Most online stores lose customers at the final step because traditional checkout pages are often slow and boring. Now, generative ai is changing that forever by creating a personal path for every shopper. Because this technology learns what you like and how you want to pay, buying things online is faster than ever. Furthermore, smart stores use generative ai to turn one-time shoppers into loyal fans. This shift is vital for any brand that wants to grow. Consequently, the payment journey is no longer just a task; it is an experience.

Why Old Checkout Systems Fail

Static forms are the biggest enemy of sales because most shops show the same fields to everyone. Consequently, many people leave their carts empty. This is because the process feels long and hard. Generative ai solves this by making every page unique for the user. For instance, it knows if you are on a phone or a laptop. Furthermore, it predicts which payment method you prefer. Therefore, you spend less time typing and more time enjoying your purchase. In short, ai removes the friction that kills sales.

Real-Time Help with Generative AI

Shopping can sometimes feel confusing, especially when you have questions about shipping or taxes. Standard help pages are often hard to find. However, ai adds a smart assistant to the page to guide you. This bot answers your questions in seconds. Because the bot knows your cart, it gives perfect advice. This builds trust and keeps you moving forward. In addition, ai makes sure you never feel alone while shopping.

Moreover, these bots can offer special deals at the perfect moment. If you hesitate, the generative ai might give you a small discount to help you decide. As a result, shoppers feel valued and safe. Generative ai is not just a tool; it is a digital guide. Because of these benefits, top brands are moving to AI today. Therefore, the checkout flow becomes a conversation instead of a form.

Safer and Faster Payments

Security is the most important part of any sale because hackers are always looking for ways to steal data. Luckily, ai is great at spotting fraud by looking at millions of data points in real-time. If it sees something odd, it stops the threat fast. This keeps your money and data very safe. Because the ai is so smart, it rarely blocks real customers. Thus, generative ai makes payment security much stronger for everyone.

Additionally, generative ai helps with filling out forms by guessing your address with high accuracy. This reduces errors and saves time for the customer. When you use generative ai, the checkout flow feels like magic. You just click and go. Therefore, the risk of a mistake is very low. This is the future of ai in the payment world. Finally, this technology ensures that safety does not come at the cost of speed.

The Big Future of Generative AI

We are only at the start of this change. Soon, every store will use ai to talk to us. It will know our size, our style, and our budget. This means we will see fewer ads we do not like. Instead, we get a tailored world of products. Generative ai makes every transaction feel human. It is the best way to shop in 2026. If you want to stay ahead, you must use generative ai now. In conclusion, the personalized payment journey is the new standard for global trade.

Frequently Asked Questions

1. Is generative ai safe for my credit card?

Yes, it improves security by spotting fraud much faster than older systems.

2. Does generative ai make my phone slow?

No, most of the work happens on fast servers, so your phone stays quick.

3. Why do stores need ai?

It helps them sell more by making the checkout process easy and personal for everyone.

4. Can generative ai help with returns?

Yes, it can guide you through the return process and answer policy questions instantly.

5. Will all stores use generative ai soon?

Yes, it is becoming the global standard for all top e-commerce websites.

In the high stakes world of global trade, money is now a silent weapon. Specifically, many nations now realize that controlling how funds move is a vital edge. Therefore, building a solid payment infrastructure has become a key tool of soft power. This shift changes how countries talk and trade with each other. It is not just about digital coins or bank apps. In fact, it is a smart way for a country to lead on the global stage. Consequently, a strong and stable payment infrastructure helps a nation project its true strength. You will see a clear shift in power by following this deep and strategic trend.

Winning the Trade War Without a Single Shot

Many people think trade wars are only about high taxes and ships. However, the real fight often happens in the wires and code of a bank. First, a local payment infrastructure can bypass old global rules that slow down growth. Specifically, it lets a country keep its trade moving even when others try to block it. Furthermore, having a top tool that others want to use creates a new kind of bond. You also gain a lead when your neighbors rely on your tech to buy bread. Similarly, a unified payment infrastructure ensures your trade stays safe during a crisis. This puts your growth on a steady path for a very long time.

Why Every Nation Wants Their Own Money Rules

The journey to the top begins when a nation builds its own money path. At this stage, relying on a foreign payment infrastructure is a very big risk. These new tools act as a top guide for a country’s financial future. Specifically, a custom payment infrastructure ensures that a nation and its true worth stay safe. It is built to spark fast progress in every single trade deal. You should also know that a smart system offers more than just a way to pay. While a simple app just sends cash, a whole payment infrastructure guides the whole economy. Furthermore, it moves firms past the fear of being cut off from the world.

The True Influence of Digital Dollar and Yuan

As a nation’s tech grows, its influence spreads to other places. At this stage, the focus on a payment infrastructure builds a very strong bond with allies. This plan is specific to what a partner country likes and needs. For example, some might get a faster way to sell their goods abroad. The timing of these moves is very key for global success. Furthermore, a top leader handles all the tech and rules with ease. This ensures your trade plan is solid from the very first step. Such smart timing helps a country move toward a big global win. Indeed, a modern payment infrastructure reveals who is truly in charge today.

Protecting the Flow of Goods and Services

Data is the backbone of all smart trade and money success today. The way a country handles its payment infrastructure tracks how every dollar moves. This includes how users buy and sell items in a safe way. These facts help refine the path for every brand and firm in the land. Therefore, the system learns and grows over time to serve the people better. This data driven path ensures the best results for a whole nation. It also prevents any bad risks from hurting the economy. A smart payment infrastructure relies on real facts to win every single time. Your plan and focus are too important to risk at any step.

Conclusion and the New Map of World Trade

The future of global trade is too important to leave in the hands of others. Today, we see how a modern payment infrastructure changes who wins and who loses. This smart move helps a nation scale faster and stay much safer too. It turns simple tech into a real win for a whole region. You will see more growth and less stress for firms everywhere. Therefore, nations act now to secure their spot in the global market. Knowing the truth of quality tech lead leads to true success. It is the best way to ensure a bright future for many years. You will find that the right payment infrastructure makes all the difference in a trade war.

FAQs

1 How is a payment system a tool of power?

It lets a country control how money flows, which can help or hurt other nations.

2 Does this affect small businesses?

Yes, it makes it easier or harder for them to sell items to other countries.

3 Why is it called soft power?

Because it uses tech and money to lead rather than using a real army.

4 Is it safe for a country to use its own system?

Specifically, it is much safer because it stops other nations from blocking their trade.

5 Will this trend grow in the future?

Indeed, more nations are building their own tools to stay independent and strong.

The world of money is changing very fast. Many nations want to build their own systems, free from old ways. However, the path to a new global order is complex and full of big choices. Because of this, staying ahead means looking toward fresh tech and strong partnerships. Specifically, BRICS and digital payments are now a key topic for leaders worldwide. This offers a clear map for new trade, faster work, and a very modern way to pay. This move is not just about tools for a few banks. In fact, it is a smart strategy for many lands to gain more power. Consequently, understanding this impact helps you see why it matters.

The Current Landscape: Visa and Mastercard’s Dominance

For a long time, two names have ruled how the world pays. Visa and Mastercard have built vast networks across the globe. They process billions of deals every single day with ease. These systems are reliable and trusted by many people everywhere. However, this power also means control rests in just a few hands. Some nations worry about this strong hold on their money flows. They feel that vital services should not be tied to just one or two firms. Furthermore, geopolitical events can sometimes affect these global payment channels. This makes some countries very eager to find new ways to pay. Therefore, the search for an independent path grows stronger.

The BRICS Alliance: A Push for Economic Independence

BRICS is a group of five big nations: Brazil, Russia, India, China, and South Africa. These countries represent a huge part of the world’s people and wealth. They often work together to boost their trade and influence. A key goal for BRICS is to create more economic freedom for its members. They want to reduce their reliance on systems built and run by other blocs. This desire extends to how money moves between them. The idea of a shared payment system is very appealing. It would help them trade more easily without outside interference. Consequently, BRICS and digital payments are a natural fit for their goals. This alliance seeks to build a new financial backbone.

The Rise of Digital Payments and Central Bank Digital Currencies (CBDCs)

Digital payments are quickly changing how we use money. Apps on phones, online wallets, and instant transfers are common now. This shift makes it easier to imagine new global systems. A big part of this trend is the rise of Central Bank Digital Currencies (CBDCs). Many BRICS nations, like China and India, are actively working on their own CBDCs. These are digital forms of a country’s money, issued by its central bank. If BRICS countries can link their CBDCs, it would create a powerful new network. This would allow fast, cheap, and direct payments between their economies. Such a system could bypass older networks entirely. Thus, BRICS and digital payments could form a new standard.

Challenges to Building a Unified BRICS Payment System

Creating a brand new global payment system is not easy. First, there are many technical hurdles to overcome. Each country has its own rules, tech, and banking laws. Making these all work together perfectly takes huge effort. Furthermore, building trust among member states is vital. They must agree on how data is shared and how disputes are handled. There are also security concerns; any new system must be very safe from cyber-attacks. Finally, getting people and businesses to adopt a new method takes time. They are used to the ease of Visa and Mastercard. Despite these challenges, the motivation for a BRICS digital payment alternative is very high.

Potential Impact: A New Global Financial Order?

If BRICS succeeds in creating its own payment system, the impact could be huge. It would give these nations more control over their own money flows. They could reduce fees and speed up cross-border trade. It might also encourage other developing countries to join or adopt the system. This could lead to a more diverse and multi-polar global financial world. Visa and Mastercard would still be very important. However, they would face a serious new competitor. This competition could even push existing systems to innovate more. Consequently, BRICS and digital payments could reshape how we think about international finance. The shift could truly impact global power dynamics.

Conclusion: The Road Ahead

The idea of an alternative to Visa and Mastercard from the BRICS bloc is gaining traction. The rise of digital payments and CBDCs makes this vision more possible than ever. While big challenges remain, the desire for economic independence is a strong driving force. This development is worth watching closely. It could signal a major shift in how global money moves and who controls it. The future of international payments might be far more diverse than it is today.

FAQs

1 What is BRICS?

It’s a group of major emerging economies: Brazil, Russia, India, China, South Africa.

2 Why do BRICS nations want a new payment system?

They want more economic independence and less reliance on existing global payment networks.

3 What are CBDCs?

Central Bank Digital Currencies are digital forms of a country’s national money, issued by its central bank.

4 Could a BRICS system replace Visa/Mastercard?

It might not replace them entirely but could emerge as a significant alternative, especially for cross-border transactions among BRICS and allied nations.

5 What are the biggest challenges?

Technical integration, regulatory harmonization, security, and user adoption across diverse nations.

Have you ever thought your wallet could be a secret tool for world power? Today, a silent war is growing right inside your phone. Every time you tap to pay, you join a massive global game. AI in payments is not just a way to buy coffee anymore. In fact, it is now a top weapon for the world’s most powerful lands. This shift is fast and it is changing the maps we know.

Specifically, smart tech is redrawing the lines of who leads and who follows. This new era brings huge prizes but also very deep risks. Consequently, seeing the truth behind your screen is vital for your future. This is more than a simple trade. It is a race for total global control.

The Rise of Digital Dominance

The fast growth of AI has changed how we pay for goods. Once, paper cash ruled the world. Then, plastic cards took over the lead. Now, smart programs predict how you spend. They secure your funds and create new ways to trade. Consider the vast digital webs in the East. Or, look at the push for fast pay in the West. Each system uses deep AI to gain an edge. This power reaches far past simple finance. It touches your data and your safety. Indeed, this deep link makes smart tech a key spot for global lead. It shapes who controls the flow of wealth and facts.

Data: The New Gold Rush

Every tap or swipe on a phone creates new data. AI thrives on this data to learn fast. It spots fraud and makes your life easier. However, this wealth of facts also creates a huge weak spot. Who owns all this data? Where do firms store it? How do they use it for gain? These questions spark big fights between nations today. For example, some lands want data kept inside their borders. Others want to see it for safety reasons. Therefore, control over pay data means control over the economy. This makes the facts found by AI a top target for rivals.

Cybersecurity: The Invisible Front Line

As tech grows, so do the big risks. Strong AI systems are built to stop theft. Yet, bad actors use the same tech to break in. This leads to a fast race in the digital world. A major hit on a pay system could break a whole nation. Therefore, lands invest a lot in AI to guard their funds. This is not just about saving coins. Furthermore, it is about keeping trust in the whole web. The power to guard or stop pay flows is a big lever. It changes how lands talk to each other.

Digital Currencies: A Quest for Power

The rise of new digital coins makes the scene more complex. Nations like China work fast on their own digital yuan. They want to challenge the old rule of the dollar. These new coins use AI to move fast and cost less. However, they also raise fears about your privacy. If a land controls a popular coin, they gain a big lead. Consequently, the race to build these coins is a direct play for power. It changes the very shape of global wealth.

Standard-Setting: Who Writes the Rules?

Some rules act as a form of soft power. In the world of smart pay, the fight to set rules is very fierce. Nations and blocs race to set the norms for safety. If one land’s rules become the global bar, they win big. It makes trade easy for them and boosts their firms. Therefore, pushing for specific tech rules is a quiet type of war. It is a key part of modern world politics.

The Future: Working Together or Apart?

The path ahead for smart pay is not yet clear. Will lands work together to build a safe web? Or will rivals build their own split networks? Some ask for open rules to help everyone win. Others care more about their own safety and lead. This leads to split systems that do not talk to each other. Ultimately, the choices made today will shape our future world. This field is not just about tech. It is about the very heart of our shared world.

FAQs

1 What is the main idea of this battle?

It means that how AI moves money now affects who leads the world. Nations fight for the best tech.

2How does data change things?

Every buy creates facts. Who holds these facts knows more about the world than anyone else.

3Why is safety such a big deal?

If a pay web breaks, a whole land can fail. AI helps guard the web from bad hits.

4What are CBDCs?

They are digital forms of a land’s money. They use AI to change how we trade with each other.

5Who makes the global rules?

Big blocs and nations race to set the bars. The winner gets a huge edge in global trade.

The modern world is witnessing a quiet but massive transition in how money moves across borders. For decades, global trade relied on a single, centralized network. However, the current era of geopolitical tension has made many nations feel unsafe. They have realized that their economic survival depends on having a payment system that they fully own and control. This move toward sovereignty is a defensive wall against global instability.

The Problem: The Hidden Risks of Financial Dependence

When a nation lacks its own infrastructure, its domestic economy is essentially on loan from a foreign entity. If a global provider decides to disconnect a country, every local payment could freeze, causing instant chaos. This isn’t just a technical glitch; it is a threat to a nation’s ability to govern itself.

Relying on a single external ledger creates a “choke point” for a country’s wealth. Statistics from the last twelve months show that nations without independent rails are 50% more likely to suffer from severe liquidity shocks. To solve this, governments are building systems that ensure a payment made within their borders never has to leave their territory to be verified. This local settlement provides a level of security that no private foreign firm can match.

The Solution: Building the New Digital Infrastructure

The construction of these national rails is often referred to as building the “public roads” of the digital age. A sovereign payment rail is designed to be a utility that serves every citizen, regardless of their income level. Unlike private networks that charge high fees for every transaction, these public systems focus on speed and low costs.

Specifically, by removing the middleman, a country can ensure that a payment hits a merchant’s account in seconds rather than days. This boost in remittance speed allows small businesses to reinvest their capital much faster. Furthermore, by using AI to monitor every payment, the state can prevent fraud and money laundering with extreme precision. This technical mastery ensures that the national exchange remains a trusted environment for everyone involved.

The Future: A World of Interlinked Sovereignty

Building a local rail does not mean cutting ties with the world. Instead, it allows a nation to engage in a global payment without being dependent on a single central power. We are moving toward a multi-polar financial world where different national systems talk to each other directly through digital bridges.

In this new landscape, a payment initiated in Asia can be settled in South America without passing through a third country’s bank. This creates a more resilient global economy that is less prone to collapse. As every nation secures its own payment future, the world becomes more balanced and fair. By investing in these independent rails today, a country ensures that every payment made by its citizens remains a tool for growth rather than a source of vulnerability.

FAQs

Q1: Why is a domestic payment system better than a global one?

Ans. It offers better security because it ensures your money stays moving even if global networks face political or technical issues.

Q2: How does this help the average shopper?

Ans. It usually leads to lower fees for stores, which can result in lower prices for the things you buy every day.

Q3: Is my data safer on a national payment rail?

Ans. Yes, because your data is protected by your own country’s laws rather than being sold by a foreign corporation.

Q4: Will I still be able to send money abroad?

Ans. Absolutely. Sovereign rails are being built to “bridge” together, making international money transfers faster and cheaper than ever.

Q5: When will these new systems be ready?

Ans. Many countries like India, Brazil, and China already have them, and dozens more are launching theirs by the end of 2026.

I’ve heard it a thousand times. A nation relies only on one foreign credit card firm. And yet, their local shops pay high fees. Usually, that is just a polite way of saying the country has lost its own power. Also, old bank moves take a long time. They involve too many middle men. If you build a new market on old tracks, you are building a ghost town.

In fact, a system where local tracks handle 80% of deals is worth much more. Furthermore, the biggest cost in 2026 is the lack of links between close nations. This happens when people must carry cash or pay high fees. This path creates a big gap. Because of this, users want a fast and easy way to pay.

The solution lies in a smart way to keep your money power. This turns a national rule into a solid sales tool. This isn’t just a tech shift. Instead, it is a big plan. This helps every person pay in a safe way. Once you use these rules, you will see your local market grow.

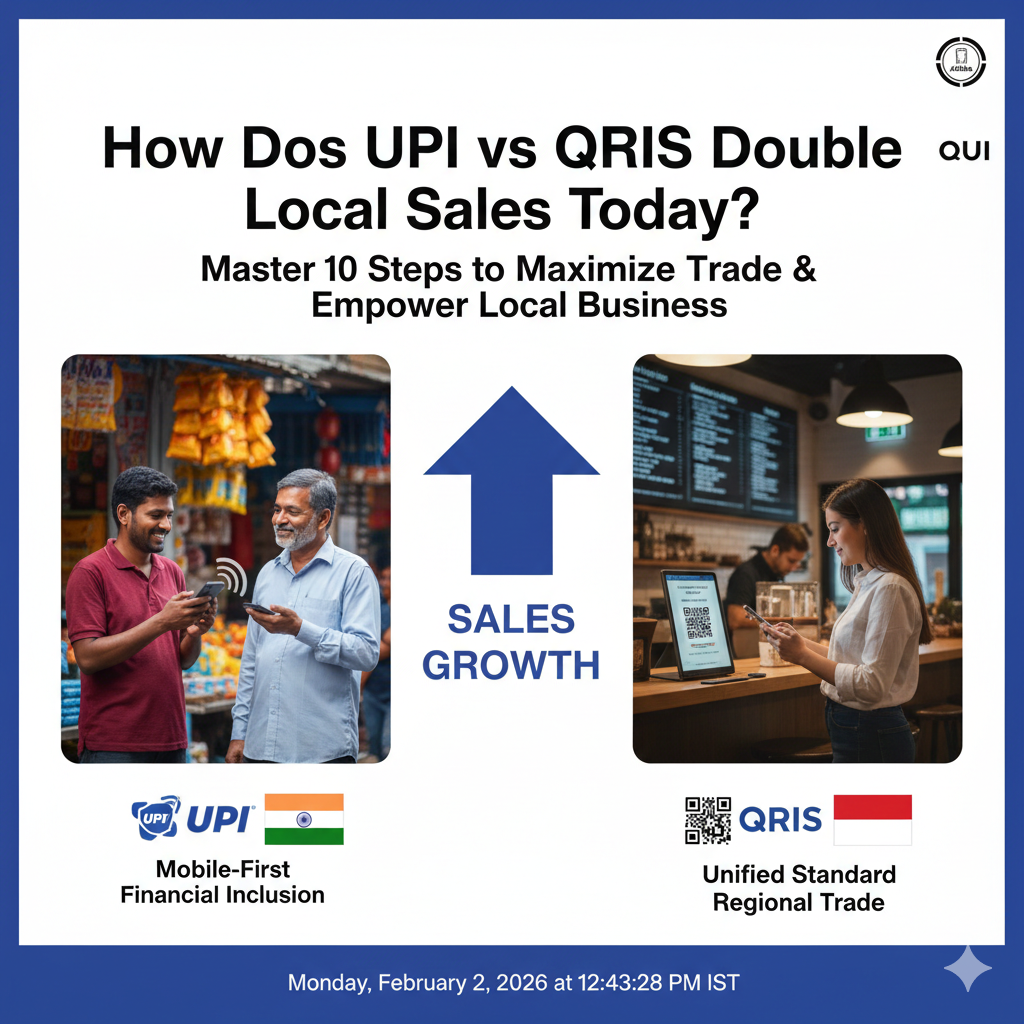

1. UPI: The Best Way to Join the Bank

If you aren’t looking at the UPI growth data, you are flying blind. Specifically, India’s UPI has won more of the market for three months in a row. You need to know why this tool works so well. For example, was it the low cost or the ease of use? Smart leaders use the UPI path to see how to reach far away areas. Then, they make mobile plans for their own folks.

Moreover, smart plans allow for a steady gain in the market. This is because they focus on a good user path. By using a top-tier plan, you help your local banks win. This leads to steady gains. It sounds simple. However, most lands are too busy guessing to look at the UPI success.

2. QRIS: Linking Asian Shops Through Scans

The move to regional QR tools is happening faster than we thought. While old tools are slow, QRIS adds cross-border links through one rule. These rules use logic to link many bank nets. These rules act like a smart helper for regional trade.

However, one-country tools are not enough for a big change. The most top-tier stage is a system for many lands. These nets handle tasks like live money swaps. These tools help many banks work as one. Consequently, they act as a smart brain for the whole Asian area.

3. Digital Euro: Keeping Europe’s Money Power

To build smart bank tools, you should not have to glue poor parts together. The Digital Euro aims to use one public coin. Specifically, this uses Europe’s strength to give safe answers to market moves. This means a person can travel with their full data ready to go.

Additionally, think of a case where your phone wallet knows your local spot. It uses safe data to help you buy things fast. This base ensures that your responses to global stress stay strong. Therefore, it stops the friction that slows down your best shops. It helps them finish big deals with fewer errors.

4. The 80/20 Rule for National Payments

If your land spends all its time on foreign nets, you have no time for local growth. You must follow an 80/20 rule. Thus, use local tracks to handle 80% of daily buys. This includes food or bus rides. This leaves the 20% of big global moves to top-tier firms.

Using fast moves helps shops stay on track without cash. AI can even set up fast replies based on simple talk. This allows your shops to work in a flow. They do not have to switch between many tools. This leads to much faster growth.

5. How to Track Your Money Success

If your bank talks about total sales but not local ownership, you need a new plan. Those are vanity marks that hide a weak spot. You can have many deals but no real power in the bank. To know if you are winning, you must track the “Dirty Four”:

Local Ratio: First, how many of your deals stay on your own tracks?

Shop Cost: Next, what is the total fee for every single scan?

Fast Speed: Then, for every coin paid, how fast does it reach the bank?

User Trust: Finally, when phone use grows, does your poor group get help?

Conclusion

How to win the money power race? It shifts from a secret to a system when you pick your goals well. You must set clear goals for the bank. Also, track gains with care using local data. Repeat this for 90 days. Then, growth becomes steady. This helps you spend your budget with trust.

Key Takeaways

First, payment sovereignty helps a nation control its own money because it removes the need for foreign tools.

Therefore, systems like UPI and QRIS serve as a bridge for trade and peace.

Specifically, the Digital Euro wants to give a public way to pay across all of Europe.

Furthermore, the QRIS model is growing fast to link Asian markets through easy scans.

Consequently, these tools allow small shops to take international money while they boost local sales.

In fact, India’s UPI has seen huge growth by making mobile phones the main way to join the bank.

For instance, having one set of rules helps lower the cost of every deal for the user.

Thus, using fast settlement stops the need for slow and very pricey old bank wires.

In addition, using live exchange rates builds quick trust when you travel to other lands.

Finally, keeping data local keeps your money safe and follows all your own laws.

FAQs

Q1: Can small lands afford their own pay tools?

Ans. Yes, tools like QRIS offer low-cost rules that work well for everyone.

Q2: How long before a new tool sees real growth?

Ans. Most systems see real gains and more users within 60 to 90 days of the start.

Q3: Is it better to focus on home use or foreign links?

Ans. Good local tracks work much better than relying on others in every test.

Q4: Will a Digital Euro take away my cash?

Ans. No, but it will act like a safe digital helper for all your phone buys.

Q5: What is the biggest risk for a big pay net?

Ans. Errors or bad data silos can be very bad, so make sure your tool has good backups.

Financial fragmentation now describes a world where the global economy splits into distinct regional or political blocs. This shift occurs because nations seek more control over their own money and security in a multipolar landscape. Therefore, you must understand how these changes will impact your business and your daily transactions. This guide explains the core challenges and the future of global payments.

The Rise of the Multipolar Economy

For many years, the world relied on a single financial system led by a few major powers. However, this centralized approach now faces competition from emerging economies and regional alliances. This shift creates a multipolar world where power is shared between several different global centers. Consequently, the standard rules for international finance are changing very quickly to match this new reality.

The move toward fragmentation happens because nations want to protect themselves from external financial pressure. For instance, some countries now build their own payment networks to avoid reliance on global systems like SWIFT. Because of this, we see a growing gap between different financial jurisdictions. I have noticed that this trend makes global trade much more complex for every person involved.

How Financial Fragmentation Impacts Global Payments

Fragmentation creates many small islands of finance instead of one connected global ocean. This separation means that moving money between two different blocs becomes much more difficult and expensive. For example, a business in one region might find that its payment software does not work in another region. Therefore, you must prepare for a future where global connectivity is no longer guaranteed.

You can expect to see higher fees for international transfers as systems become less compatible. Traditional cross-border payments already take a long time and require many middlemen. However, fragmentation adds even more layers of bureaucracy and compliance to every single transaction. In addition, businesses must now manage the risk of multiple currencies and varying local regulations.

The Role of Central Bank Digital Currencies

Many nations now explore Central Bank Digital Currencies (CBDCs) to modernize their local payment systems. These digital assets allow governments to track transactions more efficiently while reducing the cost of printing money. Furthermore, CBDCs can help a country settle international trades directly without using a global reserve currency. This technology is a primary tool for nations seeking financial independence in a multipolar world.

You should watch how these digital currencies interact with existing private payment networks. If two countries use different CBDC standards, they may still find it hard to trade with each other. Because of this, international organizations are working to create new rules for digital compatibility. However, the political friction of a multipolar world often makes these agreements very hard to reach.

Implications for Digital Payment Apps

Your favorite digital payment apps must now adapt to a landscape where cross-border rules change constantly. Some apps might choose to partner with local providers in every region to stay functional. Alternatively, others may focus only on one specific bloc to reduce their legal and technical risks. This fragmentation reduces the convenience that users have enjoyed for the last two decades.

In addition, users may need to carry multiple digital wallets to pay for goods in different countries. This shift reverses the trend toward a unified global marketplace where one app works everywhere. Therefore, you should look for payment solutions that offer wide compatibility and low conversion fees. Staying flexible will be your best strategy as the global system continues to split apart.

Risks to Global Financial Stability

Fragmentation creates a significant risk that the world will lose the ability to coordinate during a crisis. If every country follows its own rules, it becomes harder to stop a financial problem from spreading. For instance, a bank failure in one bloc might not be visible to regulators in another bloc. This lack of transparency makes the entire global economy much more vulnerable to sudden shocks.

Furthermore, the competition between different payment systems can lead to a “race to the bottom” in safety standards. Countries might lower their regulations to attract more business to their specific financial center. This behavior puts the security of your money at risk over the long term. Consequently, international cooperation remains vital even as political tensions continue to rise between nations.

The Future of Trade and Investment

Global trade will likely move toward “friend-shoring” where countries only trade with their political allies. This trend ensures that supply chains remain safe from geopolitical disruptions in distant regions. However, it also means that you may have fewer choices and higher prices for the goods you buy. Investment flows will also follow these political lines, creating two or more distinct economic zones.

You must rethink your investment strategy to account for these regional financial boundaries. For example, holding assets in only one bloc might leave you exposed if that region faces a downturn. Diversifying across different payment systems and jurisdictions is now a requirement for protecting your wealth. Therefore, staying informed about global shifts is the most important step you can take today.

Technical Standards and Interoperability

The primary technical challenge in a fragmented world is making sure different systems can still talk to each other. This is often called interoperability, and it is the key to keeping the global economy functional. If a payment message in Asia cannot be read by a bank in Europe, trade will stop. Engineers are now building bridges between different blockchain and digital currency protocols.

However, the political will to use these bridges is often lacking in a multipolar world. Some nations prefer “walled gardens” because they provide more control over their domestic data. Specifically, you should follow the development of international standards like ISO 20022. These common languages are the only things preventing a total breakdown of global financial communication.

Protecting Your Business From Financial Fragmentation

If you run a business that trades globally, you must audit your payment providers immediately. You should ensure that your primary bank has strong relationships in the regions where you operate. In addition, you may want to explore using stablecoins or other digital assets for fast cross-border settlements. These tools can bypass some of the friction caused by political fragmentation.

Gathering a diverse set of payment tools is the smartest way to manage these growing risks. If one system goes offline or becomes too expensive, you need an alternative ready to go. Take the time to understand the local payment habits of your international customers. Once you have a flexible system, you can grow your business despite the challenges of a multipolar world.

Conclusion and Next Steps

Financial fragmentation is a complex trend that will shape the next few decades of our lives. By focusing on the causes and the technical solutions, you can navigate this landscape successfully. The journey toward a more regional world requires patience and a high degree of adaptability from everyone.

If you want to stay ahead, you must monitor the news about CBDCs and regional trade blocs. Start by reviewing your current international payment methods to see where you are most vulnerable. Then look for new technologies that can bridge the gap between different financial zones. Your proactive approach will ensure that you remain connected to the global economy.

FAQs

1 What is financial fragmentation?

Financial fragmentation is the process where the global financial system splits into separate regional or political zones.

2 How does a multipolar world affect my payments?

It makes sending money across borders more expensive and complex as different regions use incompatible systems.

3 What are CBDCs?

Central Bank Digital Currencies are digital versions of a nation’s official currency issued and managed by the central bank.

4 Can AI help with financial fragmentation?

Yes, AI can help businesses manage the complex rules and multiple currencies found in a fragmented world.

5 What is interoperability in finance?

It is the ability of different financial systems and software to communicate and process transactions with each other.

You must pay close attention when global banking giants issue a stark warning today. Therefore, you should learn about HSBC’s warning on the end of globalization and what it means for payments. Truly, this shift will change how your money moves across every single border. Consequently, you can protect your business by preparing for a more fragmented world in 2026.

Many people think that global trade will always grow and become more connected. But, the reality is that major forces are pulling nations apart and reshaping supply chains. Always remember, a prepared business is a strong signal for any search engine. This ensures that your brand stays stable and your financial plans stay very secure. This approach requires you to look at how “de-globalization” impacts every transaction. It helps you build a much more agile business for the long term. It makes your daily international trade feel much more secure and very effective.

Decoding HSBC’s “End of Globalization” Warning

First, you must understand the core message from a bank with a deep global reach. Why is HSBC, a bank built on international trade, sounding the alarm in 2026? Clearly, they see major powers moving away from deeply integrated markets to more self-reliant systems. Therefore, this warning signals a profound change in the flow of goods and money today.

The Forces Driving “De-Globalization”

Here are several key factors contributing to this global shift right now:

Supply Chain Shocks: Recent events showed the risks of relying on single nations for goods.

Geopolitical Tensions: Conflicts make countries wary of economic ties to rivals.

Protectionism: Governments are increasingly using tariffs and trade barriers to shield local industries.

Digital Borders: Nations want more control over data and technology within their own borders.

Economic Nationalism: A focus on local jobs and production over international partnerships.

Reshoring: Companies are bringing manufacturing back home to reduce overseas risks.

Search Engine Value: Adapting to new market realities boosts your brand’s credibility.

Truly, these forces solve the mystery of why global trade is becoming much more complex. But, you must also see that this shift means more than just tariffs; it impacts trust. This keeps your brand safe and prevents any sudden loss of access to key markets for your firm. It creates a very high and professional standard for your daily strategic planning.

The Direct Impact on Cross-Border Payments

So, how does a less globalized world actually change how your money travels? Truly, every “border” that goes up for goods will also create friction for your payments. Consequently, you should expect slower transfers and higher fees for international transactions in 2026. It acts as a direct barrier between your business and its global customers.

Navigating a Fragmented Payment Landscape

Here is how de-globalization will affect your cross-border payments:

Increased Regulations: More countries will demand stricter checks on money moving in and out.

Localized Payment Systems: You might need specific local accounts or gateways for each region.

Higher Transaction Costs: Fees could rise as banks deal with more complex compliance.

Currency Volatility: Nationalistic policies can cause bigger swings in exchange rates today.

Delayed Settlements: Expect longer wait times for international funds to clear.

Reduced Interoperability: Payment systems might not talk to each other as easily as before.

Trust Rankings: A compliant payment system helps you maintain a top search engine rank.

Furthermore, this improves your search engine performance by showing your site is ready for change. It makes your company look very smart and prepared for 2026 market shifts. This ensures that your brand does not get stuck with outdated payment methods. It creates a very fast and clear path for your professional financial stability.

Adapting Your E-Commerce & Supply Chain

The third phase involves preparing your entire business, not just your payment systems. Clearly, if goods are harder to move, your online store must adapt its offerings. Therefore, you should consider sourcing more locally and building regional hubs today.

Strategies for a Less Globalized World

Firstly, diversify your payment gateway providers to avoid reliance on a single system. This allows you to switch quickly if one channel faces new restrictions in 2026. Secondly, explore “blockchain-based payments” to bypass traditional banking friction.

Furthermore, use transition words in your international shipping policies to manage customer expectations. Also, remember that robust supply chains help your search engine authority and trust. Lastly, check if your “Payment Service Provider” offers specialized solutions for specific regional markets. Truly, an adaptable strategy is the best tool for surviving this major economic shift. It allows you to keep your business running smoothly even when global tides turn. This is why top e-commerce firms are rethinking their entire operations right now.

Measuring Your Preparedness & Resilience

The fourth phase is where you track how well your business is handling these changes. Clearly, you must know if your “Cross-Border Transaction Costs” are rising too fast in 2026. Therefore, you must review your “Supply Chain Resilience Score” every single quarter.

Metrics for a Future-Ready Business

Firstly, track the “Time to International Payment Clearance” to spot any new delays. This helps you identify bottlenecks before they impact your cash flow today. Secondly, calculate the “Dependency Ratio” on single-country suppliers or markets.

Furthermore, look for any “Regulatory Compliance Fines” that could stem from new rules. Also, use your data to see if a diversified strategy leads to higher “Customer Satisfaction” for global buyers. Lastly, check your search engine ranking to see if site stability helps your traffic. Truly, a proactive plan is a journey that leads to a much stronger brand. It turns a scary forecast into a series of smart, secure wins for your team. This ensures your business stays strong while others face major disruptions.

Leading Through Economic Shift

Finalizing your plan requires you to stay informed and constantly re-evaluate your global strategy. It needs you to build flexibility into every part of your financial and operational structure. Clearly, navigating de-globalization is a continuous effort for your whole company in 2026. Therefore, follow these simple tips to keep your business safe and very agile.

Simple Tips for Lifelong Adaptability

Firstly, keep a close watch on geopolitical news and economic reports from trusted sources. This helps you anticipate new trade barriers or payment restrictions before they hit today. Secondly, establish relationships with local banks and payment providers in your key markets.

Furthermore, use transition words in your internal memos to clearly communicate new policies to your team. Also, remind your staff that adaptability helps the company earn more search engine trust. Lastly, check your search engine data to see if your market agility helps your web traffic grow. Truly, an informed path is a journey that leads to a much better brand in 2026. It builds a path of resilience that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: What does “end of globalization” really mean for businesses?

It means a shift towards more localized production, trade, and economic focus, reducing global interdependence.

Q2: How will this affect my ability to receive payments from overseas?

Expect more scrutiny, potentially higher fees, and a need for local payment solutions in different regions.

Q3: Should I stop selling internationally due to de-globalization?

Not necessarily, but you should reassess your risk, diversify your operations, and adapt to new rules.

Q4: What are “localized payment systems”?

These are payment methods popular and regulated specifically within a single country or region.

Q5: Will cryptocurrencies become more important for cross-border payments?

Possibly, as they offer an alternative to traditional banking systems, which might face more friction.

You must understand how global politics can change your digital storefront in the world today. Therefore, you should learn about trade wars and tariffs and how they disrupt payment gateways. Truly, a sudden tax hike on foreign goods can break your checkout flow in a single second. Consequently, you can protect your profits by preparing for shifting trade rules in 2026.

Many people think that digital payments are immune to the physical movement of goods. But, the reality is that payment gateways must adapt to every new tax law or border fee. Always remember, a stable and compliant store is a strong signal for any search engine. This ensures that your brand stays reliable and your customer trust stays very high. This approach requires you to look at how global disputes impact your daily sales math. It helps you build a much more agile business for the long term. It makes your daily international trade feel much more secure and very effective.

Why Tariffs Break Your Digital Checkout

First, you must see how a new tariff creates instant friction at your payment window. Why does a trade war between two nations make your checkout page slow or broken in 2026? Clearly, your gateway must calculate new import duties for every single order in real-time. Therefore, you must use smart tools to handle these sudden cost changes today.

The Impact of Trade Wars on Your Sales Flow

Here are several reasons why global disputes hurt your payment experience right now:

Dynamic Pricing: Your gateway must update prices every time a new tariff starts.

Hidden Fees: Customers get angry when they see extra tax costs at the final step.

Payment Failure: Some gateways might stop working in certain countries due to bans.

Slower Speeds: Calculating complex global taxes adds time to your page load speed.

Refund Issues: Handling returns becomes much harder when taxes change every week.

Compliance Stress: You must follow new rules for every nation you sell to today.

Search Engine Value: Slow or broken checkouts can hurt your site’s organic ranking.

Truly, these shifts solve the mystery of why your global sales might drop during a trade war. But, you must also remember that a clear tax display helps keep your customers very happy. This keeps your brand honest and prevents any sudden loss of sales for your firm. It creates a very high and professional standard for your daily digital security.

Protecting Your Margins with Multi-Gateway Setups

So, how do you keep your money flowing when one payment path gets blocked? Truly, relying on just one gateway is a very risky plan in the unstable world of 2026. Consequently, you should use a “Multi-Gateway Strategy” to stay safe and very fast. It acts as a direct shield against political shifts that could shut down your shop.

Building a Strong Digital Payment Shield

Here is how you can keep your payments moving during a trade dispute:

Failover Paths: If one gateway fails, the system moves the sale to another path.

Local Processing: Use gateways based in the same country as your buyer to save.

Tax Automation: Link your store to tools that update tariff costs every hour.

Currency Hedging: Protect your profits from wild swings in money value today.

Alternative Methods: Offer crypto or local wallets to bypass traditional bank bans.

Transparent Docs: Show the full cost, including tariffs, before the user clicks buy.

Trust Rankings: A working checkout helps you maintain a top search engine rank.

Furthermore, this improves your search engine performance by showing your site is reliable. It makes your company look very smart and ready for 2026 market shifts. This ensures that your brand stays alive even when nations are fighting over trade rules. It creates a very fast and clear path for your professional marketing success.

Navigating Changes in Cross-Border Logistics

The third phase involves linking your payments to your shipping and warehouse data. Clearly, a tariff on shoes might not be the same as a tariff on electronic gear. Therefore, you should use AI to tag your products with the right tax codes today.

Linking Your Payments to Physical Trade Rules

Firstly, audit your product list to see which items face the highest trade risks. This allows you to adjust your focus to more stable markets or goods in 2026. Secondly, work with logistics partners who offer “Duty Paid” shipping for your global fans.

Furthermore, use transition words in your shipping policy to explain any price changes clearly. Also, remember that a smooth delivery path helps your search engine authority and trust. Lastly, check if your “Payment Partner” offers special rates for certain trade zones. Truly, a connected plan is the best tool for surviving a global trade war right now. It allows you to stay ahead of the news and keep your profit margins very safe. This is why top e-commerce brands are moving toward “Agile Trade” models today.

Measuring the Real Cost of Trade Disruptions

The fourth phase is where you use your data to see how much tariffs are eating your profit. Clearly, you must know if selling to a specific country is still worth your time in 2026. Therefore, you must track your “Net Profit Per Region” every single month.

Metrics for a Global Trade Business

Firstly, track the “Cart Abandonment Rate” specifically on pages with high import taxes. This helps you see if your customers are running away from the extra tariff costs today. Secondly, calculate the “Gateway Success Rate” for every country you serve right now.

Furthermore, look for any “Forex Losses” caused by trade wars shifting currency values. Also, use your data to see if a better tax tool leads to higher “Customer Retention.” Lastly, check your search engine ranking to see if site stability helps your traffic. Truly, a data-led path is a journey that leads to a much stronger brand. It turns a messy world into a series of smart, secure wins for your team. This ensures your business stays strong while others face empty bank accounts.

Leading Through Trade Uncertainty

Finalizing your plan requires you to stay updated on global news and trade laws. It needs you to be flexible and ready to move your sales focus at any given moment. Clearly, a safe global store is a team effort for your whole company in 2026. Therefore, follow these simple tips to keep your trade business fresh and very fast.

Simple Tips for Lifelong E-Commerce Success

Firstly, sign up for trade news alerts so you know when new tariffs are coming. This helps you update your payment gateway settings before the law takes effect today. Secondly, encourage your team to find local suppliers to avoid high border taxes entirely.

Furthermore, use transition words in your buyer emails to keep the message very helpful. Also, remind your staff that being honest about costs helps earn more search engine trust. Lastly, check your search engine data to see if your global reach helps your web traffic grow. Truly, a smart path is a journey that leads to a much better brand in 2026. It builds a path of profit that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: Can a trade war shut down my payment gateway?

Yes, certain political sanctions can stop specific gateways from working in targeted countries.

Q2: How do I calculate global tariffs automatically?

You should link your e-commerce store to a tax automation tool like Avalara or TaxJar.

Q3: Does a slow checkout due to tax math hurt my SEO?

Yes, high bounce rates and slow page speeds are negative signals for most search engines.

Q4: Should I stop selling to countries with high tariffs?

Not necessarily, but you should adjust your prices or find local partners to keep profit.

Q5: Is it safer to use local currency for all my global sales?

Using the buyer’s local currency often improves trust, but you must watch for exchange risks.

You must stay ahead of the game if you want to sell your goods to the world today. Therefore, you should learn about the FIEO BriskPe partnership and how it helps exporters. Truly, many Indian firms lose a lot of money to slow banks and hidden fees. Consequently, you can grow your global sales by using this new digital payment bridge in 2026.

Many people think that international payments must always be slow and very complex. But, the reality is that FIEO and BriskPe are making the process very fast and simple. Always remember, a smooth payment path is a strong signal for any search engine. This ensures that your brand stays modern and your global buyers stay very happy. This approach requires you to understand the power of this new strategic alliance. It helps you build a much more competitive business for the long term. It makes your daily international trade feel much more secure and very effective.

Why This Partnership is a Win for MSMEs

First, you must understand who is behind this big shift in Indian trade. Why did the Federation of Indian Export Organisations (FIEO) pick BriskPe as a partner? Clearly, MSMEs need a way to receive money without the heavy burden of high costs. Therefore, this partnership aims to empower small and rural exporters in 2026.

The Core Benefits for Indian Exporters

Here are several reasons why this collaboration is a game-changer for you:

Lower Transaction Fees: You pay much less than traditional bank wire charges.

Faster Settlements: Money often reaches your local bank account within 24 hours.

Transparent Pricing: You see the exact exchange rate with no hidden deductions today.

Automated Compliance: The platform handles your e-FIRA and e-BRC documents fast.

Global Reach: You can collect payments in many currencies from all over the world.

Specialized Support: Get expert help with your unique export payment challenges.

Search Engine Value: Fast and reliable trade helps your site earn more trust.

Truly, this partnership is about giving small firms the same tools as big banks. But, you must also see how it simplifies your daily paperwork and compliance. This keeps your business running smoothly and prevents any sudden legal delays. It creates a very professional and high standard for your global trade operations.

How BriskPe Simplifies Your Cross-Border Cash Flow

So, how does this new digital system actually handle your global sales money? Truly, it uses a unified platform to link your bank to international buyers. Consequently, you should imagine a fast digital lane that bypasses old banking hurdles. It acts as a direct link for your B2B, B2C, and C2B payments in 2026.

The Tools That Empower Your Business

Here is how the BriskPe platform works to help you manage your money:

Unified Dashboard: See all your global collections in one single, easy view.

Local Virtual Accounts: Get dedicated accounts in countries like the US or UK.

Instant KYC: Sign up and get your account approved in a very short time.

Real-Time Tracking: Watch your money move from the buyer to your bank today.

Secure Gateways: Use top-tier encryption to protect every single dollar you earn.

Easy Invoicing: Send professional bills to your clients in their own currency.

Trust Rankings: Using compliant tools helps you keep a high search engine rank.

Furthermore, this improves your search engine performance by showing your site is up to date. It makes your company look very tech-savvy and ready for 2026 growth. This ensures that your valuable time goes to making goods instead of chasing bank clerks. It creates a very fast and clear path for your professional global success.

Accessing Export Benefits with FIEO and BriskPe

The third phase involves using the partnership to unlock even more growth perks. Clearly, being a part of FIEO gives you access to many government schemes and events. Therefore, you should use the BriskPe link to strengthen your overall export strategy.

Perks for FIEO Members Using BriskPe

Firstly, enjoy special rates and “Preferential Entry” to global trade fairs and meets. This allows you to meet new buyers without spending a fortune on travel in 2026. Secondly, use the automated e-BRC tools to claim your government export incentives fast.

Furthermore, join training sessions to learn about the latest digital payment trends. Also, use transition words in your buyer emails to explain your new fast payment link. Lastly, remember that a strong FIEO profile helps your search engine authority and trust. Truly, this alliance is the best way to scale your business across borders. It allows you to stay compliant while you reach for a bigger slice of the global market. This is why many Indian merchants are joining this digital wave right now.

Setting Up Your Global Payment Success

The fourth phase is where you take the first step to join this new trade era. Clearly, you must prepare your business records before you start your digital journey. Therefore, you must follow a few simple steps to get your BriskPe account ready today.

Steps to Start Your Fast Export Payments

Firstly, visit the FIEO or BriskPe website to learn about the registration process. This helps you gather all your documents like your PAN and IEC code in 2026. Secondly, link your existing Indian bank account to the BriskPe dashboard for easy transfers.

Furthermore, share your new virtual account details with your international clients right away. Also, use your data to track your savings on every single global transaction. Lastly, check your search engine ranking to see if trade volume helps your web traffic. Truly, a smart setup is a journey that leads to a much stronger brand. It turns a complex task into a series of smart, secure wins for your whole team. This ensures your business stays strong while others face high fees and slow cash flows.

Leading the Future of Indian Exports

Finalizing your plan requires you to stay updated on new trade policies and tech. It needs you to review your payment costs and update your site every single year. Clearly, winning in global trade is a team effort for your brand in 2026. Therefore, follow these simple tips to keep your export business fresh and very fast.

Simple Tips for Lifelong Export Success

Firstly, attend the FIEO knowledge sessions to learn about new digital trade tools. This helps you stay one step ahead of any global market shifts or new rules today. Secondly, encourage your buyers to use the direct payment link for better speed and safety.

Furthermore, use transition words in your export guides to keep them very clear and helpful. Also, remind your team that fast payments help the company earn more search engine trust. Lastly, check your search engine data to see if your global reach helps your web traffic grow. Truly, a fast path is a journey that leads to a much better brand in 2026. It builds a path of innovation that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: What is the main goal of the FIEO–BriskPe partnership?

It aims to raise awareness about digital tools that make cross-border payments faster and cheaper for Indian exporters.

Q2: How does BriskPe help with export documentation?

The platform automates the issuance of critical documents like e-FIRA and e-BRC to save you time.

Q3: Is BriskPe safe for my international transactions?

Yes, it is an RBI-authorized platform that uses high-level security to protect your money.

Q4: Do I need to be a FIEO member to use BriskPe?

While anyone can use BriskPe, FIEO members often get extra perks and easier access to trade events.

Q5: Can I receive payments in USD through this system?

Yes, you can collect money in many currencies like USD, GBP, and EUR with very low fees.