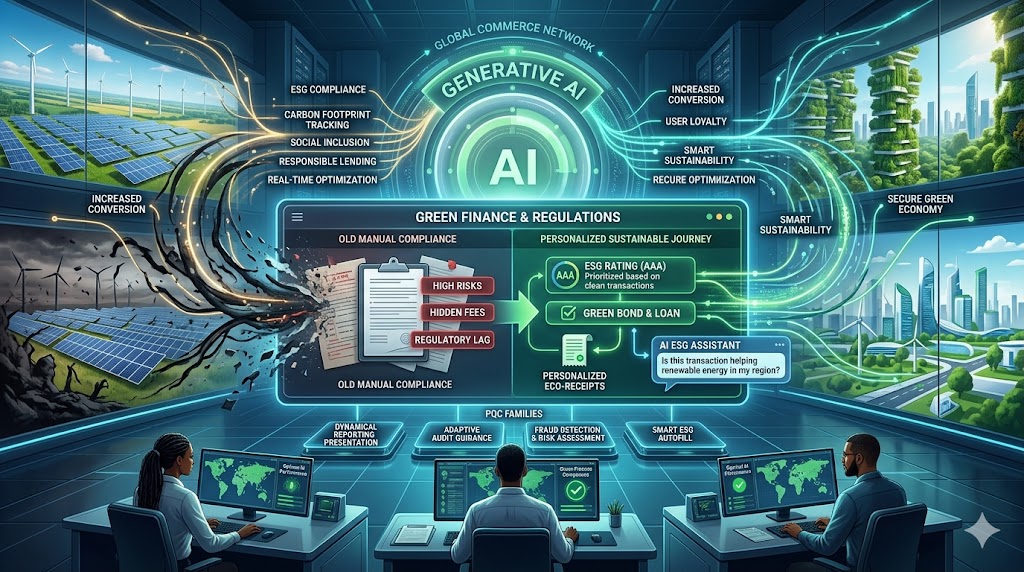

The world of money is changing to help save our planet. Today, many people care about the environment and social fairness. This is often called ESG. Because these values are so important, they are now part of global finance. Therefore, banks and payment firms must follow new green rules to stay in business. If they ignore these trends, they might face heavy fines and lose their good name. In short, the future of finance is green.

Why ESG Matters for Every Transaction

Traditional banking used to focus only on profits and speed. However, regulators now look at how money flows affect the earth. Consequently, every major player in finance must track their carbon footprint. This is because digital payments use a lot of energy in data centers. Furthermore, users want to know if their bank supports clean energy. Therefore, finance is no longer just about numbers; it is about values.

Another big issue is social fairness in the payment world. For instance, many people in poor areas still lack basic tools to pay. If a system is not inclusive, it fails the “S” in ESG. Thus, modern finance must ensure that everyone has a fair chance to use digital money. A smart strategy solves this by offering low-cost tools for every citizen. This keeps the economy healthy and builds a better society for all.

How New Regulations Change the Game

Strict green rules are a vital part of modern trade. In many regions, firms must report how much energy their systems consume. Because this transparency is required by law, it builds more trust with the public. Furthermore, a green approach in finance can lead to lower taxes for eco-friendly firms. This means that being good to the planet can actually save a company money. In short, finance wins when it aligns with the health of the world.

Green bonds and sustainable loans are also growing fast. Instead of generic funding, banks offer special deals for green projects. Because these loans are tied to ESG goals, they encourage better behavior. Therefore, finance experts are building new frameworks to track these results accurately. This ensures that the money actually helps build wind farms or solar plants. Finally, these regulations ensure that “green” is a real action and not just a marketing trick.

Staying Safe and Compliant

Security and ethics are the most important parts of green trade. Hackers are always looking for ways to exploit new systems. Luckily, new AI tools are great at spotting fraud while staying energy-efficient. If a transaction looks odd, the system stops it fast. This keeps your money and your data very safe. Because the AI is so smart, it rarely blocks real customers. Thus, finance stays strong and secure for every global user.

Additionally, digital receipts help reduce waste without making the process slow. It uses cloud tech to prove the sale is real in a second. When you use these tools, the checkout flow feels very smooth and eco-friendly. You just click and go. Therefore, the risk of a mistake or paper waste is very low. This is the future of finance in a sustainable world. Finally, safety ensures that users feel comfortable trusting their money with green firms.

The Big Future of Sustainable Money

We are only at the start of a massive green shift. Soon, every payment app will show you the carbon cost of your coffee or clothes. This means we will see a huge need for clear and honest data. Instead of a hard process, we get a tailored world of green choices. Sustainable finance makes every transaction feel like a positive step for the earth. It is the best way to shop in 2026. If you want to stay ahead, you must use these green tools now. In conclusion, ESG is the new engine for global growth.

Frequently Asked Questions

1. Does green finance make payments more expensive?

No, it often leads to better efficiency which can lower costs for the user over time.

2. How does a payment app help the planet?

By using green data centers and offering digital receipts to save millions of trees.

3. What does ESG stand for in banking?

It stands for Environmental, Social, and Governance rules that guide fair and green trade.

4. Can I choose a green bank for my store?

Yes, many banks now have special ESG ratings to show they are eco-friendly.

5. Will all finance become green soon?

Yes, most global regulators are making green rules a requirement for all firms by 2027.

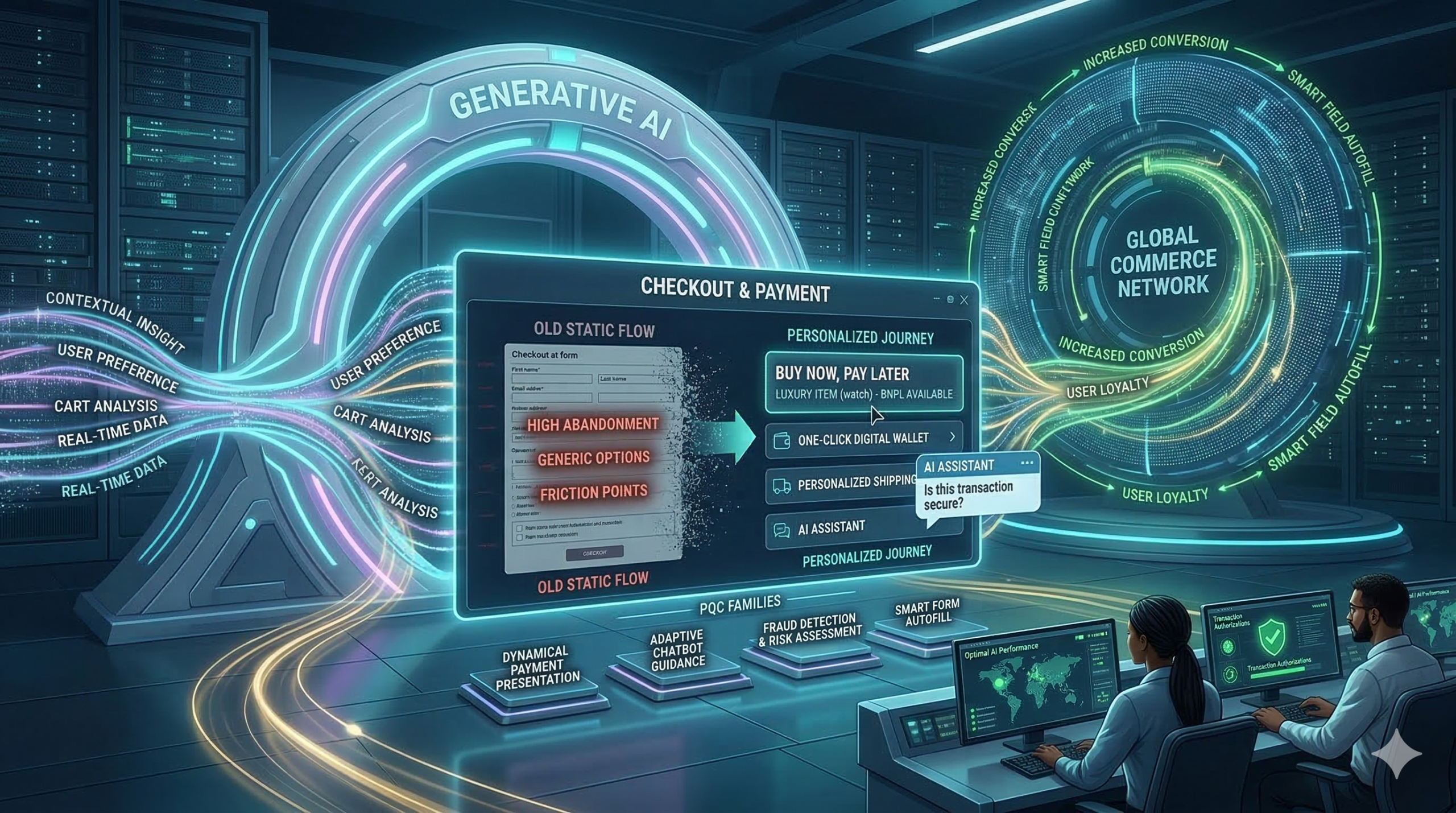

Most online stores lose customers at the final step because traditional checkout pages are often slow and boring. Now, generative ai is changing that forever by creating a personal path for every shopper. Because this technology learns what you like and how you want to pay, buying things online is faster than ever. Furthermore, smart stores use generative ai to turn one-time shoppers into loyal fans. This shift is vital for any brand that wants to grow. Consequently, the payment journey is no longer just a task; it is an experience.

Why Old Checkout Systems Fail

Static forms are the biggest enemy of sales because most shops show the same fields to everyone. Consequently, many people leave their carts empty. This is because the process feels long and hard. Generative ai solves this by making every page unique for the user. For instance, it knows if you are on a phone or a laptop. Furthermore, it predicts which payment method you prefer. Therefore, you spend less time typing and more time enjoying your purchase. In short, ai removes the friction that kills sales.

Real-Time Help with Generative AI

Shopping can sometimes feel confusing, especially when you have questions about shipping or taxes. Standard help pages are often hard to find. However, ai adds a smart assistant to the page to guide you. This bot answers your questions in seconds. Because the bot knows your cart, it gives perfect advice. This builds trust and keeps you moving forward. In addition, ai makes sure you never feel alone while shopping.

Moreover, these bots can offer special deals at the perfect moment. If you hesitate, the generative ai might give you a small discount to help you decide. As a result, shoppers feel valued and safe. Generative ai is not just a tool; it is a digital guide. Because of these benefits, top brands are moving to AI today. Therefore, the checkout flow becomes a conversation instead of a form.

Safer and Faster Payments

Security is the most important part of any sale because hackers are always looking for ways to steal data. Luckily, ai is great at spotting fraud by looking at millions of data points in real-time. If it sees something odd, it stops the threat fast. This keeps your money and data very safe. Because the ai is so smart, it rarely blocks real customers. Thus, generative ai makes payment security much stronger for everyone.

Additionally, generative ai helps with filling out forms by guessing your address with high accuracy. This reduces errors and saves time for the customer. When you use generative ai, the checkout flow feels like magic. You just click and go. Therefore, the risk of a mistake is very low. This is the future of ai in the payment world. Finally, this technology ensures that safety does not come at the cost of speed.

The Big Future of Generative AI

We are only at the start of this change. Soon, every store will use ai to talk to us. It will know our size, our style, and our budget. This means we will see fewer ads we do not like. Instead, we get a tailored world of products. Generative ai makes every transaction feel human. It is the best way to shop in 2026. If you want to stay ahead, you must use generative ai now. In conclusion, the personalized payment journey is the new standard for global trade.

Frequently Asked Questions

1. Is generative ai safe for my credit card?

Yes, it improves security by spotting fraud much faster than older systems.

2. Does generative ai make my phone slow?

No, most of the work happens on fast servers, so your phone stays quick.

3. Why do stores need ai?

It helps them sell more by making the checkout process easy and personal for everyone.

4. Can generative ai help with returns?

Yes, it can guide you through the return process and answer policy questions instantly.

5. Will all stores use generative ai soon?

Yes, it is becoming the global standard for all top e-commerce websites.

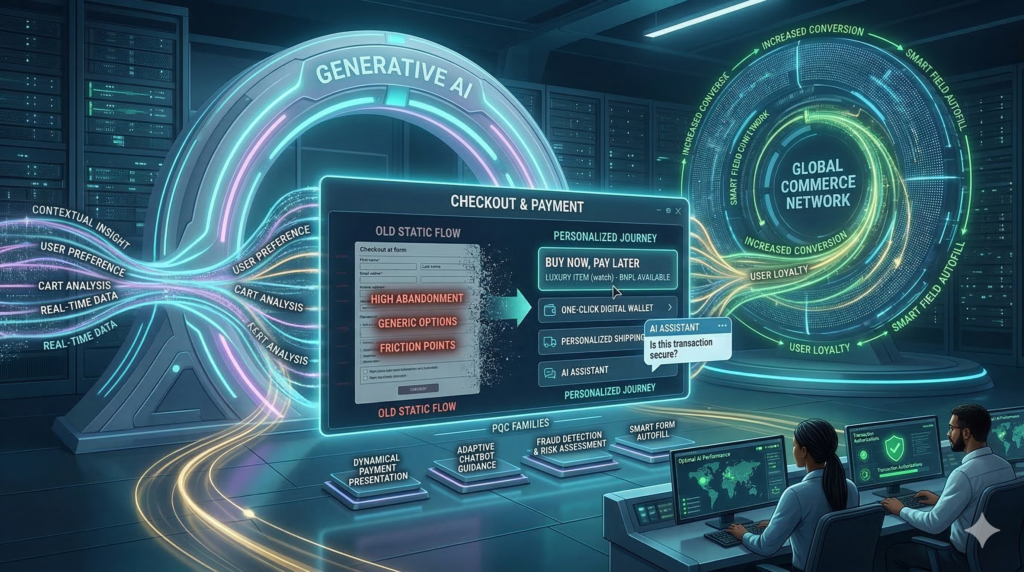

Most online stores lose customers at the final step because traditional checkout pages are often slow and boring. Now, generative ai is changing that forever by creating a personal path for every shopper. Because this technology learns what you like and how you want to pay, buying things online is faster than ever. Furthermore, smart stores use generative ai to turn one-time shoppers into loyal fans. This shift is vital for any brand that wants to grow. Consequently, the payment journey is no longer just a task; it is an experience.

Why Old Checkout Systems Fail

Static forms are the biggest enemy of sales because most shops show the same fields to everyone. Consequently, many people leave their carts empty. This is because the process feels long and hard. Generative ai solves this by making every page unique for the user. For instance, it knows if you are on a phone or a laptop. Furthermore, it predicts which payment method you prefer. Therefore, you spend less time typing and more time enjoying your purchase. In short, it removes the friction that kills sales.

Real-Time Help with Generative AI

Shopping can sometimes feel confusing, especially when you have questions about shipping or taxes. Standard help pages are often hard to find. However, generative ai adds a smart assistant to the page to guide you. This bot answers your questions in seconds. Because the bot knows your cart, it gives perfect advice. This builds trust and keeps you moving forward. In addition, it makes sure you never feel alone while shopping.

Moreover, these bots can offer special deals at the perfect moment. If you hesitate, the generative ai might give you a small discount to help you decide. As a result, shoppers feel valued and safe. It is not just a tool; it is a digital guide. Because of these benefits, top brands are moving to AI today. Therefore, the checkout flow becomes a conversation instead of a form.

Safer and Faster Payments

Security is the most important part of any sale because hackers are always looking for ways to steal data. Luckily, generative ai is great at spotting fraud by looking at millions of data points in real-time. If it sees something odd, it stops the threat fast. This keeps your money and data very safe. Because the generative ai is so smart, it rarely blocks real customers. Thus, it makes payment security much stronger for everyone.

Additionally, it helps with filling out forms by guessing your address with high accuracy. This reduces errors and saves time for the customer. When you use it, the checkout flow feels like magic. You just click and go. Therefore, the risk of a mistake is very low. This is the future of generative ai in the payment world. Finally, this technology ensures that safety does not come at the cost of speed.

The Big Future of Generative AI

We are only at the start of this change. Soon, every store will use generative ai to talk to us. It will know our size, our style, and our budget. This means we will see fewer ads we do not like. Instead, we get a tailored world of products. It makes every transaction feel human. It is the best way to shop in 2026. If you want to stay ahead, you must use generative ai now. In conclusion, the personalized payment journey is the new standard for global trade.

Frequently Asked Questions

1. Is generative ai safe for my credit card?

Yes, it improves security by spotting fraud much faster than older systems.

2. Does generative ai make my phone slow?

No, most of the work happens on fast servers, so your phone stays quick.

3. Why do stores need generative ai?

It helps them sell more by making the checkout process easy and personal for everyone.

4. Can generative ai help with returns?

Yes, it can guide you through the return process and answer policy questions instantly.

5. Will all stores use generative ai soon?

Yes, it is becoming the global standard for all top e-commerce websites.

The world of global commerce is moving at a very fast pace today. Modern firms must look toward a smart and flexible leader to stay ahead. Specifically, a trade agreement like RCEP now changes how money moves across borders. This shift offers a clear map for success and a very professional way to work. Therefore, knowing how a trade agreement affects your digital growth is a vital step for your firm. This move is not just a trend for small teams. In fact, it is a very smart investment for any brand today. Consequently, a smart choice helps you build a future proof brand name. You will see a clear gain by following this powerful and strategic lead.

Breaking Down Barriers with a Regional Trade Agreement

Many firms find that turning a big plan into real work is very hard. However, a major trade agreement helps to bridge this gap between strategy and action. Traditional ways are often too expensive and slow for most small firms. Specifically, poor digital flow can hide many deep and dark costs of old manual habits. By following a solid trade agreement, countries agree to lower these hurdles. Furthermore, finding a top tool that works across many borders is rare. You also miss out on fast moves while your output stays low. Similarly, a unified trade agreement ensures your payment tech stays for the long term. This helps your growth move forward at a steady pace.

Setting a Gold Standard for Digital Payments

The journey to the top begins when you pick a dedicated tech partner. At this stage, you might wonder why a local pick often fails you globally. These new tools must act as your top guide on a steady basis. A trade agreement ensures your tech and its true worth match your global goals. They are built to spark fast progress in every single project. You should also know that an executive trade agreement offers more than a simple tax cut. While a solo human just finishes a task, these rules guide your whole path. Furthermore, they move firms past the fear of bad tech choices early. This approach starts very strong by setting a gold standard for all.

Scaling Fast with Unified Payment Rules

After you join the model, the goal shifts to gaining big wins. One of the top wins of expert help is getting dedicated guidance. The reality of a modern trade agreement then delivers a very custom plan for your firm. This path matches what you need and how you act every day. Therefore, if a project starts, you get fast and clear focus. You also gain access to a very diverse and deep skillset. This includes design, dev, and very deep digital security through smart systems. Access to these skills keeps all your users very happy and safe. It also shows you know your specific needs in a tough market.

How a Trade Agreement Drives Real Business Value

As a firm’s tech grows, a strategic lead helps you find new ways. At this stage, the focus on a trade agreement builds a very strong architecture. This plan is specific to what the modern user likes and wants. For example, some might get a faster way to find new items. The timing of these moves is very key for your success. Furthermore, the leader handles all your vendors and developers with ease. This ensures your project plan is solid from the very first step. Such smart timing helps firms move toward a big global win. Smart leaders push for more scale every single year for you. Indeed, the right trade agreement reveals who is truly ready.

Turning Insights into a Sustainable Content Edge

Data is the backbone of all smart marketing and content success today. The way you handle a trade agreement constantly tracks how every user acts with your tech. This includes how they read and share your posts or apps. These facts help refine the paths for every brand you lead. Therefore, the system learns and grows over time to serve you better. This data driven path ensures the best results for your firm. It also prevents any bad risks from hurting your brand name. Smart leadership relies on real facts to win every single time. Your plan and focus are too important to risk at any step. The core of your strategy is about long term brand health.

Joining Human Talent with Efficient Tech Systems

For the best results, smart tech joins your team in a seamless way. This link ensures all facts stay in one place for your team. Managers and teams share the same live info to move faster. This stops double work and missed ideas for new products or sales. The system provides a full view of every piece you need. Consequently, it supports personal touches at every single step of the way. Your strategy works best when you see a trade agreement joined with intelligent tools. It sets a strong base for your future success in any market. Thus, picking the right tech head is about building a real team.

Conclusion and the Path Forward for Your Firm

The future of your tech is too important to leave to chance. Today, you can gain a top expert view of how a trade agreement helps you without the huge cost. This smart move helps you scale faster and much smarter too. It turns your tech into a real win for your brand name. You will see more growth and less stress every single day. Therefore, you should act now to secure your spot in the market. Knowing the truth of quality leadership leads to true success. It is the best way to ensure your success for many years. You will find that the right leader makes all the difference.

FAQs

1What is the main goal of a trade agreement?

It helps countries trade more easily by cutting taxes and making rules the same.

2How does it help digital payments?

It creates a set of rules that lets apps and cards work in many countries at once.

3 Are these rules hard to follow?

No, they often make the work easier by giving you one clear path to follow.

4Does it help small firms?

Specifically, it helps small firms reach global buyers without high costs.

5 Why is this a smart move for my brand?

It builds a strong base for your future growth and keeps your brand safe.

Financial fragmentation now describes a world where the global economy splits into distinct regional or political blocs. This shift occurs because nations seek more control over their own money and security in a multipolar landscape. Therefore, you must understand how these changes will impact your business and your daily transactions. This guide explains the core challenges and the future of global payments.

The Rise of the Multipolar Economy

For many years, the world relied on a single financial system led by a few major powers. However, this centralized approach now faces competition from emerging economies and regional alliances. This shift creates a multipolar world where power is shared between several different global centers. Consequently, the standard rules for international finance are changing very quickly to match this new reality.

The move toward fragmentation happens because nations want to protect themselves from external financial pressure. For instance, some countries now build their own payment networks to avoid reliance on global systems like SWIFT. Because of this, we see a growing gap between different financial jurisdictions. I have noticed that this trend makes global trade much more complex for every person involved.

How Financial Fragmentation Impacts Global Payments

Fragmentation creates many small islands of finance instead of one connected global ocean. This separation means that moving money between two different blocs becomes much more difficult and expensive. For example, a business in one region might find that its payment software does not work in another region. Therefore, you must prepare for a future where global connectivity is no longer guaranteed.

You can expect to see higher fees for international transfers as systems become less compatible. Traditional cross-border payments already take a long time and require many middlemen. However, fragmentation adds even more layers of bureaucracy and compliance to every single transaction. In addition, businesses must now manage the risk of multiple currencies and varying local regulations.

The Role of Central Bank Digital Currencies

Many nations now explore Central Bank Digital Currencies (CBDCs) to modernize their local payment systems. These digital assets allow governments to track transactions more efficiently while reducing the cost of printing money. Furthermore, CBDCs can help a country settle international trades directly without using a global reserve currency. This technology is a primary tool for nations seeking financial independence in a multipolar world.

You should watch how these digital currencies interact with existing private payment networks. If two countries use different CBDC standards, they may still find it hard to trade with each other. Because of this, international organizations are working to create new rules for digital compatibility. However, the political friction of a multipolar world often makes these agreements very hard to reach.

Implications for Digital Payment Apps

Your favorite digital payment apps must now adapt to a landscape where cross-border rules change constantly. Some apps might choose to partner with local providers in every region to stay functional. Alternatively, others may focus only on one specific bloc to reduce their legal and technical risks. This fragmentation reduces the convenience that users have enjoyed for the last two decades.

In addition, users may need to carry multiple digital wallets to pay for goods in different countries. This shift reverses the trend toward a unified global marketplace where one app works everywhere. Therefore, you should look for payment solutions that offer wide compatibility and low conversion fees. Staying flexible will be your best strategy as the global system continues to split apart.

Risks to Global Financial Stability

Fragmentation creates a significant risk that the world will lose the ability to coordinate during a crisis. If every country follows its own rules, it becomes harder to stop a financial problem from spreading. For instance, a bank failure in one bloc might not be visible to regulators in another bloc. This lack of transparency makes the entire global economy much more vulnerable to sudden shocks.

Furthermore, the competition between different payment systems can lead to a “race to the bottom” in safety standards. Countries might lower their regulations to attract more business to their specific financial center. This behavior puts the security of your money at risk over the long term. Consequently, international cooperation remains vital even as political tensions continue to rise between nations.

The Future of Trade and Investment

Global trade will likely move toward “friend-shoring” where countries only trade with their political allies. This trend ensures that supply chains remain safe from geopolitical disruptions in distant regions. However, it also means that you may have fewer choices and higher prices for the goods you buy. Investment flows will also follow these political lines, creating two or more distinct economic zones.

You must rethink your investment strategy to account for these regional financial boundaries. For example, holding assets in only one bloc might leave you exposed if that region faces a downturn. Diversifying across different payment systems and jurisdictions is now a requirement for protecting your wealth. Therefore, staying informed about global shifts is the most important step you can take today.

Technical Standards and Interoperability

The primary technical challenge in a fragmented world is making sure different systems can still talk to each other. This is often called interoperability, and it is the key to keeping the global economy functional. If a payment message in Asia cannot be read by a bank in Europe, trade will stop. Engineers are now building bridges between different blockchain and digital currency protocols.

However, the political will to use these bridges is often lacking in a multipolar world. Some nations prefer “walled gardens” because they provide more control over their domestic data. Specifically, you should follow the development of international standards like ISO 20022. These common languages are the only things preventing a total breakdown of global financial communication.

Protecting Your Business From Financial Fragmentation

If you run a business that trades globally, you must audit your payment providers immediately. You should ensure that your primary bank has strong relationships in the regions where you operate. In addition, you may want to explore using stablecoins or other digital assets for fast cross-border settlements. These tools can bypass some of the friction caused by political fragmentation.

Gathering a diverse set of payment tools is the smartest way to manage these growing risks. If one system goes offline or becomes too expensive, you need an alternative ready to go. Take the time to understand the local payment habits of your international customers. Once you have a flexible system, you can grow your business despite the challenges of a multipolar world.

Conclusion and Next Steps

Financial fragmentation is a complex trend that will shape the next few decades of our lives. By focusing on the causes and the technical solutions, you can navigate this landscape successfully. The journey toward a more regional world requires patience and a high degree of adaptability from everyone.

If you want to stay ahead, you must monitor the news about CBDCs and regional trade blocs. Start by reviewing your current international payment methods to see where you are most vulnerable. Then look for new technologies that can bridge the gap between different financial zones. Your proactive approach will ensure that you remain connected to the global economy.

FAQs

1 What is financial fragmentation?

Financial fragmentation is the process where the global financial system splits into separate regional or political zones.

2 How does a multipolar world affect my payments?

It makes sending money across borders more expensive and complex as different regions use incompatible systems.

3 What are CBDCs?

Central Bank Digital Currencies are digital versions of a nation’s official currency issued and managed by the central bank.

4 Can AI help with financial fragmentation?

Yes, AI can help businesses manage the complex rules and multiple currencies found in a fragmented world.

5 What is interoperability in finance?

It is the ability of different financial systems and software to communicate and process transactions with each other.

India has seen a revolution in digital payments, mostly driven by platforms like UPI. While Tier-1 metros fully embrace this shift, true financial inclusion relies on deep penetration into the country’s heartland. Moving past the major urban centers reveals significant, unique regional challenges for digital payments. These challenges slow the journey toward a truly cashless economy. Understanding these obstacles is essential. This is crucial for policymakers and fintech companies. They want to unlock the vast potential of these emerging markets.

Infrastructure and Connectivity Deficits

One of the most persistent regional challenges for digital payments is the lack of robust infrastructure in smaller cities. Digital transactions rely entirely on uninterrupted power and consistent internet access. These are not always guaranteed outside of major cities. Frequent power outages interrupt transactions. This causes failures that quickly erode trust among merchants and consumers. Many smaller towns and remote areas suffer from poor quality internet. This low-quality service makes real-time payment applications slow. They can even be unusable during busy times. Improving this foundational digital infrastructure is a necessary first step. This step is vital for widespread digital adoption.

Low Digital and Financial Literacy

Technology adoption is only possible when users can operate it safely. In Tier-2 and Tier-3 cities, a widespread lack of digital and financial literacy remains a critical barrier. Many residents and small merchants are unfamiliar with digital payment interfaces. They are also unaware of necessary security measures. This knowledge gap creates two problems. First, there is a strong reluctance to adopt the systems. Second, there is an increased vulnerability to cyber fraud and scams. Most support materials are often only available in English. This language barrier complicates learning for a large group of people. Customized, local-language education is vital. It is needed for overcoming these regional challenges for digital payments.

Building Trust and Overcoming Security Fears

Trust is the most important currency in the financial ecosystem. Yet, it is hard to build trust in a complex, digital system. Concerns about security are high in smaller cities. News of online fraud spreads quickly here. This causes widespread skepticism. Users fear that errors will cause monetary loss. They worry the dispute resolution process will be too slow. Small merchants often prefer cash. They fear that digital records may increase their tax liabilities. Addressing these fears requires clear, simple dispute mechanisms. It also needs strict security frameworks. Awareness campaigns must focus on public reassurance.

The Merchant Adoption Hurdle

Consumers in Tier-2 and Tier-3 cities may be ready to pay digitally. However, small, fixed retail merchants may not be ready to accept it. This reluctance comes from several factors. Many merchants do not see enough customer demand. They do not want the initial effort of setup. They also avoid the minor costs of acquiring QR codes or POS terminals. Completing the necessary Know Your Customer (KYC) documents is often seen as tedious. It is also complex and time-consuming. Unless the merchant finds a clear, immediate business benefit, they often stick with cash. Incentives and simpler onboarding are needed. This must address these specific regional challenges for digital payments for businesses.

Socio-Cultural and Behavioral Inertia

Finally, deeply ingrained socio-cultural habits pose a formidable regional challenge for digital payments. In many smaller towns, cash-based transactions are a long-standing tradition. This supports close, community-based relationships. Digital transactions can feel impersonal. The human touch of handling cash is lost. This can discourage people from adopting the technology. Breaking this strong, old habit takes more than just making the technology available. It requires sustained, community-centric effort. This effort must use social norms to make digital payment the default. It must be the trusted and socially accepted way to transact for everyone.

Frequently Asked Questions (FAQs)

1 What is the primary infrastructure challenge in Tier-2 and Tier-3 cities for digital payments?

The main challenge is the inconsistent internet and poor power supply. This leads to transaction failures and quickly lowers user trust.

2 Why do merchants in smaller cities resist digital payments?

Merchants resist because they fear higher taxes, do not see enough customer demand, and find the KYC process too complex and time-consuming.

3 What is ‘digital literacy’ in the context of payments?

Digital literacy is the user’s ability to use payment apps safely. This includes spotting fraud and knowing how to resolve transaction disputes quickly and easily.

4 How does the language barrier affect adoption in these regions?

Most security warnings and instructions are often only in English. This makes it difficult for many local residents to understand the system and use it with full confidence.

5 What is a key non-technical factor slowing down digital payment growth in Tier-3 cities?

A major factor is the strong, traditional habit of using cash. This habit is deeply trusted, which makes the shift to abstract digital money slow and challenging for communities.

The world of digital payments is constantly evolving. Every year brings new technologies, new consumer habits, and, crucially, new regulations. For businesses, understanding these changes is not just important; it is essential for managing costs and maintaining profitability. Specifically, the Merchant Discount Rate (MDR) has always been a critical factor in the cost of accepting digital payments. This fee directly impacts a merchant’s bottom line. Recently, 2025 brought about significant shifts in both MDR structures and the landscape of “Zero MDR” policies. These changes have reshaped how merchants, payment processors, and even customers interact with digital transactions. Today, we will break down what exactly changed and what it means for your business.

Understanding the Merchant Discount Rate (MDR)

Before discussing the changes, we should revisit what MDR actually is. The Merchant Discount Rate is the fee charged to a merchant by their bank or payment service provider for processing customer payments made through debit cards, credit cards, or other digital methods. This fee is usually a percentage of the transaction value. Additionally, it often includes a small fixed per-transaction fee. The MDR is not a single fee; instead, it is typically a blend of three main components:

Interchange Fee: This is the largest component, paid by the acquiring bank (merchant’s bank) to the issuing bank (customer’s bank).

Scheme Fee: This fee is paid to the card networks (like Visa or Mastercard) for using their infrastructure.

Acquirer Markup: This is the fee charged by the merchant’s bank or payment processor for their services.

Therefore, understanding these components is crucial to grasping why changes to MDR policies have such a wide-reaching impact on businesses.

The Rise and Fall of Zero MDR Policies

The concept of “Zero MDR” gained significant attention in previous years, especially in markets aiming to boost digital payments. Specifically, a Zero MDR policy meant that merchants would not be charged any fees for processing payments through certain digital channels, particularly debit card or UPI transactions. The government or regulatory bodies often absorbed these costs.

Consequently, the goal was to incentivize merchants to adopt digital payment methods, thereby promoting a cashless economy. While beneficial for merchants in the short term, this policy put immense pressure on payment service providers and banks. Therefore, maintaining the underlying infrastructure and services without a direct revenue stream became unsustainable. These pressures naturally led to policy re-evaluations, culminating in the significant shifts seen in 2025 regarding MDR.

Key Changes to MDR Policies in 2025

The year 2025 brought a series of calculated adjustments to MDR policies, moving away from a blanket Zero MDR approach in many regions. Specifically, these changes typically included:

Tiered MDR Structures: Many regions reintroduced or refined tiered MDR structures. These structures differentiate fees based on transaction value, merchant type (e.g., small business vs. large enterprise), and the payment method used (e.g., credit card, debit card, QR code). Therefore, this aims for a fairer distribution of costs.

Revised Interchange Caps: Governments and regulatory bodies often reviewed and adjusted interchange fees. This component of the MDR is a major driver of overall cost. New caps might aim to reduce overall costs for merchants while still allowing issuing banks to recover some operational expenses.

Emphasis on Digital Infrastructure Costs: The new policies often acknowledge the increasing investment required for secure digital payment infrastructure. Therefore, the revised MDR structures now attempt to ensure payment processors and banks can cover these operational and technological costs.

These changes reflect a balancing act: promoting digital payments while ensuring the sustainability of the payment ecosystem, affecting every aspect of MDR.

Impact on Merchants: Navigating New Costs

For merchants, the changes to MDR policies in 2025 mean a direct reassessment of their payment processing costs. Businesses that previously benefited from Zero MDR policies now face new fees for certain transactions. Therefore, this requires a careful review of their pricing strategies. Small and medium-sized enterprises (SMEs) are particularly affected, as even minor increases in transaction costs can significantly impact their margins. Consequently, merchants must:

Review Payment Mix: Analyze which payment methods their customers use most frequently and understand the associated new MDRs.

Negotiate with Providers: Engage with their payment service providers to understand the updated fee structures and potentially negotiate better rates based on their transaction volume.

Explore Cost-Saving Measures: Consider implementing technologies that optimize payment routing or reduce chargebacks, which indirectly lowers overall payment costs.

Ultimately, proactive management of these new MDR costs is crucial for maintaining profitability in the digital age.

Impact on Payment Service Providers and Banks

The shifts in MDR policies in 2025 have profound implications for payment service providers (PSPs) and banks. For these entities, the reintroduction or adjustment of MDR fees often means a return to a more sustainable revenue model. Previously, Zero MDR policies strained their ability to invest in technology, security, and customer service. Therefore, the new policies generally aim to provide a more predictable revenue stream. Consequently, PSPs and banks can now:

Invest in Innovation: Allocate more resources to developing advanced payment technologies, enhancing security features, and improving user experience.

Expand Digital Infrastructure: Further build out the networks and systems necessary to support a growing volume of digital transactions.

Offer Differentiated Services: Compete on value-added services rather than just trying to absorb costs, which benefits merchants with more choices.

However, they must also effectively communicate these changes to merchants and offer competitive pricing, especially concerning MDR.

The Broader Economic Context and Digital Adoption

The 2025 changes to MDR policies are not isolated; instead, they reflect broader economic trends and the maturing of digital payment ecosystems. As more economies transition towards digital transactions, the initial incentives like Zero MDR become less necessary. The focus shifts to building a self-sustaining and robust payment infrastructure. Therefore, these policy adjustments indicate a move towards greater market efficiency. They ensure that all participants—merchants, consumers, and payment providers—contribute to the cost of maintaining a secure and efficient digital payment network. Consequently, while some merchants may see increased costs, the long-term goal is a more stable and innovative digital payment landscape, driven by fair MDR structures.

Conclusion

The year 2025 marked a pivotal moment in the evolution of MDR and Zero MDR policies, fundamentally altering the economics of digital payments. While the departure from universal Zero MDR might initially present challenges for some merchants, these changes are generally aimed at fostering a more sustainable and equitable digital payment ecosystem. Therefore, businesses must thoroughly understand these new MDR structures. They must also proactively adapt their strategies to manage costs effectively. Ultimately, the ongoing evolution of payment regulations, including adjustments to the Merchant Discount Rate, is a constant reminder that staying informed and agile is paramount for success in the ever-changing digital economy.

Frequently Asked Questions (FAQs)

1. What is the Merchant Discount Rate (MDR)?

The MDR is the fee charged to a merchant by their bank or payment service provider for processing customer payments made through digital methods like debit or credit cards. It is typically a percentage of the transaction value and includes components like interchange fees and scheme fees.

2. Why did “Zero MDR” policies change in 2025?

Zero MDR policies often proved unsustainable for payment service providers and banks, as they absorbed the costs of processing transactions and maintaining infrastructure without direct revenue. The changes in 2025 generally reflect a move towards fairer cost distribution to ensure the long-term viability and innovation of the digital payment ecosystem.

3. What are “tiered MDR structures”?

Tiered MDR structures are new or refined fee models that charge different rates based on factors like transaction value, the type of merchant (e.g., small business vs. large corporate), and the specific payment instrument used (e.g., credit card, debit card, UPI). This aims for a more nuanced and equitable fee system.

4. How do the 2025 MDR changes impact small businesses?

Small businesses that previously benefited from Zero MDR for certain transactions might now face new or increased fees. This requires them to carefully review their payment mix and potentially negotiate new terms with their payment providers to manage these updated costs and maintain profit margins.

5. How can merchants prepare for and manage new MDR costs?

Merchants can prepare by reviewing their current payment processing statements, understanding the new MDR breakdown for different transaction types, and engaging with their payment service providers. They should also explore options for optimizing their payment mix and potentially leveraging new technologies to reduce overall payment-related expenses.

The evolution of India’s payment ecosystem is marked by fast innovation. The launch of the Unified Payments Interface (UPI) was a landmark event. Now, the landscape for businesses is changing dramatically with the expansion of UPI 2.0 features and the global reach of UPI Global. It is vital for companies to understand these shifts. They must prepare to utilize the full power of this payments system. The ongoing evolution of UPI is cementing its place as one of the world’s most innovative payment platforms. It is succeeding both domestically and internationally.

UPI 2.0: Deepening the Domestic Digital Experience

The first version of UPI focused on speed and convenience. It made payments instant and interoperable. Then, UPI 2.0 launched with more powerful tools for both consumers and businesses. It especially supported higher-value transactions and complex financial commitments. These advanced features streamline operations effectively. Furthermore, they foster greater financial inclusion in the domestic market. Businesses must integrate these features quickly to stay ahead of their competition. The new features help manage money better.

Key Features of UPI 2.0 and How They Help

A very significant feature is the One-Time Mandate. This lets a customer pre-authorize a future payment. The funds are blocked in their account and then debited on a specific future date or upon delivery. Consequently, this feature is perfect for e-commerce. Payment can be mandated when the order is placed but deducted only when the product ships. Another important change is the ability to link Overdraft Accounts to a UPI ID. This grants customers a short-term line of credit for their transactions. Therefore, payments to businesses are less likely to fail because of insufficient account balance. This ensures smoother transactions for everyone.

Moreover, UPI 2.0 introduced the Invoice in the Inbox feature. This allows the customer to view a detailed digital invoice right along with the collect request in their payment app. This increases transaction transparency and builds trust. Security can be enhanced further. You can integrate Signed Intent and QR Codes. These codes verify the authenticity of both the merchant and the transaction securely. Ultimately, these UPI 2.0 features simplify all transactions for individuals and businesses. They combine convenience with robust safety for all users. Businesses must train their teams to use these new tools.

The Global Game-Changer: Preparing for UPI Global

While UPI 2.0 focused on enhancing the domestic experience, UPI Global is about expanding the system’s success onto the world stage. NPCI International Payments Limited (NIPL) is actively forging partnerships with various countries and payment networks. Their goal is to enable seamless, real-time cross-border transactions. This expansion often happens by linking UPI with a foreign country’s fast payment system, like PayNow in Singapore. For this reason, it fundamentally changes how international commerce is conducted today.

The Impact of Cross-Border UPI Transactions

The main benefit of UPI Global is the drastic reduction in the friction and cost of cross-border payments. Traditional international transfers, which often rely on slow, expensive intermediary banks, now face a real challenger. Consequently, this opens up massive opportunities for all businesses. This is especially true for MSMEs that previously found international expansion too complex or costly. Furthermore, this is particularly impactful for the remittance market. It allows Indian expatriates to send money home instantly and cheaply.

For e-commerce, the potential of UPI Global is truly enormous. International merchants can easily cater to the vast Indian consumer base. Also, Indian businesses can sell globally without complicated payment gateways. Therefore, businesses must prepare for these changes. They should ensure their payment processing systems can handle foreign exchange conversions and cross-border settlement with ease. This global reach, however, requires a new mindset for Indian businesses looking to expand their market footprint quickly.

Key Countries Adopting UPI Global

UPI Global has already made significant strides in several key markets. Singapore, for example, linked its PayNow system with UPI. This created a seamless channel for instant cross-border transfers between the two nations. Similarly, countries like the UAE, France (for tourist payments), Nepal, and Bhutan have adopted or are piloting UPI integration. Thus, these countries become much more accessible markets for Indian businesses. Businesses should prioritize technical integration with these countries first. Furthermore, they should closely monitor new partnership announcements by NIPL. This will help them identify the next big market opportunity quickly.

Business Strategy: Integrating the New UPI Ecosystem

To truly maximize the benefits of these advancements, businesses must develop a clear strategic roadmap. This roadmap should focus on integrating UPI 2.0 and preparing for UPI Global. Merely accepting UPI payments is no longer enough for growth. Active integration of its newest features is essential for optimizing cash flow, enhancing customer experience, and improving security across the board.

1. Optimize for UPI 2.0 Features for Better Cash Flow

First of all, integrate the One-Time Mandate feature for any subscription, installment, or post-delivery payment models your business uses. This feature dramatically improves payment success rates. It also provides predictable revenue streams, which is great for planning. Second, leverage the Invoice in the Inbox feature to provide rich context for every single transaction. This simple step builds customer trust effectively. Also, it significantly reduces payment-related queries or disputes for your support team. Finally, you can ensure security and customer confidence. You can do this by mandating the use of Signed QR codes at your Point of Sale (POS) terminals. This proactive step helps your business remain competitive by embracing the latest domestic payment technology.

2. Prepare for Seamless UPI Global Adoption

Businesses that deal with international customers or suppliers should immediately start planning for UPI Global. This preparation involves two main areas: technical preparedness and operational readiness. Technically, you should partner with a payment gateway that supports UPI‘s cross-border linkages. This gateway should also manage multiple currencies and Foreign Exchange (FX) rates in real-time. Operationally, you must update your accounting and reconciliation systems. They need to handle the increased volume of international, real-time transactions. This adoption is a critical step for any business with serious international ambitions for the future.

3. Focus on Seamless Reconciliation and Audit Trails

The real-time nature of UPI can sometimes complicate traditional accounting practices. Therefore, the implementation of robust, automated reconciliation systems is completely non-negotiable for serious businesses. Manual reconciliation of thousands of small, instant transactions is highly inefficient. It is also very prone to errors. By investing in technology that seamlessly matches UPI transaction data with sales and inventory data, your business gains superior visibility and control over its cash flow. This operational efficiency is the true long-term benefit of mastering the entire UPI ecosystem correctly. It saves time and money for the accounting department.

Overcoming Potential Challenges in the New UPI Era

While the rise of UPI is exciting, businesses must be aware of certain operational and security challenges. They can overcome these challenges with careful planning and smart technology investments.

Managing High Transaction Volumes

The sheer volume of UPI transactions is constantly growing. This places high demands on a business’s IT infrastructure. Businesses must make sure their payment gateways and server capacity can handle peak transaction loads. Furthermore, robust backup systems must be in place to prevent service interruptions. You can maintain reliable payment processing by scaling your infrastructure properly. In turn, this keeps customers happy and transactions flowing smoothly every time.

Security and Fraud Mitigation

The security features in UPI 2.0, like Signed QR, are powerful tools. However, businesses must remain vigilant against fraud. This involves training staff to recognize social engineering tactics. It also means educating customers about transaction security best practices. Since transactions are instant, recovery from fraud is difficult. Therefore, your business should invest in advanced fraud detection algorithms. These algorithms can analyze transaction patterns in real-time. This helps stop fraudulent activities before they can cause financial loss to your business.

Regulatory Compliance Across Borders

The expansion of UPI Global means dealing with multiple international regulations. This includes local Anti-Money Laundering (AML) and Know Your Customer (KYC) laws. Furthermore, data privacy laws vary significantly from country to country. Your business must ensure that its data handling and compliance procedures meet the requirements of every jurisdiction where you use UPI Global. Since regulations change frequently, you should consult with legal and compliance experts regularly. This essential step prevents costly legal issues down the road.

Conclusion: The Future is Real-Time and Global with UPI

The combination of UPI 2.0’s enhanced features and the expansive vision of UPI Global signals a future where digital payments are not just convenient. They are also powerful strategic tools for commerce. Businesses that embrace the One-Time Mandate, leverage the transparent invoicing features, and strategically prepare for cross-border payment flows will be perfectly positioned for impressive growth. The time to upgrade and strategize is definitely now. You can ensure your business thrives in this real-time, global payments era by taking action today. The ongoing success of UPI is a clear signal that the future of finance is open, fast, and highly inclusive for everyone.

FAQs About UPI 2.0 and UPI Global

1. How does the One-Time Mandate in UPI 2.0 benefit subscription-based businesses?

The One-Time Mandate allows a customer to pre-authorize a recurring or future payment. For subscription businesses, this secures the commitment from the customer upfront. This reduces failed payments significantly and improves predictable revenue. The money is blocked and debited automatically on the due date.

2. What security features were enhanced in UPI 2.0 for merchants?

UPI 2.0 introduced Signed Intent and QR Codes. These codes digitally sign the transaction, verifying the authenticity of the merchant to the customer’s payment app. This enhanced security measure minimizes the risk of fraudulent QR codes. It successfully builds greater trust in the payment process for all users.

3. What is the biggest advantage of UPI Global for small e-commerce businesses?

The biggest advantage is the ease of cross-border commerce. UPI Global significantly reduces the cost and complexity of accepting payments from international customers in countries like Singapore or the UAE. This allows small e-commerce businesses to easily access a much larger, global customer base for faster growth.

4. How will UPI Global affect Indian businesses with international suppliers?

UPI Global will enable much faster and cheaper payments to international suppliers in countries where UPI has established linkages. Consequently, this will significantly reduce transaction fees and settlement times. These reductions are compared to traditional banking channels. It greatly improves the business’s overall supply chain efficiency.

5. What is the immediate first step a business should take to prepare for UPI 2.0’s benefits?

The immediate first step is to work with your bank or Payment Service Provider (PSP) right away. You must ensure your payment integration supports the new UPI 2.0 APIs. This is especially important for the One-Time Mandate feature if your business model involves future or recurring payments to customers.