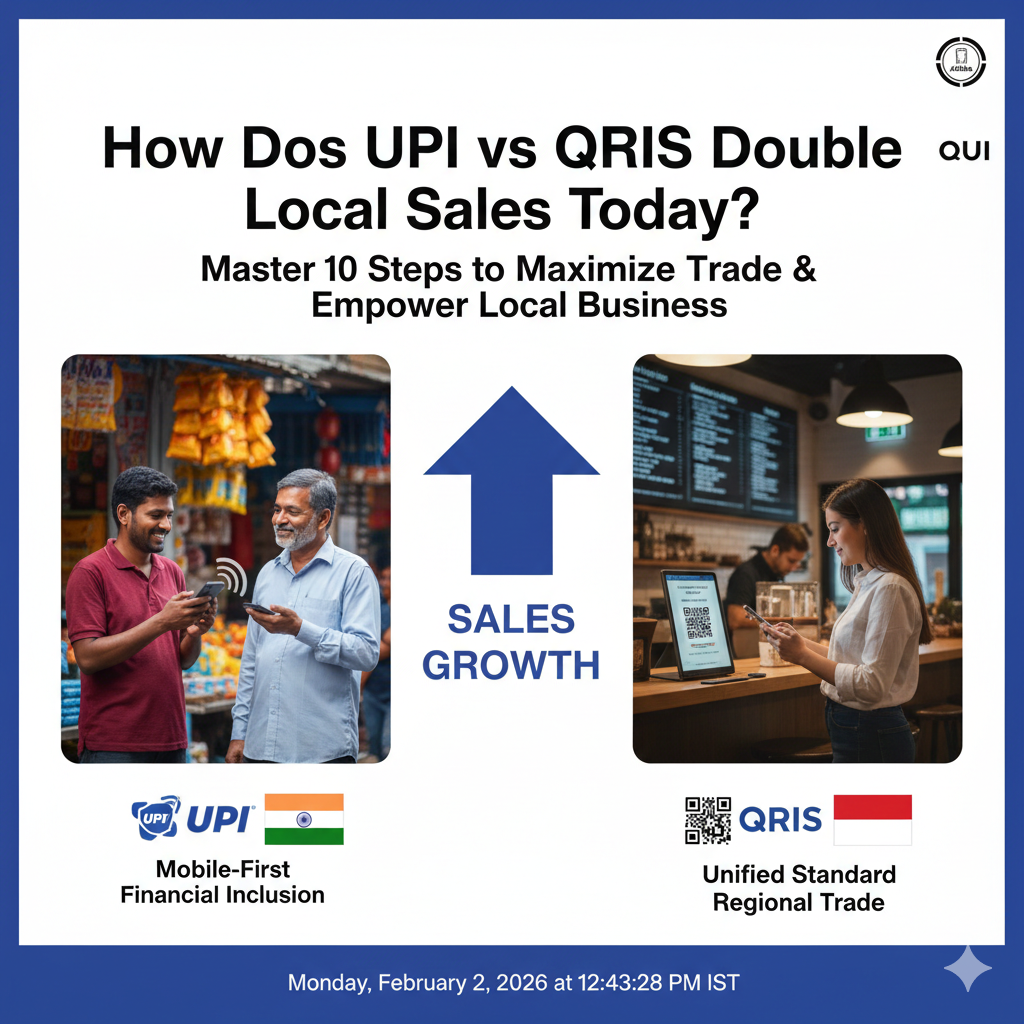

1. UPI: The Best Way to Join the Bank

If you aren’t looking at the UPI growth data, you are flying blind. Specifically, India’s UPI has won more of the market for three months in a row. You need to know why this tool works so well. For example, was it the low cost or the ease of use? Smart leaders use the UPI path to see how to reach far away areas. Then, they make mobile plans for their own folks.

Moreover, smart plans allow for a steady gain in the market. This is because they focus on a good user path. By using a top-tier plan, you help your local banks win. This leads to steady gains. It sounds simple. However, most lands are too busy guessing to look at the UPI success.

2. QRIS: Linking Asian Shops Through Scans

The move to regional QR tools is happening faster than we thought. While old tools are slow, QRIS adds cross-border links through one rule. These rules use logic to link many bank nets. These rules act like a smart helper for regional trade.

However, one-country tools are not enough for a big change. The most top-tier stage is a system for many lands. These nets handle tasks like live money swaps. These tools help many banks work as one. Consequently, they act as a smart brain for the whole Asian area.

3. Digital Euro: Keeping Europe’s Money Power

To build smart bank tools, you should not have to glue poor parts together. The Digital Euro aims to use one public coin. Specifically, this uses Europe’s strength to give safe answers to market moves. This means a person can travel with their full data ready to go.

Additionally, think of a case where your phone wallet knows your local spot. It uses safe data to help you buy things fast. This base ensures that your responses to global stress stay strong. Therefore, it stops the friction that slows down your best shops. It helps them finish big deals with fewer errors.

4. The 80/20 Rule for National Payments

If your land spends all its time on foreign nets, you have no time for local growth. You must follow an 80/20 rule. Thus, use local tracks to handle 80% of daily buys. This includes food or bus rides. This leaves the 20% of big global moves to top-tier firms.

Using fast moves helps shops stay on track without cash. AI can even set up fast replies based on simple talk. This allows your shops to work in a flow. They do not have to switch between many tools. This leads to much faster growth.

5. How to Track Your Money Success

If your bank talks about total sales but not local ownership, you need a new plan. Those are vanity marks that hide a weak spot. You can have many deals but no real power in the bank. To know if you are winning, you must track the “Dirty Four”:

Local Ratio: First, how many of your deals stay on your own tracks?

Shop Cost: Next, what is the total fee for every single scan?

Fast Speed: Then, for every coin paid, how fast does it reach the bank?

User Trust: Finally, when phone use grows, does your poor group get help?

Conclusion

How to win the money power race? It shifts from a secret to a system when you pick your goals well. You must set clear goals for the bank. Also, track gains with care using local data. Repeat this for 90 days. Then, growth becomes steady. This helps you spend your budget with trust.

Key Takeaways

First, payment sovereignty helps a nation control its own money because it removes the need for foreign tools.

Therefore, systems like UPI and QRIS serve as a bridge for trade and peace.

Specifically, the Digital Euro wants to give a public way to pay across all of Europe.

Furthermore, the QRIS model is growing fast to link Asian markets through easy scans.

Consequently, these tools allow small shops to take international money while they boost local sales.

In fact, India’s UPI has seen huge growth by making mobile phones the main way to join the bank.

For instance, having one set of rules helps lower the cost of every deal for the user.

Thus, using fast settlement stops the need for slow and very pricey old bank wires.

In addition, using live exchange rates builds quick trust when you travel to other lands.

Finally, keeping data local keeps your money safe and follows all your own laws.

FAQs

Q1: Can small lands afford their own pay tools?

Ans. Yes, tools like QRIS offer low-cost rules that work well for everyone.

Q2: How long before a new tool sees real growth?

Ans. Most systems see real gains and more users within 60 to 90 days of the start.

Q3: Is it better to focus on home use or foreign links?

Ans. Good local tracks work much better than relying on others in every test.

Q4: Will a Digital Euro take away my cash?

Ans. No, but it will act like a safe digital helper for all your phone buys.

Q5: What is the biggest risk for a big pay net?

Ans. Errors or bad data silos can be very bad, so make sure your tool has good backups.

Financial fragmentation can make traveling and trading between different nations very difficult because traditional currency exchange is often slow and expensive. However once you learn how Indonesia’s QRIS expansion connects Asian markets you will see a much smoother payment experience. I have analyzed how this cross border growth allows local businesses to accept international payments while seeing a massive boost in tourist spending.

The Problem With Traditional Currency Exchange

Many travelers still rely on physical cash or credit cards that charge very high fees for every international transaction. This approach creates a massive disconnect because users want a fast and digital way to pay for goods in a foreign country. You might feel frustrated when your local payment app fails to work the moment you cross a border. Traditional exchange methods are like carrying a heavy bag of coins and hoping every shop has the right change for you.

The solution lies in a unified digital system that works across different national boundaries instantly. Indonesia’s QRIS system allows a user to scan a single code to pay in their own currency while the merchant receives local funds. Once nations apply these interoperable standards you will see much higher trade efficiency across Asia. I have seen small vendors in Bali and Bangkok increase their sales by simply accepting digital payments from foreign visitors.

Strategy 1: Link Local QRIS to Regional Networks

Indonesia is actively connecting its national QR standard to other countries like Thailand, Malaysia, and Singapore. Specifically this link allows an Indonesian traveler to use their local banking app to pay for a meal in Kuala Lumpur. This integration removes the need for physical currency and lowers the cost for every person involved. Therefore you get a seamless experience that feels just like paying for something in your hometown.

Strategy 2: Implement Real Time Exchange Rates

Users love transparency because they want to know exactly how much they are spending in their own money. QRIS expansion uses real time rates to convert the price of a product at the exact moment of the scan. For example a shopper can see the cost in Rupiah even if the price tag is in Thai Baht. This level of detail builds immediate trust and encourages users to spend more during their travels.

Strategy 3: Optimize for Small Merchant Adoption

Many local businesses in Asia do not have expensive credit card machines because the fees are too high for their small margins. However QRIS is very cheap to implement since it only requires a printed code or a simple smartphone app. Because of this even the smallest street food stall can now accept international digital payments. This inclusion helps a wider range of local businesses benefit from the growth of regional tourism.

Strategy 4: Use QRIS to Drive Tourism Spending

A convenient payment system is a great way to encourage visitors to spend more money on local experiences. You can tell a traveler that they can pay for everything from a taxi ride to a luxury dinner using one single app. This creates a natural sense of ease that makes people more likely to choose Indonesia as their next destination. Consequently the local economy grows as digital friction disappears from the travel journey.

Strategy 5: Automate High Speed Settlement

Manual bank transfers between countries take a long time and often involve many different middlemen. However the QRIS cross border network uses advanced technology to settle transactions almost immediately. Your local business does not have to wait days to receive the funds from an international customer. Therefore you maintain a healthy cash flow and can restock your inventory without any delay.

Strategy 6: Provide Secure and Encrypted Transactions

Security is a primary concern for everyone who moves money across international borders today. QRIS uses high level encryption to ensure that every payment is safe from hackers and fraudulent activity. This ensures that both the customer and the merchant are protected during the digital handshake. Prompt and secure transactions help build a strong reputation for the Asian financial network as a whole.

Strategy 7: Collect Data for Regional Market Insights

Social proof and market data help you grow your business by showing you what your customers truly want. Indonesia’s central bank can use the data from QRIS to see which regions are seeing the most international spending. This allows the government to tailor its tourism and trade policies to match real world behavior. This simple step makes the entire regional economy much more responsive to changing user needs.

Strategy 8: Create a Seamless Bridge for Asian Trade

There are times when small businesses want to buy supplies from a neighboring country without opening a foreign bank account. You should use QRIS as a bridge that allows for easy business to business payments across Asia. This reduces friction and prevents small owners from having to deal with complex international wire transfers. A smooth payment bridge keeps the regional supply chain moving forward without any stops.

Strategy 9: Use Mobile Accessibility for Financial Inclusion

You want to make it as easy as possible for everyone to join the digital economy regardless of their location. Because many people in Asia use smartphones as their primary tool for internet access QRIS is the perfect solution. This saves people from the extra step of visiting a bank or carrying large amounts of cash. Therefore a single smartphone starts a financial journey that can lead directly to better economic health.

Strategy 10: Retarget International Shoppers Digitally

If a tourist buys from your shop using QRIS you can potentially use that connection to keep them engaged. For instance you can offer a digital loyalty card that stays in their mobile wallet for their next visit. This reminder should focus on the unique local experience your brand offers to every traveler. Remarketing with a personalized touch is a great way to win a repeat customer from across the globe.

Conclusion and Next Steps

If you follow the growth of this system you should soon see much better results for regional Asian trade. Please do not forget to let me know how you got on in the comments below. I am always interested in hearing your thoughts so tell me which part of this expansion you felt worked best for you.

FAQs

1 What is Indonesia’s QRIS expansion?

It is the growth of a unified QR payment standard that allows users to pay digitally across different Asian countries.

2 How does it help local Asian businesses?

It allows small merchants to accept international payments easily without expensive hardware or high fees.

3 Can I use QRIS in Thailand or Malaysia?

Yes, Indonesia has already established links with these countries to allow for cross border digital payments.

4 Is the QRIS system safe for travelers?

Yes, it uses advanced encryption and central bank oversight to ensure that every transaction is secure.

5 What is the first step for a business to accept QRIS?

The first step is to register with a participating bank or payment provider to receive your unique merchant QR code.

Is Blockchain a Revolution or Hype in Cross-Border Payments?

The world of global commerce depends entirely on the smooth movement of money. However, cross-border payments have long been plagued by high fees, frustrating delays, and a significant lack of transparency. Traditional systems, which rely on a complex network of correspondent banks, are slow and expensive. Therefore, they directly impact a business’s cash flow and profit margins. Naturally, a better solution is needed. Suddenly, blockchain technology arrived, promising to fix these exact pain points. Today, we investigate if this technology represents a true revolution or if it is merely overhyped. We must examine the core benefits to understand the future of international finance.

Understanding the Pain Points of Traditional Systems

Before discussing the solution, we should clearly understand the problem. Traditional cross-border payments, especially using the decades-old SWIFT network, involve many intermediaries. Specifically, a payment may pass through three or four banks before reaching its final destination. Therefore, each intermediary adds a fee, which quickly drives up the total cost. Furthermore, transactions often take three to five business days to settle. This delay is due to differing banking hours, time zones, and necessary manual compliance checks.

Consequently, businesses suffer from poor liquidity management and unpredictability. Moreover, tracking the payment’s exact location during this process can feel like operating in a black box, which creates uncertainty. Evidently, these legacy systems are inefficient and costly. This is where the decentralized ledger technology of blockchain steps in.

The Core Promise: Speed and Cost Reduction

The biggest appeal of blockchain in finance is its ability to bypass intermediaries. Since a blockchain is a distributed ledger, transactions move directly from the sender to the receiver on a peer-to-peer network. Therefore, this model radically simplifies the payment chain. Consequently, the transaction processing time drops from days to mere minutes or even seconds. This speed is a game-changer for international trade. Likewise, eliminating multiple correspondent banks removes the associated layering of fees. This reduction in cost is significant. For example, some blockchain-based solutions are reducing the total transaction costs by up to 80%. Clearly, the promise of near-instant and low-cost cross-border payments is highly appealing to businesses of all sizes, making it a powerful feature of the technology.

Enhanced Transparency and Security with Blockchain

In addition to speed and lower costs, blockchain delivers enhanced transparency and security. Because a transaction is recorded on a shared, immutable ledger, every authorized participant can see the payment’s status in real time. This end-to-end visibility is a stark contrast to the opaque nature of traditional systems. Therefore, this transparency significantly improves reconciliation and reduces disputes. Furthermore, the very nature of a blockchain—using cryptographic security—makes transactions highly tamper-proof. Once a block is added, it cannot be altered. Consequently, this decentralized security minimizes the risk of fraud and cyberattacks. As a result, companies gain a much higher degree of confidence in their cross-border payments. Ultimately, this trust is essential for global commerce.

Stablecoins and Liquidity Management

The volatility of cryptocurrencies is often cited as a challenge when discussing blockchain payments. However, stablecoins are solving this problem. Stablecoins are digital currencies pegged to fiat currencies like the US dollar. Therefore, they offer the speed and transparency of blockchain without the price swings of traditional crypto assets. Consequently, stablecoins are becoming the preferred rail for many modern cross-border payments. Furthermore, blockchain technology can also improve liquidity management. Banks and financial institutions often have to pre-fund accounts in various currencies across the globe to facilitate transfers. Now, blockchain’s real-time settlement capabilities and tokenized assets can reduce the need for large, trapped liquidity pools. Therefore, capital is deployed more efficiently across international markets. This optimization helps everyone.

The Role of Smart Contracts in Cross-Border Payments

The power of blockchain extends beyond simple money transfer; moreover, it introduces programmable money through smart contracts. Specifically, a smart contract is a self-executing agreement where the terms of the agreement are directly written into code. Consequently, these contracts automatically trigger a payment when certain predefined conditions are met. For example, a contract could release funds to a supplier immediately upon receiving confirmation of delivery from a logistics partner’s system. Therefore, this automation eliminates manual intervention and dramatically reduces operational risks. Furthermore, using smart contracts ensures compliance checks and regulatory reporting can be built directly into the transaction logic. Ultimately, smart contracts revolutionize the entire trade finance process, making the execution of cross-border payments faster, more reliable, and completely automated.

The Lingering Challenges: Regulation and Interoperability

Despite the numerous benefits, mass adoption of blockchain in finance is not without hurdles. Firstly, regulatory uncertainty remains a significant challenge. Different countries have varying rules regarding digital assets and distributed ledger technology. Therefore, navigating this fragmented legal landscape is complex for global financial institutions. Secondly, interoperability is a concern. Many different blockchain networks and private ledger systems exist, and they do not always communicate seamlessly with one another. Consequently, achieving a truly unified global system for cross-border payments requires significant standardization. Finally, integrating this new technology with older, legacy banking systems (the “core banking software”) requires a substantial investment in infrastructure and technical expertise. Therefore, the transition requires careful planning and a phased approach.

Hype or Revolution: The Verdict on Blockchain

When we look at the evidence, the impact of blockchain on cross-border payments is clearly more than just hype; moreover, it is a proven technology driving a revolution. While legacy systems like SWIFT are working to modernize, the core architectural advantages of decentralization, immutability, and real-time settlement offered by blockchain are fundamentally superior for global money movement. Solutions built on distributed ledger technology are already live, offering significant cuts in cost and time to businesses worldwide.

The challenges related to regulation and scalability are being actively addressed by global consortia and technology developers. Therefore, blockchain is not just a passing trend. Instead, it is the underlying technology that will redefine how money flows globally, ensuring a faster, cheaper, and more transparent future for cross-border payments.

Frequently Asked Questions (FAQs)

1. How does blockchain make cross-border payments faster?

Blockchain makes payments faster by eliminating the need for multiple intermediaries like correspondent banks. The payment is processed directly on a decentralized, peer-to-peer network. This allows for near-instant or real-time settlement, cutting transaction time from days to minutes.

2. Is using blockchain for international payments expensive?

No, in fact, it is typically much cheaper than traditional banking methods. Blockchain removes the layers of fees charged by multiple correspondent banks. The reduction in intermediaries can lead to cost savings of up to 80% on some cross-border payments.

3. What is the role of stablecoins in this process?

Stablecoins are digital currencies pegged to a stable asset, like the US dollar. They are used to leverage the speed and security of blockchain for payments without the price volatility associated with cryptocurrencies like Bitcoin, making them ideal rails for stable international value transfer.

4. What are the main challenges for widespread blockchain adoption in payments?

The main challenges include regulatory uncertainty, as rules vary significantly between countries. Additionally, there are issues with the interoperability of different blockchain platforms and the high initial cost and technical complexity of integrating this new technology with older banking infrastructure.

5. How does blockchain improve transparency and security?

Transparency is improved because all authorized network members can view the transaction on the immutable shared ledger in real-time. Security is enhanced through cryptographic encryption and the fact that once a transaction is recorded in a block, it cannot be altered or deleted.

The evolution of India’s payment ecosystem is marked by fast innovation. The launch of the Unified Payments Interface (UPI) was a landmark event. Now, the landscape for businesses is changing dramatically with the expansion of UPI 2.0 features and the global reach of UPI Global. It is vital for companies to understand these shifts. They must prepare to utilize the full power of this payments system. The ongoing evolution of UPI is cementing its place as one of the world’s most innovative payment platforms. It is succeeding both domestically and internationally.

UPI 2.0: Deepening the Domestic Digital Experience

The first version of UPI focused on speed and convenience. It made payments instant and interoperable. Then, UPI 2.0 launched with more powerful tools for both consumers and businesses. It especially supported higher-value transactions and complex financial commitments. These advanced features streamline operations effectively. Furthermore, they foster greater financial inclusion in the domestic market. Businesses must integrate these features quickly to stay ahead of their competition. The new features help manage money better.

Key Features of UPI 2.0 and How They Help

A very significant feature is the One-Time Mandate. This lets a customer pre-authorize a future payment. The funds are blocked in their account and then debited on a specific future date or upon delivery. Consequently, this feature is perfect for e-commerce. Payment can be mandated when the order is placed but deducted only when the product ships. Another important change is the ability to link Overdraft Accounts to a UPI ID. This grants customers a short-term line of credit for their transactions. Therefore, payments to businesses are less likely to fail because of insufficient account balance. This ensures smoother transactions for everyone.

Moreover, UPI 2.0 introduced the Invoice in the Inbox feature. This allows the customer to view a detailed digital invoice right along with the collect request in their payment app. This increases transaction transparency and builds trust. Security can be enhanced further. You can integrate Signed Intent and QR Codes. These codes verify the authenticity of both the merchant and the transaction securely. Ultimately, these UPI 2.0 features simplify all transactions for individuals and businesses. They combine convenience with robust safety for all users. Businesses must train their teams to use these new tools.

The Global Game-Changer: Preparing for UPI Global

While UPI 2.0 focused on enhancing the domestic experience, UPI Global is about expanding the system’s success onto the world stage. NPCI International Payments Limited (NIPL) is actively forging partnerships with various countries and payment networks. Their goal is to enable seamless, real-time cross-border transactions. This expansion often happens by linking UPI with a foreign country’s fast payment system, like PayNow in Singapore. For this reason, it fundamentally changes how international commerce is conducted today.

The Impact of Cross-Border UPI Transactions

The main benefit of UPI Global is the drastic reduction in the friction and cost of cross-border payments. Traditional international transfers, which often rely on slow, expensive intermediary banks, now face a real challenger. Consequently, this opens up massive opportunities for all businesses. This is especially true for MSMEs that previously found international expansion too complex or costly. Furthermore, this is particularly impactful for the remittance market. It allows Indian expatriates to send money home instantly and cheaply.

For e-commerce, the potential of UPI Global is truly enormous. International merchants can easily cater to the vast Indian consumer base. Also, Indian businesses can sell globally without complicated payment gateways. Therefore, businesses must prepare for these changes. They should ensure their payment processing systems can handle foreign exchange conversions and cross-border settlement with ease. This global reach, however, requires a new mindset for Indian businesses looking to expand their market footprint quickly.

Key Countries Adopting UPI Global

UPI Global has already made significant strides in several key markets. Singapore, for example, linked its PayNow system with UPI. This created a seamless channel for instant cross-border transfers between the two nations. Similarly, countries like the UAE, France (for tourist payments), Nepal, and Bhutan have adopted or are piloting UPI integration. Thus, these countries become much more accessible markets for Indian businesses. Businesses should prioritize technical integration with these countries first. Furthermore, they should closely monitor new partnership announcements by NIPL. This will help them identify the next big market opportunity quickly.

Business Strategy: Integrating the New UPI Ecosystem

To truly maximize the benefits of these advancements, businesses must develop a clear strategic roadmap. This roadmap should focus on integrating UPI 2.0 and preparing for UPI Global. Merely accepting UPI payments is no longer enough for growth. Active integration of its newest features is essential for optimizing cash flow, enhancing customer experience, and improving security across the board.

1. Optimize for UPI 2.0 Features for Better Cash Flow

First of all, integrate the One-Time Mandate feature for any subscription, installment, or post-delivery payment models your business uses. This feature dramatically improves payment success rates. It also provides predictable revenue streams, which is great for planning. Second, leverage the Invoice in the Inbox feature to provide rich context for every single transaction. This simple step builds customer trust effectively. Also, it significantly reduces payment-related queries or disputes for your support team. Finally, you can ensure security and customer confidence. You can do this by mandating the use of Signed QR codes at your Point of Sale (POS) terminals. This proactive step helps your business remain competitive by embracing the latest domestic payment technology.

2. Prepare for Seamless UPI Global Adoption

Businesses that deal with international customers or suppliers should immediately start planning for UPI Global. This preparation involves two main areas: technical preparedness and operational readiness. Technically, you should partner with a payment gateway that supports UPI‘s cross-border linkages. This gateway should also manage multiple currencies and Foreign Exchange (FX) rates in real-time. Operationally, you must update your accounting and reconciliation systems. They need to handle the increased volume of international, real-time transactions. This adoption is a critical step for any business with serious international ambitions for the future.

3. Focus on Seamless Reconciliation and Audit Trails

The real-time nature of UPI can sometimes complicate traditional accounting practices. Therefore, the implementation of robust, automated reconciliation systems is completely non-negotiable for serious businesses. Manual reconciliation of thousands of small, instant transactions is highly inefficient. It is also very prone to errors. By investing in technology that seamlessly matches UPI transaction data with sales and inventory data, your business gains superior visibility and control over its cash flow. This operational efficiency is the true long-term benefit of mastering the entire UPI ecosystem correctly. It saves time and money for the accounting department.

Overcoming Potential Challenges in the New UPI Era

While the rise of UPI is exciting, businesses must be aware of certain operational and security challenges. They can overcome these challenges with careful planning and smart technology investments.

Managing High Transaction Volumes

The sheer volume of UPI transactions is constantly growing. This places high demands on a business’s IT infrastructure. Businesses must make sure their payment gateways and server capacity can handle peak transaction loads. Furthermore, robust backup systems must be in place to prevent service interruptions. You can maintain reliable payment processing by scaling your infrastructure properly. In turn, this keeps customers happy and transactions flowing smoothly every time.

Security and Fraud Mitigation

The security features in UPI 2.0, like Signed QR, are powerful tools. However, businesses must remain vigilant against fraud. This involves training staff to recognize social engineering tactics. It also means educating customers about transaction security best practices. Since transactions are instant, recovery from fraud is difficult. Therefore, your business should invest in advanced fraud detection algorithms. These algorithms can analyze transaction patterns in real-time. This helps stop fraudulent activities before they can cause financial loss to your business.

Regulatory Compliance Across Borders

The expansion of UPI Global means dealing with multiple international regulations. This includes local Anti-Money Laundering (AML) and Know Your Customer (KYC) laws. Furthermore, data privacy laws vary significantly from country to country. Your business must ensure that its data handling and compliance procedures meet the requirements of every jurisdiction where you use UPI Global. Since regulations change frequently, you should consult with legal and compliance experts regularly. This essential step prevents costly legal issues down the road.

Conclusion: The Future is Real-Time and Global with UPI

The combination of UPI 2.0’s enhanced features and the expansive vision of UPI Global signals a future where digital payments are not just convenient. They are also powerful strategic tools for commerce. Businesses that embrace the One-Time Mandate, leverage the transparent invoicing features, and strategically prepare for cross-border payment flows will be perfectly positioned for impressive growth. The time to upgrade and strategize is definitely now. You can ensure your business thrives in this real-time, global payments era by taking action today. The ongoing success of UPI is a clear signal that the future of finance is open, fast, and highly inclusive for everyone.

FAQs About UPI 2.0 and UPI Global

1. How does the One-Time Mandate in UPI 2.0 benefit subscription-based businesses?

The One-Time Mandate allows a customer to pre-authorize a recurring or future payment. For subscription businesses, this secures the commitment from the customer upfront. This reduces failed payments significantly and improves predictable revenue. The money is blocked and debited automatically on the due date.

2. What security features were enhanced in UPI 2.0 for merchants?

UPI 2.0 introduced Signed Intent and QR Codes. These codes digitally sign the transaction, verifying the authenticity of the merchant to the customer’s payment app. This enhanced security measure minimizes the risk of fraudulent QR codes. It successfully builds greater trust in the payment process for all users.

3. What is the biggest advantage of UPI Global for small e-commerce businesses?

The biggest advantage is the ease of cross-border commerce. UPI Global significantly reduces the cost and complexity of accepting payments from international customers in countries like Singapore or the UAE. This allows small e-commerce businesses to easily access a much larger, global customer base for faster growth.

4. How will UPI Global affect Indian businesses with international suppliers?

UPI Global will enable much faster and cheaper payments to international suppliers in countries where UPI has established linkages. Consequently, this will significantly reduce transaction fees and settlement times. These reductions are compared to traditional banking channels. It greatly improves the business’s overall supply chain efficiency.

5. What is the immediate first step a business should take to prepare for UPI 2.0’s benefits?

The immediate first step is to work with your bank or Payment Service Provider (PSP) right away. You must ensure your payment integration supports the new UPI 2.0 APIs. This is especially important for the One-Time Mandate feature if your business model involves future or recurring payments to customers.