The world is moving toward digital money, but many rural areas still lack fast internet. This creates a big gap for people who want to shop and sell goods. However, new technology is now allowing payments to happen without any data connection. This shift is vital for rural commerce to grow and thrive in 2026. Because these tools are simple and fast, they bring the power of modern trade to everyone. In short, the future of global payments is becoming inclusive and offline.

Why Internet Gaps Slow Down Trade

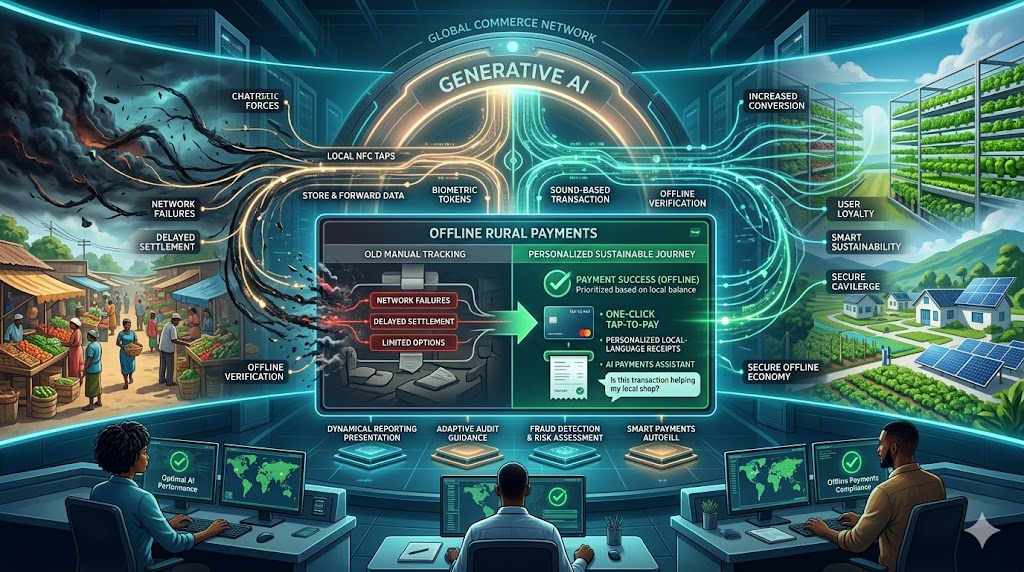

In many villages, a weak signal can stop a sale in its tracks. Traditional apps often spin and fail when the network is poor. Consequently, many shopkeepers still prefer cash because it never fails. This is because standard payments rely on a constant link to a central bank. Furthermore, customers feel frustrated when they cannot finish a purchase. Therefore, rural markets need a different kind of system to handle their daily payments smoothly.

Another issue is the high cost of data for small transactions. For instance, a farmer might only want to buy a small bag of seeds. If the digital process is too hard, they will stick to physical coins. Thus, the industry is building tools that work over basic radio waves or sound. A smart payments strategy solves this by removing the need for a smartphone. This keeps the local economy moving even in the most remote locations.

Solutions for the Offline Economy

Store-and-forward tech is a vital tool for rural success. This allows a device to collect payments while offline and sync them later when a signal is found. Because this removes the wait time, it builds instant trust between the buyer and the seller. Furthermore, sound-based tech can send encrypted data through a basic phone speaker. This means you can finish your payments just by holding your phone near a small box. In short, commerce wins when the tech fits the environment.

Near-field communication (NFC) cards are also growing fast in rural zones. Instead of a complex app, users just tap a simple plastic card on a merchant’s device. Because these payments are verified locally, they happen in less than a second. Therefore, experts are building low-power networks to support these taps across whole villages. This ensures that the flow of money never stops, even during a power cut. Finally, these offline solutions ensure that digital trade is a real choice for every citizen.

Staying Safe Without the Cloud

Security is the most important part of any offline sale. People often worry if their money is safe when there is no live internet link. Luckily, new AI tools use secure hardware chips to lock every transaction. If someone tries to change the data, the chip stops the process fast. This keeps your payments and your personal balance very safe. Because the tech is so robust, it prevents double-spending without needing a server. Thus, the system stays strong and secure for every rural user.

Additionally, biometric tokens help verify identity without making the process slow. It uses a fingerprint on the card itself to prove you are the owner. When you use these tools, the checkout flow feels very smooth and private. You just tap and go. Therefore, the risk of a mistake or theft is very low. This is the future of payments in a truly connected world. Finally, safety ensures that rural families feel comfortable moving away from cash for good.

The Big Future of Inclusive Trade

We are only at the start of a massive offline shift. Soon, every small stall in the woods or mountains will accept digital money. This means we will see a huge boost in local wealth and savings. Instead of a hard process, we get a tailored world of easy trade for all. Sustainable payments make every transaction feel like a step toward a better life. It is the best way to shop in 2026. If you want to stay ahead, you must use these offline tools now. In conclusion, rural commerce is finally finding its digital voice.

Frequently Asked Questions

1. Can I really pay without any internet?

Yes, new sound-based and NFC tools allow you to finish a sale without a data link.

2. Is my balance updated instantly?

Your local balance is updated on your device, and it syncs with the bank once you find a signal.

3. Do I need an expensive phone for this?

No, many offline systems work with basic feature phones or simple tap-cards.

4. How does the shopkeeper get the money?

The merchant’s device stores the data and clears the funds when they connect to a network later.

5. Is it safer than carrying cash?

Yes, because the digital tokens are encrypted and can only be used with your fingerprint or PIN.

Read More:

Building a Better finance Future with ESG Standards