The global financial map is shifting as physical cash turns into digital code. Central Bank Digital Currencies are no longer a future dream but a present reality. Specifically, the race to build a digital currency is a high-stakes game of power. Nations are moving away from old systems to gain a strategic edge. Therefore, understanding the rise of CBDCs is vital for any global observer. This change will redefine how countries trade and interact for decades. You will see a clear shift in influence by following this deep and technical trend.

China’s Lead and the Digital Yuan Push

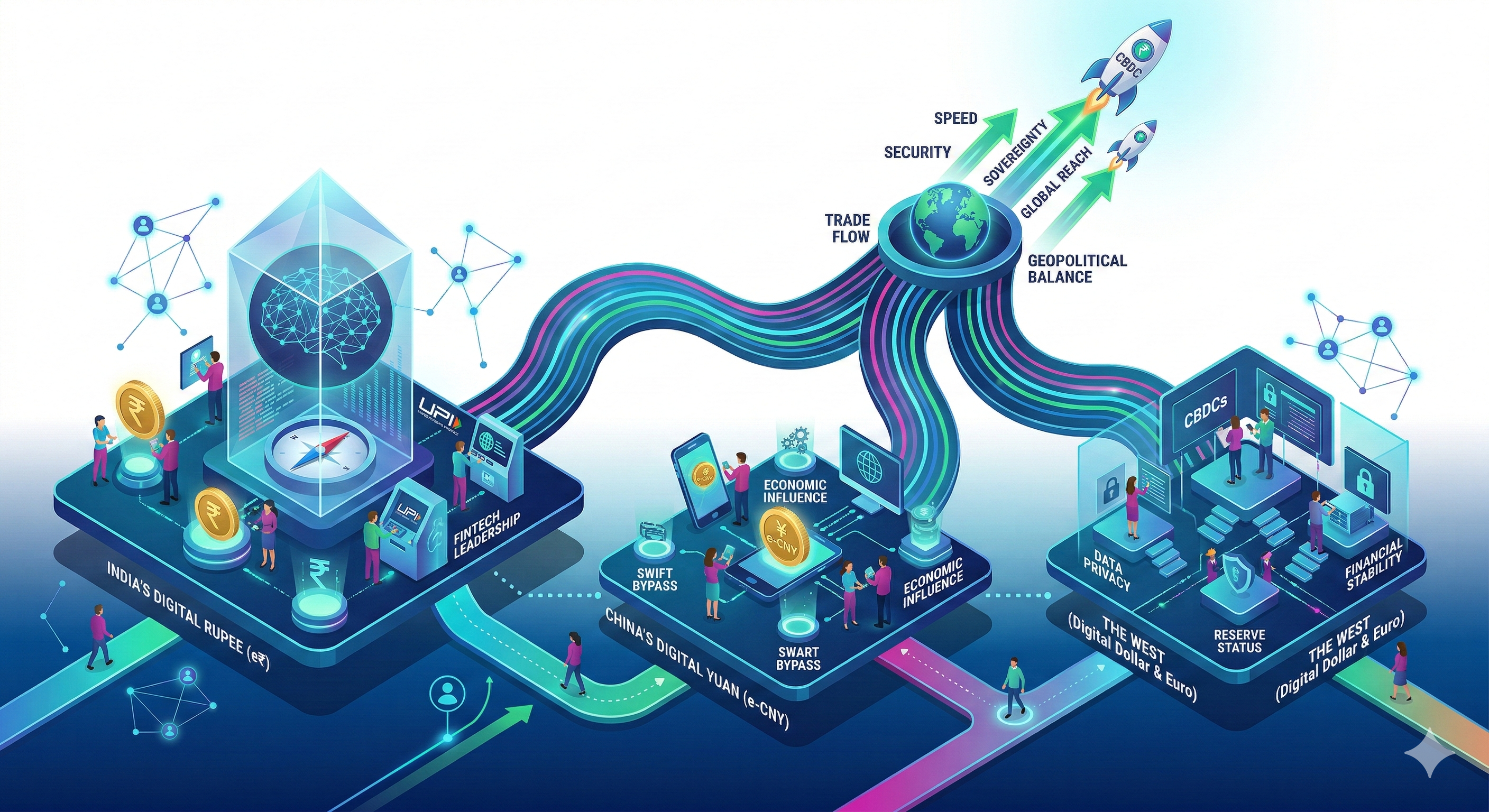

China is currently leading the race with its digital yuan, also known as the e-CNY. Specifically, the goal is to create a model for CBDCs that rivals the US dollar. By moving first, China can set the rules for how digital money flows across borders. Furthermore, this system allows them to bypass traditional Western banking networks like SWIFT. You might see a future where regional trade is settled entirely in digital yuan. This puts their economic growth on a very fast and independent path. Similarly, it acts as a tool of soft power to bring partners into their digital sphere.

India’s Digital Rupee and the UPI Success

India is taking a very smart and calculated path with its Digital Rupee. Building on the massive success of UPI, India seeks a strategy for CBDCs that balances innovation with safety. The Digital Rupee aims to reduce the high cost of printing and managing physical cash. Specifically, it offers a secure way for millions to join the formal economy instantly. Furthermore, India’s tech strength ensures that their system is both scalable and highly efficient. You should know that this move strengthens India’s spot as a global fintech leader. It ensures that the nation stays sovereign in a world of digital assets.

The West and the Struggle for the Digital Dollar

The West, led by the US and the Eurozone, is moving with more caution. There is a deep worry about how a shift toward CBDCs might affect privacy and bank stability. However, the risk of doing nothing is far too high for these major powers. If the US dollar loses its digital edge, it could lose its status as the world’s reserve currency. Therefore, the Federal Reserve and the ECB are testing systems that protect user data while staying fast. Specifically, they want a digital dollar that remains the gold standard for global trade. This journey is key to maintaining Western influence in the coming years.

The Impact on Global Trade and Sanctions

The rise of digital money changes how nations use economic pressure. In the past, blocking a country from global banks was a final and heavy blow. Now, a multi-polar world of CBDCs makes those blocks less effective. If two nations use a shared digital ledger, a third party cannot easily stop the flow. Furthermore, this leads to faster and cheaper cross-border payments for everyone. You will find that these tools reduce the friction of old money rules. Consequently, it sparks a new era of trade where speed is the ultimate advantage. This shift turns digital code into a real shield against foreign pressure.

FAQs

1 What exactly is a CBDC?

It is a digital form of a country’s national currency, issued and backed by the central bank.

2 How does it differ from Bitcoin?

Specifically, CBDCs are centralized and stable, while Bitcoin is private and its value changes often.

3 Can these digital coins replace the US dollar?

Indeed, if enough nations use different CBDCs for trade, the dollar’s global power could shrink.

4 Is my privacy safe with a digital rupee?

Central banks are building CBDCs that aim to balance your privacy with the need to stop financial crime.

5 Why is the race for these tools so fast?

Nations want to reduce their reliance on foreign systems and lead the future of global finance.

Have you ever thought your wallet could be a secret tool for world power? Today, a silent war is growing right inside your phone. Every time you tap to pay, you join a massive global game. AI in payments is not just a way to buy coffee anymore. In fact, it is now a top weapon for the world’s most powerful lands. This shift is fast and it is changing the maps we know.

Specifically, smart tech is redrawing the lines of who leads and who follows. This new era brings huge prizes but also very deep risks. Consequently, seeing the truth behind your screen is vital for your future. This is more than a simple trade. It is a race for total global control.

The Rise of Digital Dominance

The fast growth of AI has changed how we pay for goods. Once, paper cash ruled the world. Then, plastic cards took over the lead. Now, smart programs predict how you spend. They secure your funds and create new ways to trade. Consider the vast digital webs in the East. Or, look at the push for fast pay in the West. Each system uses deep AI to gain an edge. This power reaches far past simple finance. It touches your data and your safety. Indeed, this deep link makes smart tech a key spot for global lead. It shapes who controls the flow of wealth and facts.

Data: The New Gold Rush

Every tap or swipe on a phone creates new data. AI thrives on this data to learn fast. It spots fraud and makes your life easier. However, this wealth of facts also creates a huge weak spot. Who owns all this data? Where do firms store it? How do they use it for gain? These questions spark big fights between nations today. For example, some lands want data kept inside their borders. Others want to see it for safety reasons. Therefore, control over pay data means control over the economy. This makes the facts found by AI a top target for rivals.

Cybersecurity: The Invisible Front Line

As tech grows, so do the big risks. Strong AI systems are built to stop theft. Yet, bad actors use the same tech to break in. This leads to a fast race in the digital world. A major hit on a pay system could break a whole nation. Therefore, lands invest a lot in AI to guard their funds. This is not just about saving coins. Furthermore, it is about keeping trust in the whole web. The power to guard or stop pay flows is a big lever. It changes how lands talk to each other.

Digital Currencies: A Quest for Power

The rise of new digital coins makes the scene more complex. Nations like China work fast on their own digital yuan. They want to challenge the old rule of the dollar. These new coins use AI to move fast and cost less. However, they also raise fears about your privacy. If a land controls a popular coin, they gain a big lead. Consequently, the race to build these coins is a direct play for power. It changes the very shape of global wealth.

Standard-Setting: Who Writes the Rules?

Some rules act as a form of soft power. In the world of smart pay, the fight to set rules is very fierce. Nations and blocs race to set the norms for safety. If one land’s rules become the global bar, they win big. It makes trade easy for them and boosts their firms. Therefore, pushing for specific tech rules is a quiet type of war. It is a key part of modern world politics.

The Future: Working Together or Apart?

The path ahead for smart pay is not yet clear. Will lands work together to build a safe web? Or will rivals build their own split networks? Some ask for open rules to help everyone win. Others care more about their own safety and lead. This leads to split systems that do not talk to each other. Ultimately, the choices made today will shape our future world. This field is not just about tech. It is about the very heart of our shared world.

FAQs

1 What is the main idea of this battle?

It means that how AI moves money now affects who leads the world. Nations fight for the best tech.

2How does data change things?

Every buy creates facts. Who holds these facts knows more about the world than anyone else.

3Why is safety such a big deal?

If a pay web breaks, a whole land can fail. AI helps guard the web from bad hits.

4What are CBDCs?

They are digital forms of a land’s money. They use AI to change how we trade with each other.

5Who makes the global rules?

Big blocs and nations race to set the bars. The winner gets a huge edge in global trade.

In the rapidly evolving world of global finance, traditional banking routes are facing significant challenges. For instance, the trade relationship between Russia and China has undergone a massive transformation recently. As a result, both nations are exploring digital assets to maintain their economic ties today. Specifically, stablecoins have emerged as a powerful tool for a sanctions workaround. This shift is not just a trend but a strategic move to ensure trade continuity. Understanding how this system works is essential for anyone following global economic shifts. Russia–China trade in digital assets: stablecoins as a sanctions workaround is a vital topic now.

The Rise of Digital Assets in Cross-Border Trade

Sanctions have largely cut off traditional financial channels between these two major economies lately. Consequently, businesses have turned to alternative methods to settle payments quickly. Digital assets, particularly stablecoins, provide a seamless way to move value across borders. Because these assets are not tied to the Western banking system, they offer independence. Furthermore, the speed of transactions is much faster than conventional wire transfers. This efficiency is vital for maintaining the flow of goods and services. As a result, digital assets are now a cornerstone of modern trade. Russia–China trade in digital assets: stablecoins as a sanctions workaround keeps the economy moving.

Why Stablecoins Are the Preferred Workaround

Stablecoins are unique because they are pegged to a stable asset like gold. Therefore, they do not suffer from the extreme volatility of other coins. This stability makes them ideal for large commercial transactions. For example, a Russian exporter can receive payment in a dollar-pegged stablecoin. Similarly, Chinese importers can settle debts quickly using these digital tokens. In fact, stablecoins act as a bridge that bypasses the SWIFT system. This allows trade to continue even under the strictest financial restrictions. Russia–China trade in digital assets: stablecoins as a sanctions workaround provides needed financial safety.

The Role of Central Bank Digital Currencies (CBDCs)

In addition to private stablecoins, both nations are developing their own digital currencies. Russia is testing the digital ruble while China is expanding the digital yuan. These state-controlled assets aim to provide a regulated alternative for settlements. By using CBDCs, both countries can ensure that their financial data remains private. Moreover, these digital currencies can be directly exchanged between central banks. This eliminates the need for intermediary banks located in third countries. Consequently, the reliance on the US dollar is further reduced. Russia–China trade in digital assets: stablecoins as a sanctions workaround is a long-term goal.

Navigating the Legal and Regulatory Landscape

The use of digital assets for trade is still a relatively new frontier. Thus, both countries are working to create clear legal frameworks for these activities. Russia has recently passed laws to allow the use of crypto for payments. In contrast, China maintains strict domestic bans but shows pragmatism in international trade. Therefore, businesses must navigate a complex web of regulations to stay compliant. However, the drive to maintain trade volume often outweighs the regulatory hurdles. As these laws mature, we can expect more structured trade corridors. Russia–China trade in digital assets: stablecoins as a sanctions workaround requires careful legal study.

Future Implications for Global Finance

The shift toward digital assets marks a significant turning point in global finance. Specifically, it demonstrates that nations can build parallel financial systems when needed. This decentralization reduces the power of traditional financial hubs. Consequently, other countries facing similar pressures may look to this model as a blueprint. The success of stablecoins as a sanctions workaround proves the resilience of blockchain. Furthermore, it highlights the growing importance of digital sovereignty. As more trade moves on-chain, the global landscape will become increasingly fragmented. Russia–China trade in digital assets: stablecoins as a sanctions workaround is just the beginning.

Economic Resilience Through Digital Innovation

Nations must adapt when they face exclusion from the global banking grid. For instance, Russia and China are proving that technology can bridge the gap. Digital assets offer a way to keep supply chains active and stable. Moreover, this innovation helps small businesses engage in international trade without fear. Because the blockchain is transparent, it also helps in tracking large shipments. Therefore, the adoption of these tools is a sign of economic resilience. It is a bold move toward a multipolar financial world. Russia–China trade in digital assets: stablecoins as a sanctions workaround shows how tech solves problems.

Reducing Dependency on Western Financial Tools

For a long time, the global economy relied heavily on Western systems. However, this dependency is now viewed as a risk by some nations. Using stablecoins allows for a shift away from traditional currency traps. This means that trade can occur without the need for dollar conversion. Similarly, it protects local currencies from external shocks and sudden policy changes. This movement is gaining momentum across the Asian continent. Therefore, we may see more countries joining this digital trade alliance. Russia–China trade in digital assets: stablecoins as a sanctions workaround is a major part of this shift.

Security and Privacy in Digital Trade

Security is a top priority for any business conducting cross-border deals. Fortunately, blockchain technology provides a high level of encryption for every transaction. This ensures that the payment data is safe from hackers and prying eyes. Furthermore, the decentralized nature of these assets means there is no single point of failure. This makes the entire trade network more robust and reliable. Consequently, more companies are feeling confident about using digital tokens. It is a safer way to conduct business in a volatile world. Russia–China trade in digital assets: stablecoins as a sanctions workaround ensures secure transfers.

The Strategic Importance of Stablecoin Liquidity

Liquidity is essential for any currency used in international trade today. Because stablecoins are widely available, they provide the necessary liquidity for big deals. This means that businesses can convert their tokens back into local cash easily. Moreover, the presence of various stablecoins gives traders more choices and flexibility. This competition keeps transaction costs low for everyone involved. Therefore, the growth of the stablecoin market is a win for global trade. It provides the fuel needed for the digital economy to run. Russia–China trade in digital assets: stablecoins as a sanctions workaround relies on this liquidity.

FAQs

1 Why are stablecoins used for trade instead of Bitcoin?

Stablecoins offer price stability which is essential for business contracts. Consequently, they do not have the high risk of price changes.

2 Are these digital transactions legal in both countries?

Russia has legalized digital assets for international trade specifically to bypass sanctions. Similarly, China allows their use for cross-border settlements despite domestic bans.

3 How do stablecoins bypass traditional sanctions?

They operate on independent blockchain networks rather than the SWIFT system. Therefore, they do not need approval from Western banks to function.

4 What is the role of the digital yuan in this trade?

The digital yuan allows for direct state-to-state payments without using dollars. Thus, it strengthens the financial bond between the two nations.

5 Can small businesses use this method for trade?

Yes, digital assets are accessible to businesses of all sizes. Moreover, they offer a faster and cheaper way to move money globally.

Financial fragmentation now describes a world where the global economy splits into distinct regional or political blocs. This shift occurs because nations seek more control over their own money and security in a multipolar landscape. Therefore, you must understand how these changes will impact your business and your daily transactions. This guide explains the core challenges and the future of global payments.

The Rise of the Multipolar Economy

For many years, the world relied on a single financial system led by a few major powers. However, this centralized approach now faces competition from emerging economies and regional alliances. This shift creates a multipolar world where power is shared between several different global centers. Consequently, the standard rules for international finance are changing very quickly to match this new reality.

The move toward fragmentation happens because nations want to protect themselves from external financial pressure. For instance, some countries now build their own payment networks to avoid reliance on global systems like SWIFT. Because of this, we see a growing gap between different financial jurisdictions. I have noticed that this trend makes global trade much more complex for every person involved.

How Financial Fragmentation Impacts Global Payments

Fragmentation creates many small islands of finance instead of one connected global ocean. This separation means that moving money between two different blocs becomes much more difficult and expensive. For example, a business in one region might find that its payment software does not work in another region. Therefore, you must prepare for a future where global connectivity is no longer guaranteed.

You can expect to see higher fees for international transfers as systems become less compatible. Traditional cross-border payments already take a long time and require many middlemen. However, fragmentation adds even more layers of bureaucracy and compliance to every single transaction. In addition, businesses must now manage the risk of multiple currencies and varying local regulations.

The Role of Central Bank Digital Currencies

Many nations now explore Central Bank Digital Currencies (CBDCs) to modernize their local payment systems. These digital assets allow governments to track transactions more efficiently while reducing the cost of printing money. Furthermore, CBDCs can help a country settle international trades directly without using a global reserve currency. This technology is a primary tool for nations seeking financial independence in a multipolar world.

You should watch how these digital currencies interact with existing private payment networks. If two countries use different CBDC standards, they may still find it hard to trade with each other. Because of this, international organizations are working to create new rules for digital compatibility. However, the political friction of a multipolar world often makes these agreements very hard to reach.

Implications for Digital Payment Apps

Your favorite digital payment apps must now adapt to a landscape where cross-border rules change constantly. Some apps might choose to partner with local providers in every region to stay functional. Alternatively, others may focus only on one specific bloc to reduce their legal and technical risks. This fragmentation reduces the convenience that users have enjoyed for the last two decades.

In addition, users may need to carry multiple digital wallets to pay for goods in different countries. This shift reverses the trend toward a unified global marketplace where one app works everywhere. Therefore, you should look for payment solutions that offer wide compatibility and low conversion fees. Staying flexible will be your best strategy as the global system continues to split apart.

Risks to Global Financial Stability

Fragmentation creates a significant risk that the world will lose the ability to coordinate during a crisis. If every country follows its own rules, it becomes harder to stop a financial problem from spreading. For instance, a bank failure in one bloc might not be visible to regulators in another bloc. This lack of transparency makes the entire global economy much more vulnerable to sudden shocks.

Furthermore, the competition between different payment systems can lead to a “race to the bottom” in safety standards. Countries might lower their regulations to attract more business to their specific financial center. This behavior puts the security of your money at risk over the long term. Consequently, international cooperation remains vital even as political tensions continue to rise between nations.

The Future of Trade and Investment

Global trade will likely move toward “friend-shoring” where countries only trade with their political allies. This trend ensures that supply chains remain safe from geopolitical disruptions in distant regions. However, it also means that you may have fewer choices and higher prices for the goods you buy. Investment flows will also follow these political lines, creating two or more distinct economic zones.

You must rethink your investment strategy to account for these regional financial boundaries. For example, holding assets in only one bloc might leave you exposed if that region faces a downturn. Diversifying across different payment systems and jurisdictions is now a requirement for protecting your wealth. Therefore, staying informed about global shifts is the most important step you can take today.

Technical Standards and Interoperability

The primary technical challenge in a fragmented world is making sure different systems can still talk to each other. This is often called interoperability, and it is the key to keeping the global economy functional. If a payment message in Asia cannot be read by a bank in Europe, trade will stop. Engineers are now building bridges between different blockchain and digital currency protocols.

However, the political will to use these bridges is often lacking in a multipolar world. Some nations prefer “walled gardens” because they provide more control over their domestic data. Specifically, you should follow the development of international standards like ISO 20022. These common languages are the only things preventing a total breakdown of global financial communication.

Protecting Your Business From Financial Fragmentation

If you run a business that trades globally, you must audit your payment providers immediately. You should ensure that your primary bank has strong relationships in the regions where you operate. In addition, you may want to explore using stablecoins or other digital assets for fast cross-border settlements. These tools can bypass some of the friction caused by political fragmentation.

Gathering a diverse set of payment tools is the smartest way to manage these growing risks. If one system goes offline or becomes too expensive, you need an alternative ready to go. Take the time to understand the local payment habits of your international customers. Once you have a flexible system, you can grow your business despite the challenges of a multipolar world.

Conclusion and Next Steps

Financial fragmentation is a complex trend that will shape the next few decades of our lives. By focusing on the causes and the technical solutions, you can navigate this landscape successfully. The journey toward a more regional world requires patience and a high degree of adaptability from everyone.

If you want to stay ahead, you must monitor the news about CBDCs and regional trade blocs. Start by reviewing your current international payment methods to see where you are most vulnerable. Then look for new technologies that can bridge the gap between different financial zones. Your proactive approach will ensure that you remain connected to the global economy.

FAQs

1 What is financial fragmentation?

Financial fragmentation is the process where the global financial system splits into separate regional or political zones.

2 How does a multipolar world affect my payments?

It makes sending money across borders more expensive and complex as different regions use incompatible systems.

3 What are CBDCs?

Central Bank Digital Currencies are digital versions of a nation’s official currency issued and managed by the central bank.

4 Can AI help with financial fragmentation?

Yes, AI can help businesses manage the complex rules and multiple currencies found in a fragmented world.

5 What is interoperability in finance?

It is the ability of different financial systems and software to communicate and process transactions with each other.

The world of money is changing very fast as we move into 2026. Therefore, many countries are now testing their own digital versions of cash. Truly, Central Bank Digital Currencies, or CBDC, are becoming a reality for millions of users. Consequently, everyone in the payment world is asking if this is a threat or a giant opportunity.

Some people feel that a search engine will soon show a world without private payment processors. But, the truth is much more complex and interesting for business owners. Always remember, every major shift in finance creates new ways to provide value. This ensures that those who adapt will find more success than those who stay the same. This approach requires a deep look at how digital money moves across borders. It helps you prepare for a future where cash might disappear entirely. It makes your financial strategy much more robust for the years ahead.

Phase 1: What Exactly Are CBDCs and How Do They Work?

First, let us look at what makes a CBDC different from the digital money we use today. Why are governments so interested in this new technology right now? Clearly, it is about giving the central bank more control and transparency over the money supply. Therefore, it is a direct digital claim on the central bank rather than a private bank.

Key Features of a Digital Currency

Here are several things that define a CBDC in the current market:

Direct Issuance: The money comes directly from the government or central bank.

Instant Settlement: Transactions happen in real time without waiting for clearing.

Low Costs: It aims to remove many of the fees found in traditional banking.

Programmability: This allows for smart contracts that trigger payments automatically.

Universal Access: It helps people without bank accounts join the digital economy.

Enhanced Security: Each digital unit is tracked to prevent fraud and theft.

Legal Tender: It must be accepted by law for all debts and taxes.

Truly, this technology could change how every search engine tracks financial data. But, it also brings up big questions about user privacy and data safety. This keeps the debate between speed and privacy very active in 2026.

Phase 2: Why Gateways Might See CBDCs as a Threat

So, why are some payment gateways feeling nervous about these digital coins? Truly, a government-backed system could bypass the need for many private middlemen. Consequently, the traditional fees that gateways charge might be at risk. It acts as a direct competitor to the services that have existed for decades.

Risks Facing Traditional Payment Gateways

Here is how CBDCs could challenge the existing payment model:

Fee Compression: If government digital money is free to use, gateways cannot charge high fees.

Direct Wallets: Users might pay merchants directly from a government app.

Faster Rails: Central banks might build their own fast networks that skip private ones.

Reduced Volume: Traditional credit card use might drop as people switch to CBDCs.

Data Control: Governments might keep the transaction data that gateways used to own.

Strict Rules: New laws might favor the state system over private companies.

Global Shifts: International CBDC links could make cross-border gateways less vital.

Furthermore, this could hurt the search engine ranking of companies that rely on old tech. It makes it harder for slow-moving businesses to stay profitable. This ensures that only the most efficient gateways will survive the next five years. It creates a very competitive environment for everyone in the finance space.

Phase 3: The Massive Opportunity for Smart Gateways

The third phase looks at why CBDCs might actually be a good thing for the industry. Clearly, new technology always creates new needs for the average user. Therefore, smart gateways can act as the vital bridge between the state and the people.

How Gateways Can Thrive with Digital Currency

Firstly, gateways can provide a better user experience. Government apps are often very simple and hard to use for complex tasks. Secondly, they can offer advanced fraud protection. While CBDCs are secure, hackers will always try to find new ways to steal.

Furthermore, gateways can manage the mix of different currencies. Most people will still use credit cards, crypto, and CBDCs at the same time. Also, they can provide better reporting for merchants. Business owners need deep data that a basic government wallet might not show. Lastly, they can help with international trade. Linking different national CBDCs together is a task that gateways are perfect for. Truly, your search engine authority grows when you offer solutions to these new problems. It allows you to become a trusted advisor in a confusing digital landscape. This is the key to winning in the new financial era.

Phase 4: Preparing for the 2026 Financial Shift

The fourth phase is about the steps you must take to be ready for this change. Clearly, you cannot wait for the rules to be fully written before you act. Therefore, you should start integrating digital currency options into your systems now.

Steps to Future-Proof Your Payment Strategy

Firstly, monitor the pilot programs in major countries. Watching how China or Europe handles their digital coins gives you a head start. Secondly, invest in blockchain and ledger technology. These are the foundations that most CBDCs are built upon.

Furthermore, talk to your customers about their needs. See if they are interested in using digital versions of their national currency. Also, stay active in the regulatory discussion. Helping shape the laws can protect your business from bad rules later. Lastly, improve your site speed and mobile features. A fast site helps your search engine ranking and makes digital payments smoother. Truly, being an early adopter is the best way to secure your future. It shows the world that your brand is a pioneer in the digital space. This leads to more trust and higher traffic over the long term.

Best Practices: Balancing Innovation and Safety

Managing digital money requires a very careful and balanced approach. It needs a focus on both new features and old-fashioned security. Clearly, the trust of your users is the most valuable asset you have. Therefore, follow these simple habits to maintain your lead in 2026.

Strategies for Long-Term Digital Currency Success

Firstly, always prioritize the privacy of your users. Even with a state-backed coin, people want to know their data is safe with you. Secondly, keep your systems simple and easy to understand. New financial tools can be very scary for the average person.

Furthermore, update your content frequently. Use your blog to explain how these changes help your customers save money. Also, build partnerships with banks and tech firms. No company can handle the shift to CBDCs entirely on its own. Lastly, track your search engine performance closely. Make sure people can find your guides when they search for digital money help. Truly, a helpful and modern gateway will always be in high demand. It turns a potential threat into a powerful tool for growth. This ensures your brand stays strong regardless of what the central banks do.

Frequently Asked Questions (FAQs)

Q1: Is a CBDC the same as Bitcoin?

No, Bitcoin is a private crypto currency that is not backed by any state. A CBDC is a digital version of a country’s official money and is controlled by the government.

Q2: Will CBDCs help my search engine ranking?

Writing about CBDCs can help your ranking if you provide expert info that users are searching for. It shows you are an authority on the latest financial trends.

Q3: When will CBDCs become common for everyone?

Many countries are already in the pilot phase in 2025. It is likely that CBDCs will be a common payment option in major markets by the end of 2026.

Q4: Can I use a CBDC for international payments?

Yes, one of the main goals of CBDCs is to make international payments faster and cheaper. Gateways will play a major role in linking these different systems.

Q5: Will my private bank account disappear?

No, CBDCs are expected to work alongside traditional bank accounts. Most experts believe we will continue to use a mix of both systems for a long time.