Global trade is moving faster than ever before. Most online stores now look for customers in every corner of the world. However, selling across borders brings many difficult hurdles. This is because every country has its own rules and preferred ways to pay. Therefore, businesses must find smart ways to handle these gaps. If they fail, they risk losing sales and trust. Successful e-commerce depends on a smooth and safe payment journey for everyone.

The Big Problems for Global Sellers

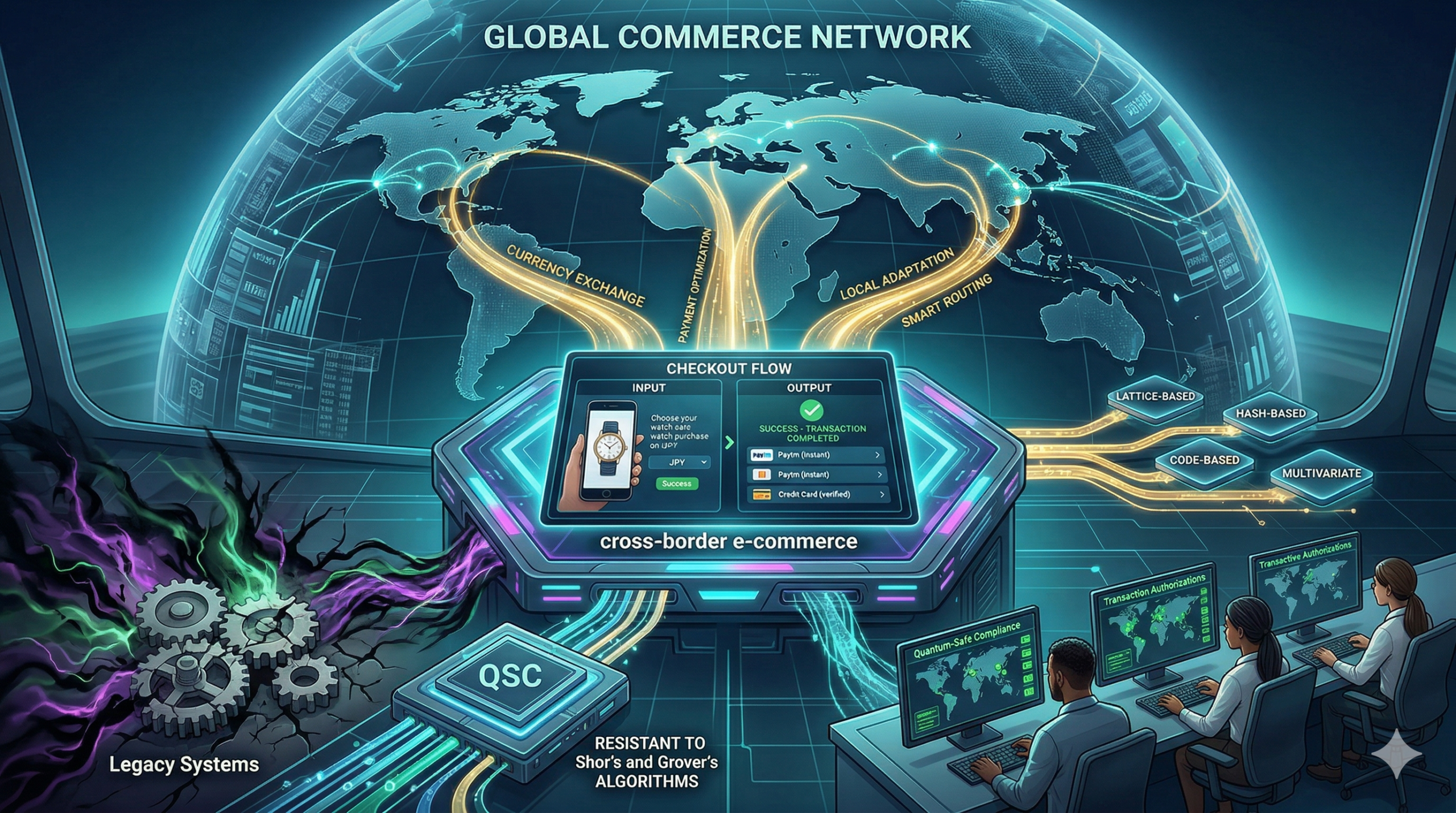

High fees are a major enemy of global growth. When a customer buys something from another country, banks often take a large cut. Consequently, the final price becomes too high for the shopper. This is because currency exchange rates are often unfair. Furthermore, hidden costs can surprise the customer at the final step. This leads to cart abandonment. Therefore, e-commerce firms must be very clear about all costs from the start.

Another big issue is the variety of payment habits. For instance, shoppers in Europe might prefer digital wallets. Meanwhile, customers in Asia might use QR codes or local bank transfers. If a store only offers credit cards, it will fail in these regions. Thus, a one-size-fits-all plan does not work. Every e-commerce site needs to adapt to local tastes to stay ahead.

Solutions for a Better Payment Journey

Multi-currency pricing is a vital tool for success. Customers want to see prices in their own money. Because this removes confusion, it builds instant trust. Furthermore, using a local acquiring bank can reduce transaction fees. This means the store keeps more profit while the user pays less. In short, e-commerce wins when the math is simple for the buyer.

Smart routing is another great way to fix failures. Sometimes, a bank might block a foreign payment by mistake. However, modern systems can instantly try a different bank to finish the sale. This keeps the flow moving without any delay. Because the user does not see the struggle, the experience feels like magic. Therefore, e-commerce platforms must use these intelligent tools to prevent lost sales.

Staying Safe Against Global Fraud

Security is the most important part of any global sale. Hackers are always looking for ways to steal data across borders. Luckily, new AI tools are great at spotting fraud by looking at millions of data points. If a transaction looks odd, the system stops it fast. This keeps your money and data very safe. Because the AI is so smart, it rarely blocks real customers. Thus, e-commerce stays strong and secure for everyone.

Additionally, 3D Secure 2.0 helps verify identity without making the process slow. It uses data to prove the user is real in the background. When you use these tools, the checkout flow feels very smooth. You just click and go. Therefore, the risk of a mistake or theft is very low. This is the future of e-commerce in a connected world. Finally, safety ensures that your brand grows a good name worldwide.

The Future of Global Trade

We are only at the start of a massive shift. Soon, every store will use local solutions to talk to global fans. This means we will see faster shipping and lower fees for everyone. Instead of a hard process, we get a tailored world of products. E-commerce makes every global transaction feel like a local one. It is the best way to trade in 2026. If you want to stay ahead, you must use these solutions now. In conclusion, a better payment journey is the key to global success.

Frequently Asked Questions

1. Why do global payments often fail?

They fail because banks might flag foreign cards as high-risk or due to technical errors in legacy systems.

2. How can I reduce currency exchange fees?

You should use a local payment provider or an e-wallet that offers better rates than traditional banks.

3. What is the best payment method for Asia?

Local digital wallets and QR-based systems are the most popular choices for shoppers in that region.

4. Does 3D Secure slow down my checkout?

No, the 2.0 version is much faster and often works in the background without bothering the user.

5. Is it hard to set up multi-currency pricing?

Most modern payment gateways offer this feature as a simple setting you can turn on.

In today’s fast-paced digital economy, every transaction tells a story. Indeed, raw payment data, often overlooked, holds an extraordinary wealth of information just waiting to be uncovered. Therefore, payment analytics emerges as a critical discipline, transforming this vast stream of transaction data into actionable growth insights. Truly, it allows businesses to move beyond simple reporting, delving deep into customer behavior, operational efficiency, and revenue opportunities. Clearly, by harnessing the power of these insights, companies can make smarter decisions, optimize their payment strategies, and ultimately drive sustainable growth. Furthermore, ignoring this valuable data means leaving money and opportunities on the table.

Many businesses view payment data merely as a record of financial exchange. However, this perspective severely limits its potential. In reality, payment analytics provides a 360-degree view of your customer’s purchasing journey, from initial interest to successful checkout. This comprehensive understanding enables businesses to identify trends, predict future behaviors, and proactively address challenges. Always remember, the goal is not just to process payments, but to learn from them. This strategic approach turns every swipe, click, or tap into a valuable piece of intelligence, guiding future business decisions with precision and foresight.

The Foundation of Payment Analytics: What It Is and Why It Matters

To begin with, let’s clearly define what payment analytics actually entails. Simply put, payment analytics is the process of collecting, processing, and analyzing data generated from every financial transaction a business handles. This data includes information such as transaction amounts, payment methods, customer locations, timestamps, and even fraud attempts. Consequently, by applying various analytical techniques, businesses can uncover patterns, correlations, and anomalies that are invisible to the naked eye. This deeper understanding is paramount for making data-driven decisions that impact the bottom line.

Why Payment Analytics is Indispensable for Modern Businesses

Naturally, the importance of payment analytics cannot be overstated in the current competitive landscape. Firstly, it offers an unparalleled view into revenue optimization. By understanding which payment methods are preferred, where conversion rates drop, or how different pricing strategies impact sales, businesses can fine-tune their offerings. Secondly, it plays a vital role in fraud detection and prevention. Analyzing transaction patterns helps identify suspicious activities in real time, significantly reducing financial losses and protecting customer trust. Clearly, a robust analytics system can be your first line of defense.

Furthermore, payment analytics dramatically enhances customer experience. By knowing customer preferences and pain points in the payment journey, companies can streamline checkout processes, offer preferred payment options, and provide a seamless experience. This leads to higher customer satisfaction and loyalty. Lastly, it drives operational efficiency. Identifying bottlenecks in payment processing, understanding chargeback reasons, or optimizing vendor relationships can lead to substantial cost savings. Therefore, payment analytics moves beyond mere financial reporting, becoming a strategic tool for continuous improvement and growth.

Key Metrics and Dimensions in Payment Analytics

To truly extract value from your payment data, you must focus on the right metrics and dimensions. Indeed, simply collecting data is not enough; you need to know what questions to ask. Consequently, identifying key performance indicators (KPIs) relevant to payments allows you to measure success, pinpoint areas for improvement, and track progress over time. Therefore, a clear understanding of these metrics is fundamental to any effective payment analytics strategy.

Essential Metrics for Deeper Insights

First, consider conversion rates at various stages of the payment funnel. How many customers initiate a checkout versus how many complete it? Tracking this helps identify drop-off points. Next, examine average transaction value (ATV), which provides insights into customer spending habits. A rising ATV suggests effective upselling or a higher perceived product value. Furthermore, payment method breakdown is crucial. Understanding which payment types (credit card, digital wallet, bank transfer) are most popular among different customer segments enables you to optimize your offerings.

Moreover, chargeback rates are critical for assessing fraud and customer dissatisfaction. A high chargeback rate indicates underlying issues that need immediate attention. You should also track payment success rates, identifying any recurring errors or declines that might be deterring customers. Additionally, transaction volume and frequency over time can reveal seasonal trends and peak periods, informing staffing and inventory decisions. Finally, customer lifetime value (CLV), when viewed through the lens of payment data, offers insights into the long-term profitability of different customer segments. Truly, a holistic view of these metrics empowers businesses to make informed, impactful decisions.

Leveraging Payment Analytics for Revenue Optimization

One of the most immediate and impactful benefits of payment analytics is its ability to directly influence revenue. By scrutinizing transaction data, businesses can uncover opportunities to increase sales, improve conversion rates, and enhance profitability. Clearly, a deeper understanding of payment trends allows for targeted strategies that resonate with customer preferences and overcome potential hurdles in the buying journey. Therefore, every business aiming for growth must prioritize this area.

Strategies for Boosting Your Top Line

Firstly, use payment analytics to optimize your payment mix. By identifying the most preferred payment methods for different demographics or regions, you can ensure these options are prominently displayed and seamlessly integrated. For example, if mobile wallet usage is surging in a particular market, prioritizing that option can significantly boost conversions. Secondly, analyze data to identify and mitigate conversion bottlenecks. Perhaps a specific payment gateway consistently experiences higher failure rates, or customers abandon carts at the final payment step. Pinpointing these issues allows for targeted improvements, such as switching providers or simplifying the checkout flow.

Furthermore, payment analytics assists in dynamic pricing and promotions. Understanding how different price points or discount structures impact payment behavior and overall revenue enables businesses to tailor offers more effectively. For instance, you might discover that a specific payment method user responds better to loyalty rewards. Also, analyze subscription payment data to reduce churn. Identifying patterns in failed recurring payments, such as expired cards, allows for proactive communication and retries, thereby preserving recurring revenue. Ultimately, this strategic application of payment data ensures you’re not just processing transactions, but actively growing your revenue streams.

Enhancing Security and Fraud Prevention with Payment Analytics

In the digital landscape, where cyber threats are constantly evolving, safeguarding transactions against fraud is paramount. Payment analytics plays an indispensable role in strengthening security measures and proactively detecting suspicious activities. Consequently, by analyzing payment data patterns, businesses can build more robust fraud prevention systems, protect their financial integrity, and maintain customer trust. Clearly, neglecting this aspect can lead to significant financial losses and reputational damage.

Building Robust Fraud Detection Systems

Firstly, payment analytics enables the identification of unusual transaction patterns. Fraudulent activities often deviate significantly from normal purchasing behavior. For example, multiple small purchases from different geographic locations in a short period, or unusually high-value transactions from new customers, can be red flags. By establishing baselines of normal behavior, analytics systems can flag these anomalies for further investigation. This real-time detection is crucial for mitigating damage.

Secondly, you can use payment data to enrich fraud models. Integrating data points like IP addresses, device fingerprints, shipping addresses, and customer transaction history provides a more comprehensive picture for machine learning-based fraud detection algorithms. These algorithms learn from past fraudulent and legitimate transactions to predict future risks with high accuracy. Furthermore, analytics helps in reducing false positives. While aggressive fraud detection can block legitimate transactions, payment analytics refines the rules, ensuring that valid customers can complete their purchases without unnecessary friction, thereby improving the customer experience. Ultimately, leveraging payment analytics for fraud prevention transforms your security from a reactive measure into a proactive, intelligent defense mechanism.

Driving Operational Efficiency and Customer Experience

Beyond revenue and security, payment analytics offers profound benefits for streamlining operations and elevating the customer experience. In fact, by understanding the intricate details of how payments flow through your systems and how customers interact with them, businesses can identify inefficiencies and pinpoint areas for service improvement. Truly, an optimized payment journey directly translates into higher customer satisfaction and loyalty.

Streamlining Processes and Delighting Customers

Firstly, payment analytics helps in optimizing payment gateway performance. By monitoring success rates and latency across different providers, businesses can identify underperforming gateways or regions where specific providers excel. This allows for intelligent routing of transactions, ensuring higher success rates and faster processing times. Furthermore, analyzing transaction failure reasons—such as insufficient funds, incorrect card details, or technical errors—enables proactive communication with customers or internal system adjustments, thereby reducing abandoned carts.

Secondly, analytics provides insights into customer payment preferences, which is vital for enhancing the user experience. For instance, if a significant portion of your mobile users prefers digital wallets, making those options easily accessible and intuitive can significantly improve checkout speed and convenience. Conversely, if a particular region heavily relies on bank transfers, ensuring that option is robustly supported is crucial. Moreover, understanding chargeback reasons goes beyond fraud; it can reveal issues with product delivery, unclear billing, or poor customer service, prompting improvements across various operational touchpoints. In sum, payment analytics empowers businesses to fine-tune every aspect of their payment infrastructure, leading to smoother operations and a superior experience for every customer.

Frequently Asked Questions (FAQs)

Q1: What kind of data is included in payment analytics?

Payment analytics includes a wide range of transaction data, such as transaction amounts, timestamps, payment methods used (credit card, digital wallet, bank transfer), customer location, currency, device used for payment, success/failure status, and details related to chargebacks or refunds. It can also incorporate demographic and behavioral data if available.

Q2: How can payment analytics help reduce cart abandonment?

Payment analytics helps reduce cart abandonment by identifying common drop-off points and reasons for transaction failures. By analyzing data on where customers leave the checkout process, which payment methods fail most often, or what technical errors occur, businesses can pinpoint issues and make targeted improvements to streamline the payment flow and improve success rates.

Q3: Is payment analytics only useful for large enterprises?

Absolutely not! While large enterprises often have vast amounts of data, payment analytics is equally beneficial for small and medium-sized businesses (SMBs). Even with smaller transaction volumes, SMBs can gain valuable insights into customer preferences, identify fraud patterns, optimize payment costs, and improve their overall operational efficiency, leading to significant growth.

Q4: How does payment analytics contribute to better customer experience?

Payment analytics enhances customer experience by allowing businesses to understand and cater to customer preferences. By knowing which payment methods are preferred, which parts of the checkout process cause friction, or why transactions fail, companies can optimize their payment offerings, simplify the checkout flow, and provide proactive support, leading to smoother, more satisfying interactions.

Q5: What’s the difference between payment analytics and general financial reporting?

General financial reporting typically focuses on historical data to track overall financial health (e.g., total revenue, expenses, profits). Payment analytics, however, delves much deeper into the details of payment transactions to uncover actionable insights, predict future trends, optimize processes, and identify specific opportunities for growth, fraud prevention, and customer experience improvement.

Every business that accepts card payments faces the threat of chargebacks and disputes. These are not just minor inconveniences. They can lead to significant financial losses. They also harm your reputation. Moreover, they can even cause your payment processor to impose higher fees or close your account. Understanding the root causes of these issues is the first step. Developing a strong strategy to combat them is essential. This is crucial for any business wanting to protect its bottom line and ensure long-term stability in the digital marketplace.

Minimizing losses from chargebacks and disputes requires a multi-faceted approach. It involves careful prevention measures. It also needs robust management processes. Finally, it requires effective representment tactics. Many businesses simply absorb the losses. They see them as a cost of doing business. However, a proactive stance can transform this challenge. It can turn it into an opportunity. This opportunity allows for improved customer service. It also helps refine internal processes. Thus, businesses can not only recover funds. They can also build stronger relationships with customers. They can also enhance their operational efficiency.

Understanding the Landscape: Types of Chargebacks & Disputes

To minimize losses from chargebacks and disputes, you must know their various forms. Each type has a distinct cause. Therefore, each requires a specific approach to prevention and resolution. Broadly, these issues fall into a few main categories: fraud, merchant error, and friendly fraud (or consumer disputes). Knowing these differences is key. It helps in building effective defense mechanisms.

Fraudulent chargebacks and disputes occur when an unauthorized transaction happens. A stolen card may be used. Or, account information might be compromised. These are often the most straightforward to identify. Merchant error disputes happen when a business makes a mistake. This could be double billing. It could be shipping the wrong item. It could also be poor customer service. Friendly fraud is the most complex. It happens when a customer makes a legitimate purchase. Then, they dispute it, often claiming it was unauthorized. They may also claim non-receipt, despite getting the goods. This can stem from confusion. It can also be intentional deceit. Each type demands a tailored response.

Proactive Prevention: Stopping Chargebacks Before They Start

The best way to minimize losses from chargebacks and disputes is to prevent them. This involves implementing robust strategies across various business operations. Strong prevention reduces the number of cases you face. It also strengthens your customer relationships. Many disputes arise from simple misunderstandings. Others come from security gaps. Addressing these areas effectively can significantly reduce your risk.

Key prevention strategies for chargebacks and disputes include:

Clear Communication: Ensure all product descriptions are accurate. Display pricing clearly. State shipping and return policies explicitly. Furthermore, use descriptive billing descriptors. These help customers recognize transactions on their statements.

Enhanced Security Measures: Implement advanced fraud detection tools. Use AVS (Address Verification Service). Also, use CVV (Card Verification Value) checks. Consider 3D Secure for higher-risk transactions. These layers of security deter fraudsters. They also provide stronger evidence in case of a dispute.

Exceptional Customer Service: Provide easily accessible and responsive customer support. Many customers initiate a dispute because they cannot resolve an issue directly with the merchant. Offering quick solutions can prevent many chargebacks and disputes. This also builds customer loyalty.

Prompt Order Fulfillment: Ship products quickly. Provide tracking information. Avoid delays. Communicate any expected delays clearly. Non-receipt claims are a common reason for disputes. Fast and trackable shipping reduces this risk.

Transparent Refund Policies: Make your refund and return policies easy to find. Make them easy to understand. Also, make them easy to follow. A fair and clear policy helps customers resolve issues without resorting to a chargeback.

Effective Management: Responding to Disputes Swiftly

Despite your best prevention efforts, some chargebacks and disputes will still occur. The way you manage these situations once they arise is crucial. A swift and organized response can often mitigate the financial impact. It can even lead to successful reversal of the dispute. Delays, on the other hand, often result in automatic losses.

A critical step in managing chargebacks and disputes is setting up clear internal processes. Designate a team or individual to handle these cases. Ensure they are well-trained. They must understand the timelines. They also need to know the specific evidence required for each type of dispute. Most payment networks have strict deadlines for responding. Missing these deadlines almost guarantees a loss. Implement a system for tracking all disputes. This helps monitor their status. It also aids in identifying trends. This allows you to improve your prevention strategies over time.

Additionally, consider using technology to streamline this process. Chargeback management software can automate data collection. It can also help organize evidence. It can even submit representment cases. This reduces manual effort. It also increases the chances of winning. Furthermore, maintain excellent records of all transactions. Keep customer interactions, shipping proofs and IP addresses. All these are vital for successful dispute resolution.

The Art of Representment: Fighting Back Against Unjust Claims

Representment is the process of providing evidence to your bank. This evidence challenges a customer’s chargeback and disputes claim. It is your chance to recover funds. It also proves the legitimacy of your transaction. This is especially important for friendly fraud. Many businesses avoid representment. They see it as too complex. However, winning a representment case can save significant money.

Successful representment against chargebacks and disputes demands compelling evidence. The type of evidence needed varies. It depends on the reason code for the dispute. Common pieces of evidence include:

Proof of Delivery: Tracking numbers, delivery confirmations, customer signatures.

Transaction Details: Date, time, amount, product purchased, customer IP address.

Terms and Conditions: Evidence that the customer agreed to your policies (e.g., checkout screenshots).

Prior History: Evidence of past successful transactions with the same customer. This helps in friendly fraud cases.

Refund/Cancellation Policy: Proof that your policy was clear and followed.

Assemble a complete and clear case. Present it within the given timeline. A well-organized representment package greatly increases your chances of winning. It allows you to recover funds that would otherwise be lost. Furthermore, winning representment cases helps protect your merchant account. It shows you are actively managing your risk.

Analyzing Data: Learning from Every Chargeback

Every chargeback and disputes case offers valuable insights. Analyzing the data from these events is critical. It helps to continuously improve your prevention and management strategies. Look beyond just the number of chargebacks. Examine the reasons behind them. Identify common themes. This data-driven approach allows you to pinpoint weaknesses. It helps you strengthen your defenses over time.

Key areas for data analysis include:

Reason Codes: Which reason codes appear most frequently? Are they related to fraud, merchant error, or friendly fraud? This tells you where to focus your prevention efforts.

Product/Service Trends: Are certain products or services generating more disputes? This might indicate a description issue. It could also point to a quality problem.

Customer Segments: Are disputes more common from specific customer demographics or regions? This could highlight potential fraud hotspots.

Time Lags: Is there a pattern in how long it takes for a dispute to be filed after a transaction? This can inform your monitoring strategies.

Representment Success Rates: Which types of cases are you winning? Which are you losing? This helps refine your evidence gathering. It also improves your representment strategies.

By consistently reviewing this data, businesses can make informed decisions. They can adjust their payment gateway settings and can refine their customer service scripts. They can improve product descriptions. This iterative process is crucial. It minimizes losses from chargebacks and disputes over the long term.

The Role of Technology: Tools to Fight Chargebacks

Modern technology offers powerful tools. These tools help businesses combat chargebacks and disputes. Leveraging these solutions can automate processes. They can also enhance accuracy. This allows you to scale your protection efforts. Manually managing every dispute becomes impossible as businesses grow. Technology provides the necessary efficiency.

Key technologies and services for minimizing losses from chargebacks and disputes include:

Fraud Detection Systems: AI-powered solutions analyze transactions in real-time. They identify suspicious patterns. They flag high-risk orders before fulfillment.

Chargeback Management Software: These platforms centralize dispute data. They automate the evidence collection process. They also help with representment submission.

Order Fulfillment Integration: Connecting your payment system with shipping and inventory management. This ensures consistent data for proof of delivery.

Customer Relationship Management (CRM) Systems: A good CRM captures all customer interactions. This provides a clear record for dispute resolution.

Payment Gateway Features: Many gateways offer built-in tools. These include AVS, CVV, and 3D Secure. They also offer negative lists for blocking known fraudsters.

Integrating these technologies creates a robust defense system. It works against chargebacks and disputes and protects your revenue. It also frees up valuable staff time. This allows them to focus on core business activities. This makes it a smart investment for any growing business.

Frequently Asked Questions (FAQs)

1. What is the most common reason for chargebacks?

The most common reasons for chargebacks and disputes typically fall into three categories: fraud (unauthorized transactions), merchant error (e.g., wrong item, double billing), and friendly fraud (customer disputes a legitimate purchase). Friendly fraud, especially, is on the rise and often stems from customer confusion or intent to deceive.

2. How can good customer service prevent chargebacks?

Exceptional customer service can significantly prevent chargebacks and disputes. Many customers initiate a dispute because they feel unable to resolve an issue directly with the merchant. Providing quick, accessible, and helpful support offers an alternative. It allows customers to address their concerns without resorting to a chargeback.

3. What is representment, and how important is it?

Representment is your process of fighting a chargeback and disputes claim. You provide evidence to your bank. This evidence proves the transaction was legitimate. It is very important. Successfully winning a representment case allows you to recover lost funds. It also protects your merchant account status.

4. What types of evidence are most effective in winning a chargeback dispute?

The most effective evidence depends on the specific reason code for the chargeback and disputes. Generally, strong evidence includes proof of delivery (tracking), customer communication logs (chats, emails), transaction details (IP address, order details), and proof that the customer agreed to your terms and conditions at checkout.

5. Can technology truly help reduce losses from chargebacks?

Yes, technology plays a vital role in reducing losses from chargebacks and disputes. Fraud detection systems, chargeback management software, and payment gateway features (like AVS/CVV/3D Secure) automate prevention and management. These tools streamline evidence collection. They also enhance your chances of winning disputes.

E-commerce businesses constantly face a growing and evolving threat from online fraud. As digital payments become more common, criminals invent increasingly sophisticated ways to exploit vulnerabilities. For many merchants, this results in significant financial losses, mainly from high chargeback rates and the operational costs of manual reviews. Therefore, businesses must shift from reactive security measures to a proactive, intelligent defense. Traditional systems, often built on static rules, are simply no match for modern criminal networks. Consequently, integrating advanced AI e-commerce fraud prevention at the earliest point—the payment gateway—is not merely an option; it is a fundamental necessity for survival and growth. This transformative step helps protect both revenue and valuable customer trust in the digital marketplace.

Why Traditional Rules Fail Against Modern Scams

Older, rule-based fraud detection systems operate on rigid, predefined criteria. For instance, a rule might automatically flag any transaction over $500 or any purchase using a foreign IP address. While simple, this approach has two major flaws. Primarily, it leads to unacceptable rates of false positives, which wrongly decline legitimate customers, causing frustration and lost sales. Furthermore, static rules are easy for experienced fraudsters to learn and bypass.

Consequently, criminals continually adapt their methods, making the old systems quickly obsolete. Because of this adaptability, a truly effective defense requires a system that can learn and evolve faster than the fraud itself. The core problem lies in their inability to detect never-before-seen or subtle patterns of deceit. This is precisely where the dynamic power of AI fraud detection offers an unbeatable advantage to all e-commerce players.

Machine Learning: The Engine of Next-Generation Security

The central component of effective modern fraud defense is machine learning. This is a type of artificial intelligence that uses vast amounts of historical and real-time transaction data to find complex patterns. Unlike rules, machine learning models do not just look for a single red flag. Instead, they analyze hundreds of data points simultaneously, including device IDs, geographic locations, purchase velocity, and behavioral anomalies. The models train on labeled data (known fraud vs. legitimate sales) to build a probabilistic risk score for every single transaction.

Moreover, unsupervised learning models are crucial for identifying totally new and unexpected types of fraud that do not fit any known pattern. This capability to detect both known and unknown threats makes machine learning fraud detection the gold standard for AI e-commerce fraud prevention. The continuous feedback loop further allows the system to improve its accuracy with every transaction, making it truly adaptive.

Real-Time Transaction Analysis at the Gateway

For maximum effectiveness, fraud screening must happen before the transaction is authorized. Therefore, integrating AI directly into the payment gateway security system is essential. This allows for what is called real-time transaction analysis. Within milliseconds—faster than a customer can even notice—the AI model assesses the risk score. It analyzes hundreds of data features, cross-referencing them against known fraud rings and establishing the user’s normal behavioral baseline.

Consequently, if the score is too high, the gateway can instantly reject the transaction, stopping the fraudster before any loss occurs. Conversely, if the score is moderate, the system can introduce step-up authentication, such as a two-factor verification, without declining a potentially good customer. This immediate action is vital because a slow decision allows fraudsters to execute their attack plans. This speed ensures a seamless experience for legitimate customers while providing a rock-solid layer of protection at the most critical moment of the e-commerce checkout flow.

Combating Card-Not-Present (CNP) and Account Takeover (ATO) Fraud

The biggest challenge in e-commerce is the proliferation of card-not-present (CNP) fraud. Since the physical card is absent, fraudsters use stolen card details to make online purchases. AI addresses this by moving beyond simple CVV and AVS checks. It employs device fingerprinting to track suspicious devices and IP addresses used in multiple attempts. Furthermore, AI is the best defense against Account Takeover (ATO) attacks. ATO occurs when a fraudster gains unauthorized access to a legitimate customer’s account.

Because of this danger, the AI fraud detection system monitors behavioral biometrics—things like typing speed, mouse movements, and navigation patterns. Any significant deviation from the customer’s established habits immediately triggers an alert or an enhanced authentication step. This layered, behavioral approach is highly effective. Ultimately, AI not only prevents CNP fraud but also protects the integrity of loyal customer accounts against unauthorized use.

The Hidden Advantage: Reducing False Positives and Chargebacks

A major unseen cost of outdated fraud systems is the revenue lost from false positives. When a legitimate customer’s transaction is blocked, the business not only loses that sale but also risks losing the customer forever. Importantly, AI e-commerce fraud prevention significantly lowers this problem. Through its superior pattern recognition, machine learning models identify nuances that differentiate a high-value returning customer from a fraudster using a similar transaction size. This improved accuracy means fewer good customers are rejected, which directly boosts conversion rates and customer satisfaction.

Furthermore, by preventing fraud more effectively, the system naturally reduces the number of successful fraudulent transactions. This reduction in fraud directly translates to lower e-commerce chargebacks with AI, saving the business costly fees and protecting its relationship with acquiring banks and payment networks. Therefore, the return on investment in an AI solution is twofold: reduced losses and increased revenue from legitimate sales.

Adaptive Fraud Prevention Solutions and Future Trends

Fraud is not static; it is a constantly evolving challenge. The core strength of AI e-commerce fraud prevention lies in its ability to adapt in real time, which is essential for long-term security. These adaptive fraud prevention solutions use continuous learning to adjust their models automatically as new fraud schemes appear. When a new coordinated attack begins, the AI detects the anomalous cluster of transactions and instantly updates its risk scoring criteria to block the emerging pattern globally. This prevents the same attack from succeeding across all accounts.

Looking ahead, the future of payment gateway security will involve the integration of new technologies. We will see greater use of federated learning, where multiple banks and merchants securely share non-sensitive fraud patterns to build more robust global models without compromising customer data. The continued focus remains on creating a friction-free experience for the customer while building an invisible, iron-clad defense against all fraudulent activity. The speed and scalability of AI make this future a reality right now.

Building Your Defense: Implementing AI at the Gateway

Implementing a robust AI e-commerce fraud prevention solution requires a strategic approach. First, e-commerce managers must work closely with their payment gateway provider or a specialized fraud solution vendor. The initial phase involves integrating the AI tool seamlessly with the gateway’s transaction processing API. Next, the system requires training on the business’s historical transaction data to establish a baseline for normal customer behavior.

During live deployment, starting in a “monitor only” mode is smart, allowing the AI model to score transactions without automatically blocking them. This parallel testing ensures accuracy and helps fine-tune the risk thresholds. Importantly, the team must establish clear review processes for transactions that the AI flags for manual review. By prioritizing a phased, data-driven rollout, businesses can maximize the effectiveness of real-time transaction analysis and secure their checkout process quickly and confidently.

The Final Verdict: AI is the Non-Negotiable E-Commerce Shield

The relentless increase in digital fraud means that simple, rule-based systems are functionally obsolete. E-commerce businesses cannot afford to sustain high chargeback rates, manual review costs, and the customer frustration caused by false positives. The move to AI e-commerce fraud prevention offers the only scalable, adaptive, and accurate solution. By integrating machine learning fraud detection directly into the payment gateway, businesses create an intelligent, real-time shield that protects every transaction. This advanced security not only stops criminals but also enhances the customer experience by processing legitimate transactions swiftly and without unnecessary friction. Adopting these advanced solutions is the key to maintaining a competitive edge and ensuring long-term financial stability in the fast-paced world of online retail.

Frequently Asked Questions (FAQs)

1. What is the main difference between traditional and AI fraud detection?

The main difference is adaptability. Traditional systems use static rules that are easy to bypass, while AI e-commerce fraud prevention uses machine learning to continuously analyze new data and adapt its models to detect emerging fraud patterns in real time.

2. How does AI help to reduce e-commerce chargebacks with AI?

AI fraud detection significantly reduces chargebacks by proactively identifying and blocking fraudulent transactions before they are approved and completed, thereby lowering the number of unauthorized transactions reported to card issuers.

3. What is behavioral biometrics in e-commerce and how is it used?

Behavioral biometrics in e-commerce involves analyzing unique user actions like typing speed, mouse movements, and scrolling patterns. Real-time transaction analysis uses this data to verify a user’s identity, making it a strong defense against account takeover fraud.

4. Does AI fraud detection cause a delay in transaction processing?

No, the analysis is nearly instantaneous. AI-powered payment gateway security systems complete their risk assessment and scoring in milliseconds, meaning the vast majority of transactions are processed without any noticeable delay to the customer.

5. What is the role of unsupervised learning in machine learning fraud prevention?

Unsupervised learning models are critical because they detect entirely new and unknown types of fraud. They identify transactions that are significant statistical outliers from all established, normal behavior, allowing for a defense against emerging threats without prior examples.

Have you shopped online? Online fraud is what you can come across if not aware, Online fraud is false deception intentionally made for financial gains. Online frauds are of different types:

Online Spoofing

Online Phishing.

Triangulation fraud.

Data Theft

Chargeback fraud.

Online Spoofing:

Spoofing is the creation of spam emails that look genuine and trick businesses to take action. No one would knowingly download a Trojan package into the system unless provoked to do it by putting fake popups on security threats for the system. How it’s done? Well, genuine-looking mail is created with corporate graphics of reputed service providers which will guide you on how to protect your business. This professional graphic makes the mail look genuine and tricks businesses to click on the link in the mail. This link executes malicious software which harms the operating system and critical files, it expands through the network and affects clients as well.

How to prevent Spoofing?

-When you receive such suspicious emails best thing to do is hover over the senders’ address, hackers have a domain name that is very much similar to legitimate domain names, so check for spelling mistakes.

-Legitimate institute never sends an attachment like .exe, .bat, or zip, check if the email has an attachment. Red flag the mail and do not follow any instructions written in the mail.

Online Phishing:

Phishing is a form of Spoofing but unlike Spoofing where attackers tend to break into the system and fetch information, Phishing is tricking the end-user to reveal sensitive information wherein a genuine-looking message is forwarded to the end-user which consists of a fake website link. This link redirects the end user to a bogus website that asks for sensitive account-related information. Revealing this information can harm your financial assets.

How to prevent Phishing?

-There is no problem in clicking on the links when you are on a trusted site, but when it comes to clicking on the links within the email or message you need to be 100% sure as these links can be spam links. Before clicking on such a link hover over the email and check if the links direct to what it actually shows. Do not fill in any personal data on such sites as it can be a lure to steal your data.

-Install Anti Phishing tools on a browser as these tools scan the entire websites and check with a list of phishing sites. If you visit any malicious sites the tool prompts immediately, do not visit the site.

Triangulation fraud:

Triangular fraud as the name suggests involvement of three people,

How fraud is done? A legitimate-looking website is made by a fraud seller who displays some items at very low prices, which makes the customers buy the products. The customer is unaware of the fraud happening and places an order on this fake website. The fraud seller has stolen credit card information which he uses to make the purchase of those products for which an order has been placed on his fake website. He purchases these products from a genuine website. The customer receives all the updates with the respective product from the seller. The seller sends these updates from a genuine site to the customer.

Who is the criminal? The seller with a stolen credit card is the criminal.

Victims? Well, there are two victims, the customer, If the fraud is discovered, the genuine website will contact the customer to return the stolen products.

and the person whose credit card details were used for transactions is a victim as he is unaware of those transactions.

How to prevent Triangulation fraud?

-Speak with the customer who doubts suspect triangulation fraud, and gather as much information as possible about the seller to determine the fake website.

-Focus on the products as the seller has some list of common products which sell very frequently, this can help to analyze the pattern of fraud.

Chargeback fraud:

Chargeback is the term used for an order from a bank to a business to return the amount paid for a fraudulent purchase. How is a chargeback fraud done? The customer makes a payment through a payment gateway for certain goods or services, later on, he/she claims that the purchase was made fraudulently or makes a false request that the goods were not delivered and claims for a chargeback. When a transaction seems legitimate then chargeback is the only way to get the money back.

How to prevent Chargeback Fraud?

The customer claims a chargeback for many reasons so the first step will be to identify the reason for a chargeback. Sometimes the customer can claim a chargeback if the description doesn’t go with the product when delivered. So work on the description to avoid a chargeback.

-Use delivery confirmation to ensure that the product has been delivered to the customer, at times it happens that a customer is not at home and the package is left on the porch which can be stolen, so for you, the item is delivered but the customer did not receive the product for which chargeback can be claimed.