Global trade is moving faster than ever before. Most online stores now look for customers in every corner of the world. However, selling across borders brings many difficult hurdles. This is because every country has its own rules and preferred ways to pay. Therefore, businesses must find smart ways to handle these gaps. If they fail, they risk losing sales and trust. Successful e-commerce depends on a smooth and safe payment journey for everyone.

The Big Problems for Global Sellers

High fees are a major enemy of global growth. When a customer buys something from another country, banks often take a large cut. Consequently, the final price becomes too high for the shopper. This is because currency exchange rates are often unfair. Furthermore, hidden costs can surprise the customer at the final step. This leads to cart abandonment. Therefore, e-commerce firms must be very clear about all costs from the start.

Another big issue is the variety of payment habits. For instance, shoppers in Europe might prefer digital wallets. Meanwhile, customers in Asia might use QR codes or local bank transfers. If a store only offers credit cards, it will fail in these regions. Thus, a one-size-fits-all plan does not work. Every e-commerce site needs to adapt to local tastes to stay ahead.

Solutions for a Better Payment Journey

Multi-currency pricing is a vital tool for success. Customers want to see prices in their own money. Because this removes confusion, it builds instant trust. Furthermore, using a local acquiring bank can reduce transaction fees. This means the store keeps more profit while the user pays less. In short, e-commerce wins when the math is simple for the buyer.

Smart routing is another great way to fix failures. Sometimes, a bank might block a foreign payment by mistake. However, modern systems can instantly try a different bank to finish the sale. This keeps the flow moving without any delay. Because the user does not see the struggle, the experience feels like magic. Therefore, e-commerce platforms must use these intelligent tools to prevent lost sales.

Staying Safe Against Global Fraud

Security is the most important part of any global sale. Hackers are always looking for ways to steal data across borders. Luckily, new AI tools are great at spotting fraud by looking at millions of data points. If a transaction looks odd, the system stops it fast. This keeps your money and data very safe. Because the AI is so smart, it rarely blocks real customers. Thus, e-commerce stays strong and secure for everyone.

Additionally, 3D Secure 2.0 helps verify identity without making the process slow. It uses data to prove the user is real in the background. When you use these tools, the checkout flow feels very smooth. You just click and go. Therefore, the risk of a mistake or theft is very low. This is the future of e-commerce in a connected world. Finally, safety ensures that your brand grows a good name worldwide.

The Future of Global Trade

We are only at the start of a massive shift. Soon, every store will use local solutions to talk to global fans. This means we will see faster shipping and lower fees for everyone. Instead of a hard process, we get a tailored world of products. E-commerce makes every global transaction feel like a local one. It is the best way to trade in 2026. If you want to stay ahead, you must use these solutions now. In conclusion, a better payment journey is the key to global success.

Frequently Asked Questions

1. Why do global payments often fail?

They fail because banks might flag foreign cards as high-risk or due to technical errors in legacy systems.

2. How can I reduce currency exchange fees?

You should use a local payment provider or an e-wallet that offers better rates than traditional banks.

3. What is the best payment method for Asia?

Local digital wallets and QR-based systems are the most popular choices for shoppers in that region.

4. Does 3D Secure slow down my checkout?

No, the 2.0 version is much faster and often works in the background without bothering the user.

5. Is it hard to set up multi-currency pricing?

Most modern payment gateways offer this feature as a simple setting you can turn on.

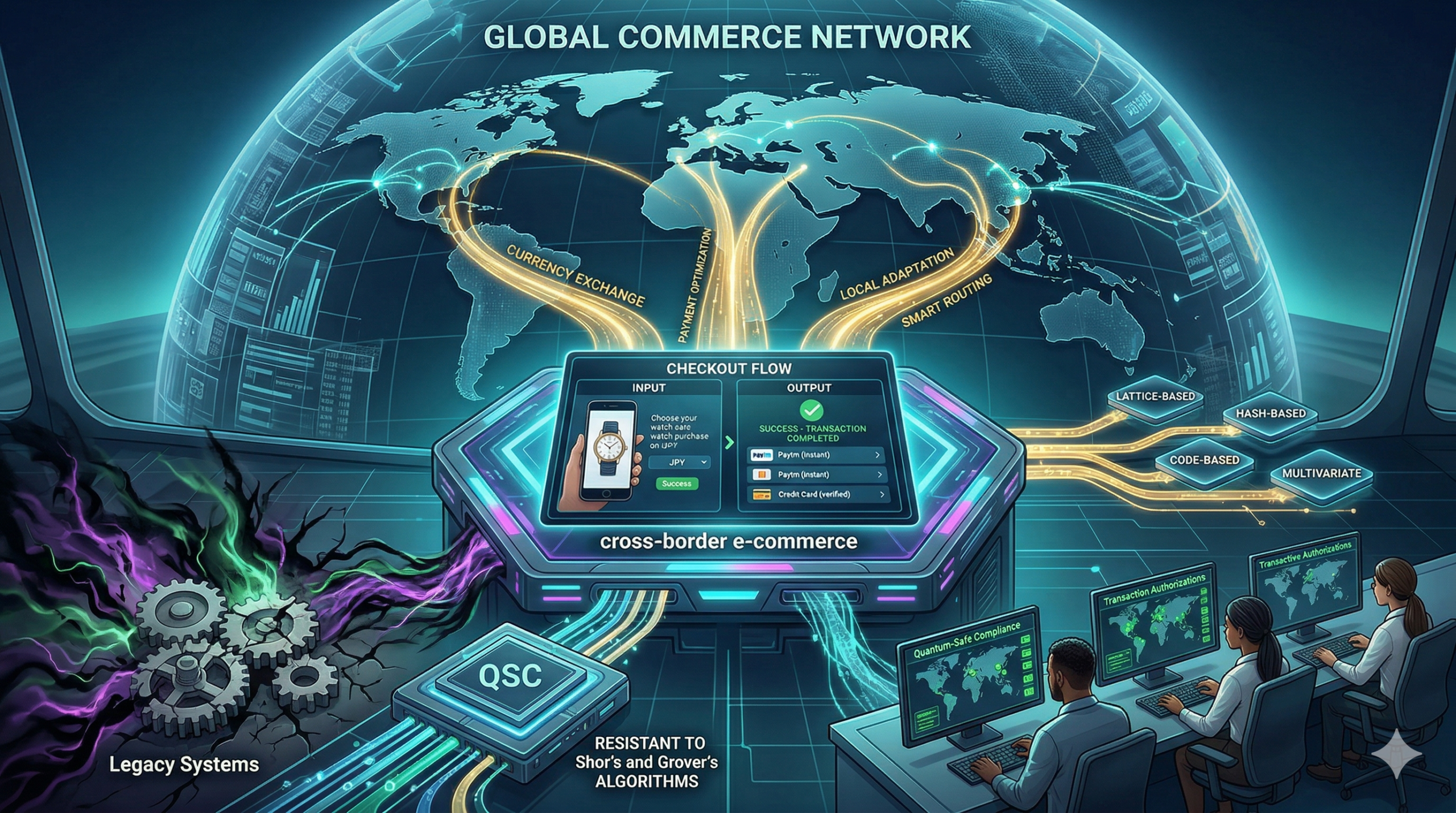

The rapid development of quantum computers creates a massive risk for global finance. Currently, most banks use encryption like RSA, which relies on math that is too hard for normal computers to solve. However, a quantum machine can crack these codes in just minutes. This is why we must adopt quantum-safe cryptography to protect payment security before these machines become common. Because the entire digital economy relies on trust, a single breach could cause a global collapse. Therefore, the race to secure our financial data is already moving at full speed.

The Rising Threat to Digital Money

A quantum computer does not work like a laptop. It uses qubits, which allow it to try millions of paths at the exact same time. This speed means that hackers could soon bypass the walls that keep our money safe. If we do not upgrade our systems, payment security will become a thing of the past. The threat is not just in the future; it is happening now through “harvesting” attacks.

Criminals are currently stealing locked data with the plan to open it later. They know that once they have a quantum machine, they can unlock years of old bank records. Consequently, we cannot wait for the technology to arrive. We must strengthen payment security today to prevent these future leaks. This proactive shift is the only way to maintain long-term consumer confidence.

What is Quantum-Safe Technology?

Quantum-safe math is designed to be so complex that even a quantum brain cannot find the answer. It uses different geometric and algebraic structures that do not have “shortcuts” for quantum algorithms. By moving to these new methods, we ensure that payment security remains intact for decades to come.

There are three main types of math that experts are testing right now:

Lattice-based Math: This hides data in a massive, multi-dimensional grid of points.

Code-based Math: This uses the science of error-correction to scramble and lock sensitive files.

Hash-based Signatures: This creates a digital “fingerprint” that is almost impossible to replicate or forge.

Building a Resilient Financial Future

The move to new standards is a major task for the world’s banks. It requires a concept called “crypto-agility.” This allows a bank to update its code without needing to rebuild its entire software suite. When a system is agile, it can adopt new payment security tools as soon as they are ready. This flexibility is vital because the hackers will never stop looking for new ways to get in.

Furthermore, global groups like NIST are already picking the best math to use. Banks must follow these standards to ensure they can talk to each other safely. If one bank uses old math while another uses new math, the system breaks. Thus, unity in payment security is just as important as the technology itself. We must work together to build a wall that no computer can climb.

Conclusion

The future of our economy depends on how we handle the quantum threat. By focusing on payment security now, we can stop the “cryptographic apocalypse” before it starts. It is a slow and difficult journey, but it is necessary for a safe digital world. Companies that lead this change will be the ones that people trust with their money. Ultimately, payment security is the foundation upon which the next century of trade will be built.

Frequently Asked Questions

1. Is my bank account at risk right now?

No, powerful quantum computers do not exist yet. However, we need to upgrade now to stay safe in the future.

2. What does “Harvest Now, Decrypt Later” mean?

It means hackers steal your locked data today so they can open it in a few years with a quantum machine.

3. Will new security make my payments slower?

Some new math is slower, but experts are picking the fastest ones to keep your experience smooth.

4. Can a normal computer run quantum-safe security?

Yes, these new rules are designed to run on the phones and laptops we use today.

5. How does this affect global payment security standards?

It forces every bank to move to a new, shared language of math that quantum machines cannot understand.

Remember struggling with countless PINs and passwords? How about waiting for those annoying One-Time Passwords (OTPs) via SMS? For years, these methods have been our digital guards. They protected our money and kept our accounts safe. However, these systems have their flaws. They can be slow. They can be stolen through phishing. Plus, they add friction to every transaction. Now, a new era is dawning. Biometric payments are here. This technology uses unique body traits to confirm your identity. It offers a faster, safer, and much more seamless way to pay. This shift marks a major step forward. It moves us far beyond the limits of old-school passwords and OTPs.

What Are Biometric Payments?

Biometric payments use your unique biological or behavioral features. These features confirm who you are during a transaction. Instead of typing a code, you simply use a part of your body. This makes payments both personal and secure.

Common types of biometric authentication include:

Fingerprint Recognition: This is the most common form. You simply touch a sensor with your finger. Your unique fingerprint pattern confirms your identity.

Facial Recognition: Your smartphone or a payment terminal scans your face. It uses distinct features to verify who you are. Apple’s Face ID is a prime example.

Iris/Retina Scans: These methods scan the unique patterns in your eye. They offer a very high level of security.

Voice Recognition: Your unique voice pattern can also verify your identity. This is used in some payment systems.

Behavioral Biometrics: This newer method looks at how you type, swipe, or walk. It creates a “behavioral profile” to confirm you are truly you.

Each method relies on features that are nearly impossible to copy or guess. This makes biometric authentication very strong.

Solving the OTP Headache: Speed and Convenience

Think about the delays caused by OTPs. You might wait for the SMS. Sometimes it never arrives. This stops the transaction. Biometric payments solve this problem completely. They offer instant authentication. There is no need to wait for a code. Your fingerprint or face scan happens in milliseconds.

This speed greatly improves the user experience. It makes checkout processes faster. It cuts down on abandoned carts in online shopping. For physical stores, it means quicker lines. Also, for mobile payments, it offers unmatched ease. You tap, you scan, you pay. This simple action shows how biometric authentication makes transactions smooth. It moves us far beyond the friction of old methods.

Enhanced Security: Far Beyond Passwords

One of the biggest benefits of biometric payments is their superior security. Passwords can be weak. They can be forgotten. OTPs can be intercepted or phished. However, your fingerprint or face is much harder to steal or fake. Each biometric trait is unique to you.

Furthermore, many biometric systems use liveness detection. This means they check if the biometric input is from a live person. They can tell the difference between a real finger and a photo. This makes faking them very hard. Also, biometric data is usually encrypted and stored securely. It is not easily exposed like a password list. This strong security reduces fraud significantly. It gives users peace of mind. Therefore, biometric authentication offers a robust defense against modern cyber threats. It truly protects your financial data.

Challenges and the Road Ahead

Despite the clear benefits, biometric payments face some challenges.

Privacy Concerns: Some people worry about how their biometric data is stored and used. Clear rules and strong encryption are vital.

Accuracy: While highly accurate, no system is perfect. Extreme conditions (like a cut finger) can affect scans.

Cost of Implementation: Setting up biometric readers for all payment terminals can be expensive for businesses.

Standardization: Different systems may use different biometric types. A unified standard is still developing.

However, these challenges are being addressed. Technology is improving fast. Consumer trust is growing. As these systems become more common, biometric authentication will become the norm. It will make payments simpler and safer for everyone.

The Future is Touch and Face

The future of payments is clear. It moves towards simpler, more secure methods. Biometric payments lead this change. They offer a powerful upgrade from OTPs and passwords. Imagine a world where paying is as easy as a glance or a touch. This world is quickly becoming real. For consumers, it means unmatched convenience and peace of mind. For businesses, it means faster transactions and less fraud. So, get ready to embrace your unique identity. Your fingerprint, face, or voice is truly your next payment method.

Frequently Asked Questions (FAQs)

1. Are biometric payments more secure than OTPs?

Yes, generally. Biometrics are unique to you and harder to steal or fake than OTPs. Many systems also use “liveness detection” to prevent spoofing.

2. What happens if a biometric scan fails (e.g., wet finger)?

Most biometric payment systems have backup methods. These include PINs, passwords, or a temporary OTP. This ensures you can still complete your transaction.

3. Is my biometric data stored somewhere centrally?

Typically, your biometric data is encrypted and stored locally on your device (like your smartphone). It is not usually stored on a central server. This design protects your privacy.

4. Can my biometrics be stolen and used for fraud?

While no system is 100% foolproof, biometric data is very hard to steal and use. Modern systems use advanced encryption and liveness detection. This makes them much more secure than passwords.

5. What is “behavioral biometrics”?

Behavioral biometrics analyzes how you interact with devices. It looks at your unique typing rhythm, swipe patterns, or even how you hold your phone. This creates a unique profile to confirm your identity.

The world of payments is changing fast. Artificial Intelligence is the main reason for this big change. Old ways of checking for fraud and generic checkouts are now ending. Now, AI in payments starts a new era of safety and custom service. This shift helps both businesses and shoppers. AI does everything from protecting against smart cyber threats to making unique shopping trips. Clearly, AI in payments is not just a future idea. It is now a key part of financial systems everywhere. Therefore, all businesses must understand how AI changes payment rules. This action is crucial to stay secure and customer-focused. This technology is truly the future of smooth and safe transactions.

Smart Fraud Detection: AI Keeps Your Money Safe

AI in payments helps a lot with detecting and stopping fraud. This use is truly the most important one. Old fraud systems used simple rules. Fraudsters could easily beat these simple rules. Conversely, AI uses strong learning programs to check huge amounts of data in real-time. Thus, it finds small patterns, strange actions, and odd behaviors that people or old systems would miss. For instance, AI learns a customer’s normal spending. It checks their usual buying places and devices. Therefore, if a sale looks odd—like a big buy from a new device in a different country—the AI flags it fast.

This smart fraud detection limits false positives greatly. This means your normal sales are not blocked often. This fact makes the customer feel happier. At the same time, it lowers the money lost by businesses. Because AI in payments learns from every new payment, it always gets better at being accurate. It stays ahead of new ways to commit fraud. Thus, a strong, smart guard protects every payment you make. This builds great trust and security throughout the whole payment process.

Proactive Protection: Checking Risk in Real-time

AI in payments does more than find old fraud signs. It also manages risk assessment in real-time. This quick action lets businesses judge the danger of each sale as it happens. It makes instant choices that protect everyone. AI programs review hundreds of facts right away: the sale amount, where it came from, the device used, past actions, and even how quickly the data was typed.

This real-time intelligence lets payment systems give a quick risk score to every sale. High-risk sales might face extra checks or be denied. Low-risk sales, on the other hand, move forward with no trouble. This exact checking lowers false denials. False denials upset honest customers and lose money for the business. As a result, this system is very finely tuned. It approves most good sales quickly while stopping fraud. All this is possible thanks to the smart power of AI in payments.

Personalized Checkout: Making Customers Happy

AI helps with more than just fighting fraud. It greatly improves the customer’s journey through personalized checkout. AI looks at what a customer bought before. It checks what they looked at and what payment methods they like. Then, AI quickly changes the checkout process for that person. Consider a customer who visits an online store again. AI remembers their favorite card. It fills in their address. Furthermore, it even shows them payment choices (like Buy Now, Pay Later) that they used before.

This personalized checkout makes buying easier. It makes the process faster. Also, it increases the number of finished sales greatly. For businesses, this means fewer abandoned carts and much happier customers. Furthermore, AI can smartly suggest other items to buy during checkout. These suggestions are based on that person’s history. Consequently, this simple act raises the average order value. By making the payment process feel easy and made just for them, AI in payments builds loyalty and encourages repeat business.

AI is Key to Future Payments

AI in payments is now necessary; it is not just a nice feature but also handles smart fraud detection and checks risk in real-time. It also builds highly personalized checkout experiences. AI is silently powering all modern financial dealings. For businesses, this means strong protection, lower costs, and much better customer happiness. For shoppers, it means quicker, safer, and simpler ways to pay. Since online buying will keep growing, smart AI programs will remain vital. They will be the silent helper in every successful sale, driving new ideas and securing the future of payments.

Frequently Asked Questions (FAQs)

1. How does AI improve fraud detection over traditional methods?

AI uses machine learning to check huge amounts of data for small, changing patterns. Traditional systems often miss these patterns. AI learns from new fraud attempts, making it more successful.

2. What is “real-time risk assessment” in payments?

It is the AI’s ability to instantly check the risk of each sale. It uses facts like the device, location, and history. This process lets the system make quick choices like approval or denial.

3. Can AI truly personalize the checkout experience?

Yes. AI checks a customer’s history and preferences. Then, it quickly shows their preferred payment options. It also fills in details. This makes the checkout process much faster and easier.

4. Does AI in payments only benefit large corporations?

No. Payment systems and FinTech groups are making AI tools available for all businesses. This helps small and medium-sized businesses compete fairly.

5. What are the main benefits of using AI in payments for a business?

The biggest benefits are far fewer fraud losses, higher transaction approval rates, and a happier customer base due to a smoother checkout.

You worry about keeping customer payment data safe. This is a big job. You must choose the best tools. Two top tools are tokenization and encryption. They both help your payment security. However, they work in different ways. Furthermore, they are best for different parts of a transaction. We will look at both methods now and will find out which one works best for your overall payment security plan. We will also talk about how to use them together. This will give you the strongest payment security possible.

What is Tokenization?

Tokenization is a simple idea. It replaces sensitive data with a useless placeholder. This placeholder is called a token. For example, a customer’s credit card number is very sensitive. The tokenization process swaps this real number. It substitutes a random string of numbers and letters. The token has no value. It has no mathematical link to the original card number. Therefore, if a hacker steals the token, they get nothing. The real card number stays safe. It is kept in a separate, highly secure place. This place is known as a token vault. This method gives you better payment security.

This process works very fast. First, a customer gives you their card details. Then, your system sends the card data to the tokenization provider. The provider creates the token. It stores the real card number in its secure vault. Consequently, the provider sends the non-sensitive token back to you. So, you never store the actual card number. Instead, you only store and use the token. This significantly reduces your risk. This is a smart approach to payment security.

Tokenization’s Strong Role in Payment Security

Tokenization is a favorite tool for many businesses. It is popular because it greatly reduces a company’s liability. Consider this: a breach happens. Your system only holds tokens. Hackers cannot use the stolen tokens. They are just random characters. They do not contain the real financial data. The actual card number never left the token vault. This is a very strong defense for payment security.

In addition, tokenization makes compliance easier. The Payment Card Industry Data Security Standard is called PCI DSS. This rule set protects cardholder data. Storing real card numbers means you must secure your entire network. This is expensive and difficult. But, when you only store tokens, the scope of PCI DSS shrinks. Your compliance burden is much smaller. Consequently, tokenization is a smart business move. It is a vital layer for top-tier payment security. Therefore, many experts recommend it for long-term storage of payment data.

What is Encryption?

Encryption is a different way to protect data. It uses mathematics to scramble information. It turns readable data into unreadable nonsense. This nonsense is called ciphertext. An encryption key is necessary to scramble the data. Similarly, a decryption key is necessary to unscramble it. Without the correct key, the ciphertext is useless.

For example, you type in your card number on a shopping website. The encryption process starts at that moment. Your browser uses an algorithm and a key. It turns the card number into a secret code. The code travels safely over the internet. Then, the payment processor receives the code. They use the correct key to unlock it. Consequently, the data turns back into the original number. This is how encryption protects data in motion. It is a necessary part of your payment security. Because of this process, people can shop online safely.

Encryption’s Key Role in Payment Security

Encryption is the backbone of all secure online communication. It is critical for securing data in transit. Data is most vulnerable when it travels from one computer to another. This is where encryption shines. It is always needed when you send data over a public network. You see the little lock icon in your web browser. This icon shows that a connection uses encryption. It means the data is safe as it moves.

Moreover, encryption can protect many types of data. It works well with large amounts of data. It can secure whole documents or video files. This is a major difference from tokenization. Tokenization mostly works on small, structured pieces of data. These are items like a credit card number or a Social Security number. Encryption is more flexible. It is a wider tool for general data protection. It is a must-have for complete payment security. So, you must use it to protect data on your servers too. This includes the secure token vault itself.

Comparing Reversibility and Security

Tokenization and encryption differ most in how they reverse the process. Encryption is designed to be reversed. It uses a key. Anyone with the key can turn the ciphertext back into plain text. This is a strength and a weakness. It is a strength because data can be easily shared and used by authorized parties. It is a weakness because a stolen key means total data loss. A thief who steals the key can access all encrypted data. Therefore, good key management is essential for this type of payment security.

On the other hand, tokenization does not use a key to create the token. The token is a random value. There is no mathematical formula to reverse it. It only links back to the original data in the secure token vault. To “detokenize,” you must access that vault. Therefore, a stolen token is worthless on its own. It is a much safer option if a breach occurs outside the vault. This makes tokenization a very strong defense for payment security. Consequently, it removes the danger that comes with key management.

Different Use Cases for Payment Security

Tokenization and encryption also have different best-use scenarios. Encryption is a superior choice for data in transit. You must encrypt the card details as they leave the customer’s device. This protects the data immediately. It prevents eavesdropping during transmission. The data must be unlocked later for processing.

However, tokenization is the better solution for data at rest. Data at rest means stored data. Merchants often save card details for recurring billing or one-click checkouts. Storing the actual PAN is risky. Storing a token is much safer. The token is useless if the storage system is compromised. This is why tokenization is a crucial strategy. It reduces the amount of time that sensitive data is exposed. It keeps the real PAN away from your less secure systems. This is the main benefit for overall payment security. Also, you can still use the token to process a charge later.

The Compliance Advantage and PCI DSS

Compliance with rules is a big reason to choose tokenization. The PCI DSS is very strict. It requires many security controls if you store, process, or transmit card data. These controls cover things like firewalls, system configuration, and monitoring. This can be complex and expensive for many companies.

Tokenization simplifies this process greatly. When a card number is tokenized, the token is no longer considered sensitive data under most PCI rules. The token is harmless. So, your internal systems that handle only tokens fall outside the strictest parts of PCI DSS. This saves you time and money. It also lowers the risk of compliance failures. Therefore, tokenization is a compliance strategy as much as it is a security strategy. Encryption is still required for transmission and for the vault itself. But, tokenization reduces the total effort needed for payment security compliance.

Choosing the Best Method for Payment Security

You may ask, “Which method is truly better?” The answer is that both methods are necessary. They are not competing tools. They are two pieces of a stronger payment security puzzle. Using them both provides a layered defense. This layered approach is known as defense in depth.

For example, imagine a bank vault. Encryption is like the armored truck that moves the money. The truck keeps the cash safe while it is traveling. Tokenization is like putting the cash into a new, unmarked safe deposit box once it arrives. The box is then placed in a larger, very secure vault. Even if someone steals the key to the safe deposit box, the box is unmarked. They cannot link it back to the original money. Therefore, you need both the secure transport and the clever storage. Both tokenization and encryption work together to achieve the highest level of payment security. This ensures maximum protection against different types of threats.

How Tokenization and Encryption Work Together

First, the customer starts an online payment. Their browser encrypts the card number immediately. This protects the data during the transfer. This is the first step in robust payment security. Then, the encrypted data reaches the payment processor’s secure server. The server uses the decryption key. It turns the data back into the original PAN.

Next, the tokenization process begins. The payment processor’s system takes the PAN. It generates a random token. It stores the real PAN in its highly secured, highly encrypted token vault. The vault is protected by the strongest encryption standards available. Finally, the system sends the non-sensitive token back to the merchant. The merchant then uses this token for the current transaction and all future transactions. The merchant never sees the sensitive PAN again. This combined approach is the industry best practice for payment security. It safeguards data at every point.

Different Payment Scenarios and Best Practices

Different payment scenarios favor one method over the other. For a one-time, in-person payment using a physical terminal, encryption protects the data from the card swipe to the processor. Tokenization is not always needed here. However, for e-commerce, tokenization is extremely beneficial. It allows for safe storage of card data for later use. This makes checkout easier for returning customers. Consequently, it improves the customer experience.

Moreover, for mobile wallets like Apple Pay or Google Pay, tokenization is always the main defense. The customer’s device creates a unique token for each card. The merchant and payment network only see this device-specific token. The actual card number is never shared. This is called network tokenization. It is a very powerful way to achieve strong payment security. It proves that tokenization is the better solution for modern, recurrent payment methods. But, the communication between the mobile app and the network is always secured with encryption.

Future-Proofing Your Payment Security

The world of cyber threats changes constantly. New hacking techniques appear every day. Therefore, your payment security strategy must be flexible. Relying on only one method is a mistake. Encryption keys can be compromised. Token vaults can still be targeted. But, if a hacker manages to steal an encrypted token, they face two massive challenges. They must break the encryption. Then, they must also breach the separate token vault. This makes the job much harder for them.

In conclusion, you should use both tokenization and encryption. They are not competing. They are partners. Use encryption to secure the transmission of data. Use tokenization to remove the sensitive data from your own systems. This layered approach minimizes your risk. It lowers your compliance costs. It gives your customers confidence. This dual method is the most effective choice for comprehensive payment security today.

Frequently Asked Questions

What is the main advantage of tokenization over encryption?

The main advantage is that a stolen token is worthless. It has no link to the original card number. It cannot be mathematically reversed by a hacker. This is safer than encrypted data if the key is stolen.

2. Does tokenization help me avoid PCI DSS compliance completely?

No, it does not let you avoid compliance entirely. It significantly reduces the scope of your compliance. You still need to secure your systems. You must protect the environment that handles the tokens.

3. Is data protected by SSL/TLS considered tokenized?

No, data protected by SSL/TLS is only encrypted. SSL/TLS is a form of encryption. It protects data in transit. It does not replace the data with a token.

4. Can I use only encryption to meet all payment security needs?

You can use only encryption. But, this leaves you with a large PCI DSS scope. It requires you to store and manage decryption keys. Most businesses use tokenization to reduce this risk.

5. What kind of data should I tokenize?

You should tokenize sensitive, structured data. This includes credit card numbers. It also includes bank account numbers. It helps protect other identifying numbers too. This helps improve payment security for all customers.

Online payment security is a critical concern in today’s interconnected world. The increase in online transactions today is primarily due to the convenience that digital payment methods offer.

With the rise of smartphones and e-commerce, customers are embracing the ease of completing transactions with just a few taps or clicks. Moreover, digital payments streamline the checkout process, eliminating the need for physical cash or card swipes.

Businesses are adapting to meet the growing demand for digital payment options, recognizing the importance of providing seamless and secure payment experiences to their customers. This demands an increased responsibility of ensuring the security and integrity of sensitive information. As cyber threats continue to evolve and grow in sophistication, implementing robust security measures is imperative to safeguarding online transactions and protecting both businesses and consumers. There are various security measures that businesses can adopt to secure online transactions and mitigate risks effectively.

Encryption-Safeguarding Data in Transit and at Rest: Encryption serves as the cornerstone of online payment security, protecting sensitive data from unauthorized access or interception by encrypting it into an unreadable format. Secure Socket Layer (SSL) and Transport Layer Security (TLS) protocols encrypt data transmitted between a user’s browser and the website’s server. This ensuring confidentiality and integrity during online transactions. Additionally, businesses should implement encryption techniques such as Advanced Encryption Standard (AES) to secure stored data in databases and servers in order to safeguard it from potential breaches or theft.

Multi-Factor Authentication (MFA)-Adding Layers of Verification: Multi-Factor Authentication (MFA) adds an extra layer of payment security to online transactions. MFA requires users to provide multiple forms of verification before accessing their accounts or completing a transaction. This typically involves a combination of something the user knows (password), something they have (a mobile device or token), and something they are (biometric data such as fingerprint or facial recognition). By implementing MFA, businesses can significantly reduce the risk of unauthorized access, identity theft, and account takeover, enhancing the security of online transactions.

Tokenization-Securing Payment Card Information: Tokenization replaces sensitive payment card information such as credit card numbers with unique tokens that have no intrinsic value and cannot be reverse-engineered to obtain the original data. When a customer initiates an online transaction, the payment card details are replaced with a token generated by the payment gateway, which is then used to process the payment securely. By adopting tokenization, businesses can minimize the risk of payment card fraud, protect customer data, and maintain compliance with Payment Card Industry Data Security Standard (PCI DSS) regulations.

Fraud Detection and Monitoring-Identifying Suspicious Activity: Implementing robust fraud detection and monitoring systems is crucial for identifying and mitigating fraudulent activities during online transactions. Machine learning algorithms analyze transaction patterns, user behavior, and other risk factors to detect anomalies and flag suspicious transactions in real-time. Additionally, businesses can utilize fraud prevention tools such as address verification systems (AVS), card verification value (CVV) checks, and geolocation tracking to verify the authenticity of transactions and prevent fraudulent activities before they occur.

Secure Payment Gateway-Partnering with Trusted Providers: Choosing a secure payment gateway is essential for ensuring the security of online transactions. Businesses should partner with reputable payment service providers that offer robust payment security features, compliance with industry standards, and a track record of reliability. Secure payment gateways encrypt sensitive data, facilitate secure communication between the merchant and the payment processor. They adhere to strict payment security protocols to protect against data breaches and unauthorized access. Businesses should regularly update their payment gateway software and configurations to patch vulnerabilities and mitigate emerging threats.

Customer Education and Awareness-Empowering Users to Stay Safe: Educating customers about online security best practices is essential for empowering them to protect themselves against cyber threats and fraud. Businesses should provide clear guidelines on creating strong passwords, recognizing phishing scams, and securing personal information. Additionally, businesses can offer resources such as payment security FAQs, tips for safe online shopping, and proactive alerts about potential security risks to help users stay informed and vigilant. By fostering a culture of security awareness, businesses can mitigate the risk of payment security breaches and build trust with their customers.

Regular Payment Security Audits and Compliance Checks-Ensuring Adherence to Standards: Conducting regular security audits and compliance checks is essential for evaluating the effectiveness of security measures and identifying potential vulnerabilities or gaps in online transaction security. Businesses should perform penetration testing, vulnerability assessments, and code reviews to identify and security weaknesses proactively. Additionally, businesses should ensure compliance with industry regulations such as PCI DSS, General Data Protection Regulation (GDPR), and California Consumer Privacy Act (CCPA) to protect customer data and avoid regulatory penalties.

As cyber threats continue to evolve, businesses must remain vigilant and proactive in adapting their payment security strategies protect the interests of all stakeholders involved in online transactions.