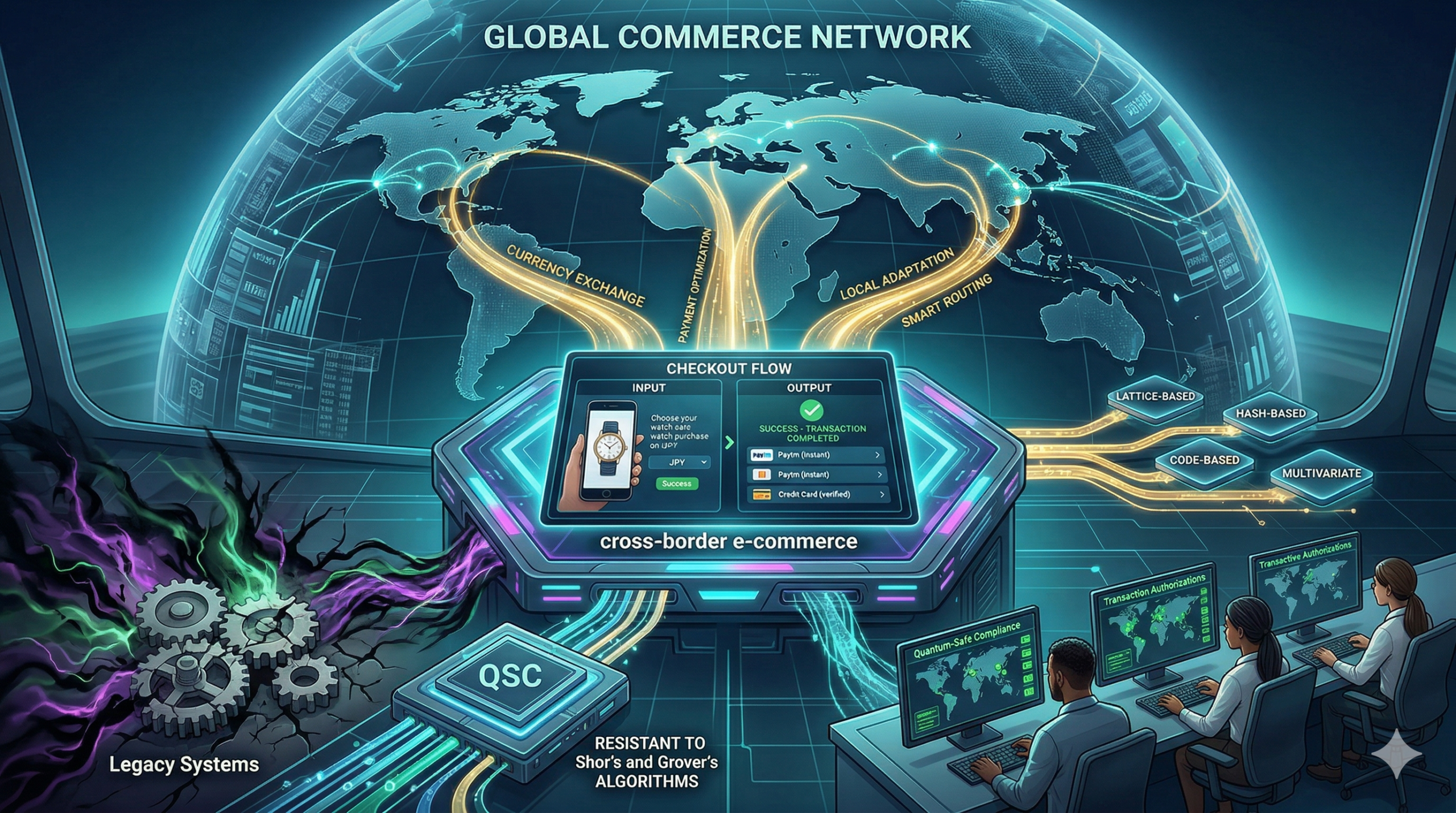

Global trade is moving faster than ever before. Most online stores now look for customers in every corner of the world. However, selling across borders brings many difficult hurdles. This is because every country has its own rules and preferred ways to pay. Therefore, businesses must find smart ways to handle these gaps. If they fail, they risk losing sales and trust. Successful e-commerce depends on a smooth and safe payment journey for everyone.

The Big Problems for Global Sellers

High fees are a major enemy of global growth. When a customer buys something from another country, banks often take a large cut. Consequently, the final price becomes too high for the shopper. This is because currency exchange rates are often unfair. Furthermore, hidden costs can surprise the customer at the final step. This leads to cart abandonment. Therefore, e-commerce firms must be very clear about all costs from the start.

Another big issue is the variety of payment habits. For instance, shoppers in Europe might prefer digital wallets. Meanwhile, customers in Asia might use QR codes or local bank transfers. If a store only offers credit cards, it will fail in these regions. Thus, a one-size-fits-all plan does not work. Every e-commerce site needs to adapt to local tastes to stay ahead.

Solutions for a Better Payment Journey

Multi-currency pricing is a vital tool for success. Customers want to see prices in their own money. Because this removes confusion, it builds instant trust. Furthermore, using a local acquiring bank can reduce transaction fees. This means the store keeps more profit while the user pays less. In short, e-commerce wins when the math is simple for the buyer.

Smart routing is another great way to fix failures. Sometimes, a bank might block a foreign payment by mistake. However, modern systems can instantly try a different bank to finish the sale. This keeps the flow moving without any delay. Because the user does not see the struggle, the experience feels like magic. Therefore, e-commerce platforms must use these intelligent tools to prevent lost sales.

Staying Safe Against Global Fraud

Security is the most important part of any global sale. Hackers are always looking for ways to steal data across borders. Luckily, new AI tools are great at spotting fraud by looking at millions of data points. If a transaction looks odd, the system stops it fast. This keeps your money and data very safe. Because the AI is so smart, it rarely blocks real customers. Thus, e-commerce stays strong and secure for everyone.

Additionally, 3D Secure 2.0 helps verify identity without making the process slow. It uses data to prove the user is real in the background. When you use these tools, the checkout flow feels very smooth. You just click and go. Therefore, the risk of a mistake or theft is very low. This is the future of e-commerce in a connected world. Finally, safety ensures that your brand grows a good name worldwide.

The Future of Global Trade

We are only at the start of a massive shift. Soon, every store will use local solutions to talk to global fans. This means we will see faster shipping and lower fees for everyone. Instead of a hard process, we get a tailored world of products. E-commerce makes every global transaction feel like a local one. It is the best way to trade in 2026. If you want to stay ahead, you must use these solutions now. In conclusion, a better payment journey is the key to global success.

Frequently Asked Questions

1. Why do global payments often fail?

They fail because banks might flag foreign cards as high-risk or due to technical errors in legacy systems.

2. How can I reduce currency exchange fees?

You should use a local payment provider or an e-wallet that offers better rates than traditional banks.

3. What is the best payment method for Asia?

Local digital wallets and QR-based systems are the most popular choices for shoppers in that region.

4. Does 3D Secure slow down my checkout?

No, the 2.0 version is much faster and often works in the background without bothering the user.

5. Is it hard to set up multi-currency pricing?

Most modern payment gateways offer this feature as a simple setting you can turn on.

The rapid development of quantum computers creates a massive risk for global finance. Currently, most banks use encryption like RSA, which relies on math that is too hard for normal computers to solve. However, a quantum machine can crack these codes in just minutes. This is why we must adopt quantum-safe cryptography to protect payment security before these machines become common. Because the entire digital economy relies on trust, a single breach could cause a global collapse. Therefore, the race to secure our financial data is already moving at full speed.

The Rising Threat to Digital Money

A quantum computer does not work like a laptop. It uses qubits, which allow it to try millions of paths at the exact same time. This speed means that hackers could soon bypass the walls that keep our money safe. If we do not upgrade our systems, payment security will become a thing of the past. The threat is not just in the future; it is happening now through “harvesting” attacks.

Criminals are currently stealing locked data with the plan to open it later. They know that once they have a quantum machine, they can unlock years of old bank records. Consequently, we cannot wait for the technology to arrive. We must strengthen payment security today to prevent these future leaks. This proactive shift is the only way to maintain long-term consumer confidence.

What is Quantum-Safe Technology?

Quantum-safe math is designed to be so complex that even a quantum brain cannot find the answer. It uses different geometric and algebraic structures that do not have “shortcuts” for quantum algorithms. By moving to these new methods, we ensure that payment security remains intact for decades to come.

There are three main types of math that experts are testing right now:

Lattice-based Math: This hides data in a massive, multi-dimensional grid of points.

Code-based Math: This uses the science of error-correction to scramble and lock sensitive files.

Hash-based Signatures: This creates a digital “fingerprint” that is almost impossible to replicate or forge.

Building a Resilient Financial Future

The move to new standards is a major task for the world’s banks. It requires a concept called “crypto-agility.” This allows a bank to update its code without needing to rebuild its entire software suite. When a system is agile, it can adopt new payment security tools as soon as they are ready. This flexibility is vital because the hackers will never stop looking for new ways to get in.

Furthermore, global groups like NIST are already picking the best math to use. Banks must follow these standards to ensure they can talk to each other safely. If one bank uses old math while another uses new math, the system breaks. Thus, unity in payment security is just as important as the technology itself. We must work together to build a wall that no computer can climb.

Conclusion

The future of our economy depends on how we handle the quantum threat. By focusing on payment security now, we can stop the “cryptographic apocalypse” before it starts. It is a slow and difficult journey, but it is necessary for a safe digital world. Companies that lead this change will be the ones that people trust with their money. Ultimately, payment security is the foundation upon which the next century of trade will be built.

Frequently Asked Questions

1. Is my bank account at risk right now?

No, powerful quantum computers do not exist yet. However, we need to upgrade now to stay safe in the future.

2. What does “Harvest Now, Decrypt Later” mean?

It means hackers steal your locked data today so they can open it in a few years with a quantum machine.

3. Will new security make my payments slower?

Some new math is slower, but experts are picking the fastest ones to keep your experience smooth.

4. Can a normal computer run quantum-safe security?

Yes, these new rules are designed to run on the phones and laptops we use today.

5. How does this affect global payment security standards?

It forces every bank to move to a new, shared language of math that quantum machines cannot understand.

In the high stakes world of global trade, money is now a silent weapon. Specifically, many nations now realize that controlling how funds move is a vital edge. Therefore, building a solid payment infrastructure has become a key tool of soft power. This shift changes how countries talk and trade with each other. It is not just about digital coins or bank apps. In fact, it is a smart way for a country to lead on the global stage. Consequently, a strong and stable payment infrastructure helps a nation project its true strength. You will see a clear shift in power by following this deep and strategic trend.

Winning the Trade War Without a Single Shot

Many people think trade wars are only about high taxes and ships. However, the real fight often happens in the wires and code of a bank. First, a local payment infrastructure can bypass old global rules that slow down growth. Specifically, it lets a country keep its trade moving even when others try to block it. Furthermore, having a top tool that others want to use creates a new kind of bond. You also gain a lead when your neighbors rely on your tech to buy bread. Similarly, a unified payment infrastructure ensures your trade stays safe during a crisis. This puts your growth on a steady path for a very long time.

Why Every Nation Wants Their Own Money Rules

The journey to the top begins when a nation builds its own money path. At this stage, relying on a foreign payment infrastructure is a very big risk. These new tools act as a top guide for a country’s financial future. Specifically, a custom payment infrastructure ensures that a nation and its true worth stay safe. It is built to spark fast progress in every single trade deal. You should also know that a smart system offers more than just a way to pay. While a simple app just sends cash, a whole payment infrastructure guides the whole economy. Furthermore, it moves firms past the fear of being cut off from the world.

The True Influence of Digital Dollar and Yuan

As a nation’s tech grows, its influence spreads to other places. At this stage, the focus on a payment infrastructure builds a very strong bond with allies. This plan is specific to what a partner country likes and needs. For example, some might get a faster way to sell their goods abroad. The timing of these moves is very key for global success. Furthermore, a top leader handles all the tech and rules with ease. This ensures your trade plan is solid from the very first step. Such smart timing helps a country move toward a big global win. Indeed, a modern payment infrastructure reveals who is truly in charge today.

Protecting the Flow of Goods and Services

Data is the backbone of all smart trade and money success today. The way a country handles its payment infrastructure tracks how every dollar moves. This includes how users buy and sell items in a safe way. These facts help refine the path for every brand and firm in the land. Therefore, the system learns and grows over time to serve the people better. This data driven path ensures the best results for a whole nation. It also prevents any bad risks from hurting the economy. A smart payment infrastructure relies on real facts to win every single time. Your plan and focus are too important to risk at any step.

Conclusion and the New Map of World Trade

The future of global trade is too important to leave in the hands of others. Today, we see how a modern payment infrastructure changes who wins and who loses. This smart move helps a nation scale faster and stay much safer too. It turns simple tech into a real win for a whole region. You will see more growth and less stress for firms everywhere. Therefore, nations act now to secure their spot in the global market. Knowing the truth of quality tech lead leads to true success. It is the best way to ensure a bright future for many years. You will find that the right payment infrastructure makes all the difference in a trade war.

FAQs

1 How is a payment system a tool of power?

It lets a country control how money flows, which can help or hurt other nations.

2 Does this affect small businesses?

Yes, it makes it easier or harder for them to sell items to other countries.

3 Why is it called soft power?

Because it uses tech and money to lead rather than using a real army.

4 Is it safe for a country to use its own system?

Specifically, it is much safer because it stops other nations from blocking their trade.

5 Will this trend grow in the future?

Indeed, more nations are building their own tools to stay independent and strong.

You must understand the new ways the world moves money today. Therefore, you should learn about the battle between SWIFT, CIPS, and UPI. Truly, the old ways of sending cash across borders are changing very fast. Consequently, you can stay ahead by knowing which system works best for your global trade.

Many people think that all international bank transfers are exactly the same. But, the reality is that each system has its own rules and goals in 2026. Always remember, a fast payment system is a strong signal for any search engine. This ensures that your brand stays reliable and your global partners stay happy. This approach requires you to look at speed, cost, and political safety. It helps you build a much more resilient financial plan for the long term. It makes your daily international sales feel much more secure and very effective.

Phase 1: The Global Standard of SWIFT

First, you must look at SWIFT because it is the biggest network today. Why has it been the leader of global finance for so many decades? Clearly, it connects over 11,000 banks in almost every country on earth. Therefore, most businesses still rely on it for large, secure transfers every day.

Why SWIFT Stays at the Top of Finance

Here are several reasons why SWIFT remains a powerhouse in 2026:

Massive Reach: You can send money to almost any corner of the globe.

High Security: It uses the best tech to keep your data and cash very safe.

New Speed: The gpi system now makes many transfers happen in minutes.

Global Trust: Banks everywhere know and use this system without any doubt.

Shared Standards: It uses a common language that all bank systems understand.

Transparency: You can track your money like a package in the mail today.

Search Engine Data: Stable SWIFT flows help your business earn trust scores.

Truly, SWIFT is a very solid choice for most of your corporate needs. But, you must also consider the fees and the time it takes to clear. This keeps your costs in check and prevents any delays in your supply chain. It creates a very professional and high standard for your global trade.

Phase 2: The Rising Power of CIPS in China

So, what happens when a nation wants its own way to move money? Truly, China created CIPS to help the yuan become a global currency fast. Consequently, you should watch this system if you do a lot of business in Asia. It acts as an alternative path that does not always rely on Western banks.

How CIPS Changes the Payment Game

Here is how CIPS works differently from the old systems:

Direct Yuan Trade: It allows you to pay for goods in yuan without a middle step.

Fast Clearing: It offers real-time settlement for many types of trade deals.

Extended Hours: It stays open longer to match the working day in many zones.

Lower Costs: Using CIPS can be cheaper for firms that trade with China today.

Independent Path: It provides a safety net if other networks face political noise.

Direct Access: More banks in Europe and Africa are joining the system right now.

Trust Levels: Using local systems improves your search engine authority in Asia.

Furthermore, this improves your search engine performance by showing your reach in the East. It makes your company look very modern and ready for 2026 global shifts. This ensures that you have a backup plan for your most important trade routes. It creates a very fast and clear path for your international growth.

Phase 3: The Rapid Growth of UPI and QR Payments

The third phase involves a much newer and faster way to pay for things. Clearly, India’s UPI is changing how people and small firms send money today. Therefore, the link between UPI and other nations is a huge trend to watch.

Why UPI Is the Future of Small Cross-Border Payments

Firstly, UPI is very fast and works on your mobile phone in seconds. This allows you to pay for a meal or a small service with just a QR code. Secondly, it is very cheap because it skips many of the old bank fees.

Furthermore, many nations are now linking their own systems to the UPI network. Also, it allows for instant currency swaps at the moment of the sale today. Lastly, remember that fast mobile payments help your search engine trust and local SEO. Truly, UPI is the best tool for the small, daily needs of your global team. It allows you to move small amounts of cash without any of the old bank stress. This is why so many travelers and small shops love it in 2026.

Phase 4: Comparing the Three Systems for Your Business

The fourth phase is where you pick the right tool for your specific goal. Clearly, one system might be better for a factory order while another fits a small fee. Therefore, you must compare speed, cost, and reach for every single payment.

A Quick Look at the Payment Leaders

Firstly, use SWIFT for large, high-value deals with new partners in the West. This helps you stay secure and follows all the global banking rules today. Secondly, use CIPS if you are buying bulk goods from a supplier in China.

Furthermore, use UPI or its partners for quick travel costs or small digital tasks. Also, check the exchange rates for each system to see which one saves you the most. Lastly, check your search engine ranking to see how payment speed helps your traffic. Truly, a mix of these systems is your best tool for global success in 2026. It turns a complex task into a series of smart, fast wins for your brand. This ensures your business stays connected while the world changes its money rules.

Best Practices: Staying Safe in a Multi-System World

Finalizing your finance plan requires you to stay alert and very flexible. It needs you to know which rules apply to each system you choose to use. Clearly, you must follow all the laws to keep your accounts open and healthy. Therefore, follow these simple tips to keep your global payments safe and fast.

Simple Tips for Global Financial Success

Firstly, always verify the bank details of your partners before you hit send. This helps you avoid fraud and keeps your cash moving in the right direction. Secondly, keep your records clean so you can prove where your money came from.

Furthermore, use transition words in your invoices to make them easy for banks to read. Also, check the news for any new trade rules that might affect your chosen system. Lastly, check your search engine data to see if global fans trust your secure store. Truly, the world of finance is a journey that leads to a much better brand. It builds a path of wealth that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: Is SWIFT the same thing as a bank transfer?

SWIFT is the messaging network that banks use to send the instructions for a transfer.

Q2: Can I use UPI in every country today?

Not yet, but many nations like Singapore and the UAE now accept UPI-style payments.

Q3: Why did China create CIPS?

China wanted a system that helps more people use the yuan for global trade and deals.

Q4: Which system is the cheapest for small amounts?

UPI is usually the cheapest because it was built for small, fast mobile transactions.

Q5: Does my choice of payment system affect my SEO?

Indirectly, yes. Faster and more reliable payments lead to better user trust and site authority.

You must watch the rising friction between Europe and the United States today. Therefore, you should learn how these trade tensions change the world of payments. Truly, new digital rules in the EU are clashing with the way US tech firms work. Consequently, this creates a complex landscape for any business that moves money across borders.

Many people think that trade wars only happen with physical goods like steel or cars. But, the reality is that digital rules are the new battleground for global power. Always remember, a stable payment flow is a strong signal for any search engine. This ensures that your brand stays reliable and your global sales stay on track. This approach requires you to stay informed about new laws like the Digital Markets Act. It helps you build a much more resilient trade strategy for the long term. It makes your daily international sales feel much more secure and very effective.

Phase 1: The Clash of Digital Sovereignty

First, you must understand why the EU is creating strict new digital laws. Why does Europe want to limit the power of large US payment and tech firms? Clearly, the EU wants to protect its own digital market and its citizens’ data. Therefore, rules like the DMA and DSA target the biggest firms to ensure fair play.

Key Points of Friction in Digital Trade

Here are several areas where EU rules clash with US business models:

Market Access: New rules force US firms to open their systems to local rivals.

Data Privacy: Strict EU laws limit how US firms can move and use user data.

Anti-Trust: The EU often fines large firms for favoring their own payment tools.

Digital Tax: Many EU nations want to tax digital profits made within their borders.

Interoperability: Apps must now work with smaller, local payment providers.

Security Standards: The EU sets high bars for how firms must stop online fraud.

Search Engine Bias: Fair play rules help smaller sites gain better search engine visibility.

Truly, these tensions create a lot of noise in the global market today. But, you must also look at how these rules change the way you take payments. This keeps your business safe and prevents any sudden blocks in your cash flow. It creates a very high standard for your international trade operations.

Phase 2: How Tensions Impact Daily Payment Costs

So, how does a trade dispute in Brussels affect a shop in New York or Paris? Truly, higher tensions often lead to higher costs for moving money across the sea. Consequently, you might see a jump in the fees you pay for every global sale. It acts as a hidden tax on the growth of your digital business.

Why Your Payment Fees Might Rise

Here is how trade tensions impact your bottom line in 2026:

Compliance Costs: Firms spend more on lawyers to follow conflicting sets of laws.

Digital Levies: New taxes on tech giants often get passed down to the merchants.

Network Changes: US card firms may change their fee structures to cover EU fines.

Currency Shifts: Political noise can make the euro and dollar more volatile.

Local Mandates: You might have to use local EU tools that require a new setup.

Data Audits: You may pay extra for secure, EU-based data storage for your sales.

Trust Scores: Stable pricing helps you maintain a better search engine reputation.

Furthermore, this improves your search engine performance by letting you offer stable prices to fans. It makes your company look very professional and ready for 2026 shifts. This ensures that you keep more of your profit even when trade talks get messy. It creates a very fast and clear path for your financial planning.

Phase 3: The Move Toward Payment Independence

The third phase involves the EU building its own tools to rely less on the US. Clearly, Europe does not want to be vulnerable to foreign policy changes. Therefore, the rise of the digital euro and Wero is a direct response to these tensions.

Europe’s Plan for Financial Freedom

Firstly, the EU is pushing for a system that works without US-based card networks. This helps local firms keep their money within the European economy. Secondly, new laws encourage “open banking” so that users can pay directly from their accounts.

Furthermore, these tools offer a backup if trade relations ever break down completely. Also, they give the EU more power to set its own rules for digital safety and privacy. Lastly, remember that using local tools helps your search engine authority in the EU. Truly, this move toward independence is the biggest shift in payments for a decade. It allows the region to protect its interests while still staying part of the global market. This is why the ECB is working so hard on the digital euro today.

Phase 4: Navigating the Future of Global Sales

The fourth phase is where you adapt your business to survive this trade friction. Clearly, you cannot change the laws, but you can change how you react to them. Therefore, you must build a flexible payment setup that works on both sides of the sea.

How to Stay Flexible in a Divided Market

Firstly, use payment gateways that support both US cards and local EU tools like Wero. This helps you reach every customer no matter what happens in the news. Secondly, stay updated on the latest data transfer rules between the US and the EU.

Furthermore, consider setting up a local entity in the EU to simplify your taxes and rules. Also, use simple words in your checkout to explain why you offer different ways to pay. Lastly, check your search engine ranking to see how global trust helps your site. Truly, a flexible plan is your best tool against trade tensions. It turns a political risk into a series of smart, adaptive wins for your brand. This ensures your business stays running while the giants argue over the rules.

Best Practices: Protecting Your Brand Reputation

Finalizing your trade strategy requires you to stay out of the political crossfire. It needs you to focus on what your customers need from you right now. Clearly, fans just want a safe and easy way to pay for your great goods. Therefore, follow these simple tips to keep your brand strong during these tensions.

Simple Tips for Global Trade Success

Firstly, always follow the strictest privacy laws to keep all your customers safe. This builds a path of trust that works in both the US and the EU today. Secondly, monitor your payment success rates to catch any blocks from foreign networks.

Furthermore, use transition words in your shipping guides to explain any new rules. Also, check for new digital tax rules every quarter to avoid any surprise bills. Lastly, check your search engine data to see if global fans still trust your store. Truly, surviving a trade war is a journey that leads to a much stronger brand. It builds a path of safety that lets your whole team grow very fast. This secures your future in the digital world for a long time.

Frequently Asked Questions (FAQs)

Q1: Why are the US and EU arguing over digital rules?

They are fighting over who controls user data and how much power big tech firms should have.

Q2: Will my US credit card still work in Europe?

Yes, but you might see new fees or more security checks due to new EU laws in 2026.

Q3: Does this trade tension help my search engine rank?

No, but showing that you follow all local laws improves your site’s trust and SEO scores.

Q4: What is the Digital Markets Act (DMA)?

It is an EU law that forces large tech “gatekeepers” to be fairer to smaller local rivals.

Q5: Should I stop using US payment firms?

No, but you should add local European payment choices to your store to stay safe and flexible.

Handling money online requires a very high level of trust and speed between a business and its customers. Therefore, the rise of AI agents in payment gateway support is a major milestone for the financial industry. Truly, these smart systems are now capable of solving complex transaction issues in a matter of seconds. Consequently, businesses can enjoy much higher uptime and fewer lost sales due to technical errors.

Some people feel that financial support should always be handled by a human being to ensure safety. But, the reality is that AI agents can process data and find errors much faster than any person could. Always remember, a fast and reliable payment process is a strong signal for any search engine to trust your website. This ensures that your checkout page remains smooth and secure for every single user. This approach requires a focus on integrating smart tools into your existing banking stack. It helps you build a much more resilient and profitable online store for the long term. It makes your entire payment infrastructure feel much more modern and very effective.

Phase 1: Drastically Reducing Response and Resolution Times

First, let us look at how automation changes the speed of help when a payment fails. Why is it so important for a payment gateway to respond instantly to a support ticket? Clearly, every minute of downtime can mean thousands of dollars in lost revenue for a merchant. Therefore, AI agents are used to provide immediate answers to the most common transaction questions.

How AI Speed Benefits the Payment Industry

Here are several ways that automated agents improve the support experience:

Instant Error Decoding: AI can instantly explain why a specific credit card was declined.

Real Time Status Updates: Users get immediate info on where their refund is in the banking system.

24/7 Availability: Automated agents provide support at midnight or on holidays without any delay.

Automated Ticket Routing: The AI sends complex banking issues to the right human expert instantly.

Instant Documentation: Users get links to the exact help guide they need based on their error code.

Fraud Alerts: The system can explain a security hold to a customer as soon as it happens.

Transaction Lookups: AI agents find specific payments in a massive database in less than a second.

Truly, this level of speed is essential for maintaining customer confidence in a digital world. But, you must also ensure that the AI can hand off the conversation to a human when things get too complicated. This keeps your support system balanced and prevents customer frustration during sensitive money matters. It creates a very reliable and high standard for your financial brand.

Phase 2: Improving Fraud Detection and Security Communication

So, how does artificial intelligence help keep transactions safe while also helping the customer? Truly, the secret lies in the ability of AI agents to monitor millions of data points for signs of suspicious activity. Consequently, this allows the gateway to stop fraud before it happens while explaining the situation clearly to the user. It acts as a digital bodyguard that also speaks clearly to the people it protects.

Enhancing Security Through Automated Intelligence

Here is how AI agents help manage security in payment support:

Pattern Recognition: The AI spots unusual buying habits that might suggest a stolen card.

Immediate Verification: The agent can trigger a two step check if a login looks strange.

Clear Explanations: Instead of a vague error, the AI tells the user exactly how to verify their identity.

Risk Scoring: Every transaction gets a safety score in real time to prevent chargebacks.

Bot Prevention: Automated systems can tell the difference between a real buyer and a malicious script.

Compliance Monitoring: The AI ensures every support interaction follows strict banking privacy rules.

Search Engine Trust: Secure payment paths improve your search engine reputation and site safety.

Furthermore, this improves your search engine performance by reducing the number of fraudulent links associated with your domain. It makes your brand look very secure and professional to both banks and customers. This ensures that your business stays on the right side of financial regulations while growing your audience. It creates a very safe and stable environment for your digital commerce.

Phase 3: Personalizing the Merchant Experience at Scale

The third phase looks at how gateway providers support the businesses that use their software. Clearly, a small coffee shop has different payment needs than a global software company. Therefore, AI agents use data to provide custom advice to every merchant without needing a huge team of consultants.

Tailoring Support with Intelligent Data

Firstly, the AI agent analyzes the merchant’s sales volume to suggest the best fee structure. This allows the business owner to save money without having to ask for a review. Secondly, the system suggests new payment methods, like digital wallets, based on where the customers are located.

Furthermore, it provides proactive alerts if the merchant’s refund rate starts to climb too high. Also, the tool helps the team set up their checkout page to match the latest search engine optimization trends. Lastly, remember that a personalized support experience leads to much higher merchant loyalty. Truly, AI agents allow gateway providers to act as a partner rather than just a utility. It allows them to provide high level financial coaching to thousands of businesses at once. This is why the best payment platforms are investing heavily in automation in 2026.

Phase 4: Streamlining Onboarding and Compliance Checks

The fourth phase addresses the difficult process of getting a new business approved to take payments. Clearly, the paperwork and background checks can take weeks if they are done manually. Therefore, AI agents are now used to scan documents and verify identities in a fraction of the time.

Accelerating the Path to Your First Sale

Firstly, the AI checks business licenses and IDs for authenticity as soon as they are uploaded. This makes the onboarding process feel fast and modern for the new business owner. Secondly, the system automatically flags any missing information so the merchant can fix it immediately.

Furthermore, the agent guides the user through the technical setup of their API keys and webhooks. Also, it monitors the first few transactions to ensure everything is working perfectly. Lastly, monitor your search engine ranking to ensure your new store is visible to the world. Truly, no-code AI tools make it possible for anyone to start taking payments in just a few hours. It turns a boring legal process into a smooth and helpful digital journey. This ensures your business can start making money as quickly as possible.

Best Practices: Choosing a Gateway with Smart Support

Selecting the right payment partner requires looking at how they handle their technical support. It needs a focus on finding a provider that balances automated speed with human empathy. Clearly, the best gateway for your business is one that uses AI to make your life easier. Therefore, follow these simple tips to find the perfect payment partner today.

Strategies for Selecting a Modern Payment Gateway

Firstly, look for a provider that offers an AI chat agent that can actually solve problems. This saves you from waiting in a phone queue every time a transaction fails. Secondly, ensure the platform provides detailed automated reports on your sales and refund trends.

Furthermore, check if the gateway uses AI to automatically fight false chargebacks on your behalf. This protects your revenue and keeps your merchant account in good standing. Also, use plenty of transition words in your own site copy to keep your customers informed. Lastly, keep an eye on your search engine metrics to see how your checkout speed affects your traffic. Truly, the impact of AI agents on payment support is a huge win for everyone involved in online sales. It builds a foundation of efficiency that lets you focus on your products instead of your payments. This secures your future in the global digital marketplace.

Frequently Asked Questions (FAQs)

Q1: Can an AI agent fix a declined credit card?

An AI agent cannot force a bank to accept a card, but it can tell you exactly why it was declined so you can fix the issue.

Q2: Is my financial data safe when talking to an AI agent?

Yes, reputable payment gateways use the same high level encryption for their AI support as they do for their transactions.

Q3: How does faster payment support help my search engine ranking?

Faster support leads to better user experiences and less site downtime, which are both positive factors for any search engine.

Q4: Will AI agents replace human support in payment gateways?

AI will handle the majority of simple tasks, but humans will always be needed for complex legal and financial disputes.

Q5: Do I need to pay extra for AI-powered support?

Most modern gateways include these automated tools as part of their standard service because it helps them stay competitive.

Digital money is changing how the world thinks about finance. Therefore, India finds itself at a very major turning point. But, the path for crypto has not been easy or simple. Truly, it is a mix of high interest and strict rules.

Some people see crypto as a great way to pay for things. But, the government has many concerns about safety and stability. Consequently, the rules stay very firm for now. Always remember, India has a very large and tech-savvy population. This ensures that the talk about crypto never really stops. It also means that the future could hold many big changes. This approach to money might look very different in a few years. It could transform how we shop and save every day.

The Current State of Crypto in the Indian Market

First, let us look at where things stand today. Why is crypto so popular yet so regulated? Clearly, millions of Indians already own some form of digital asset. Therefore, the market is already quite massive and active.

Key Factors Defining the Indian Crypto Space

Here are several things that define the current crypto scene in India:

High Tax Rates: There is a thirty percent tax on all crypto gains.

No Deductions: You cannot offset losses against your profits.

TDS Rules: A one percent tax is deducted at the source for every trade.

Banking Hurdles: Some banks are still slow to work with crypto exchanges.

High Adoption: Many young people use crypto as a long-term investment.

CBDC Launch: The RBI has started testing its own digital rupee.

Legal Gray Area: Crypto is not banned, but it is not legal tender either.

Truly, these factors make the market a bit complicated for new users. But, the interest remains very high across the country. This keeps the industry moving forward despite the tough rules.

How Cryptocurrency Payments Work Today: A Slow Shift

So, can you actually use crypto to buy a coffee in India? Not quite yet. Truly, most people use it as an investment like gold. It also serves as a way to store value over time. It acts as a digital version of a savings account for many.

Ways People Use Crypto in India Right Now

Here is how crypto moves through the Indian economy today:

Investment Portfolios: People buy and hold coins on local exchanges.

P2P Trading: Users trade directly with each other using special platforms.

Gift Cards: Some sites let you buy vouchers using digital coins.

Remittances: People send money from abroad using fast crypto networks.

Freelance Pay: Some global workers take their salary in digital assets.

Tech Testing: Developers use crypto to build new decentralized apps.

Educational Trading: Students learn how global markets work using small amounts.

Consequently, crypto is more of a tool for growth than for daily shopping. It helps people grow their wealth in a new way. This ensures they stay connected to global financial trends. It keeps the Indian tech scene very vibrant and modern.

Pillar 1: The Regulatory Framework and Tax Laws

The first pillar is all about the rules set by the government. The Ministry of Finance and the RBI watch crypto very closely. Clearly, they want to protect the rupee and stop financial crimes. Therefore, they have created a very strict tax system for everyone.

Understanding the 30 Percent Tax and 1 Percent TDS

Firstly, know the flat tax rate. If you make money from crypto, you must pay thirty percent to the state. This applies to every single profitable trade. Secondly, track the TDS on every transaction. The one percent TDS helps the government track who is buying and selling.

Furthermore, remember that losses do not help you. In normal stocks, you can use a loss to pay less tax. But, in crypto, you cannot do this at all. Also, report all holdings in your tax returns. Failing to show your crypto can lead to very big fines. Lastly, stay alert for new policy updates. The government might bring a new crypto bill to parliament soon. Truly, the tax laws are the biggest hurdle for users. They make daily payments very expensive and hard to track. This is why most people prefer to hold their assets for a long time.

Pillar 2: The Role of the RBI and the Digital Rupee (e-Rupee)

The second pillar focuses on the central bank. The Reserve Bank of India (RBI) is very cautious about private coins. Clearly, they prefer a digital currency that they can control. Therefore, they have launched the Central Bank Digital Currency (CBDC).

How the e-Rupee Differs from Private Crypto

Firstly, the e-Rupee is legal tender. It is exactly like a paper note but in digital form. You can use it to pay anyone in the country. Secondly, it has the full backing of the state. Unlike Bitcoin, the value of the e-Rupee is always stable.

Furthermore, it uses blockchain technology for safety. This makes the system very fast and very secure. Also, it helps reduce the cost of printing money. Digital notes are much cheaper to manage than paper ones. Lastly, it might replace private crypto for daily use. The RBI wants people to use the e-Rupee for shopping and bills. Truly, the e-Rupee is the official answer to the crypto craze. It offers the speed of crypto with the safety of the rupee. This will shape the road ahead for all digital payments in India.

Pillar 3: The Road Ahead – What the Future Holds

The third pillar is about looking into the future. Will India ever embrace Bitcoin for payments? Clearly, the next few years will be very important for this sector. Therefore, we must look at the likely trends and changes.

Predictions for the Indian Crypto Landscape

Firstly, expect more global cooperation on rules. India is working with the G20 to create common crypto laws. This will make the market safer for everyone. Secondly, watch for more institutional investment. If the rules get clearer, big banks might start offering crypto services.

Furthermore, look for a focus on Web3 and blockchain. India wants to be a leader in blockchain tech, even if it stays careful with coins. Also, anticipate a shift in tax policies. Many experts hope the tax rate will come down to match normal stocks. Lastly, see the rise of hybrid payment systems. We might see apps that use the e-Rupee and crypto side by side. Truly, the road ahead is full of both risks and great chances. It requires a balance between innovation and very strong safety. This ensures the Indian economy stays healthy and strong.

Best Practices: Staying Safe in the Indian Crypto Market

Using crypto in India requires a very careful approach. You must follow the laws and protect your assets. Clearly, the digital world has many scams and risks. Therefore, follow these simple steps to stay safe.

Strategies for Responsible Crypto Management

Firstly, use only registered Indian exchanges. These platforms follow the local laws and verify your identity. This makes your money much safer. Secondly, keep a detailed record of every trade. This is vital for paying your taxes correctly at the end of the year.

Furthermore, never share your private keys or passwords. Scammers often pretend to be help desk workers. Also, diversify your digital assets. Do not put all your money into just one coin or token. Lastly, only invest money you can afford to lose. Crypto prices can go up and down very fast in one day. Truly, being careful is the best way to enjoy the crypto world. It helps you learn without taking too much risk. This ensures a positive experience for every new user in India.

Frequently Asked Questions (FAQs)

Q1: Is it legal to buy Bitcoin in India right now?

Yes, it is legal to buy, sell, and hold Bitcoin in India. However, it is not considered legal tender. This means a shop can refuse to take it as payment for goods.

Q2: How much tax do I pay on crypto profits in India?

You must pay a flat thirty percent tax on all profits from digital assets. Additionally, a one percent TDS is deducted from the total value of every transaction.

Q3: Can I use crypto to pay for my mobile recharge or bills?

Directly using crypto for bills is rare due to tax and legal hurdles. However, some third-party sites allow you to buy gift cards with crypto to pay for such services.

Q4: What is the difference between Bitcoin and the e-Rupee?

Bitcoin is a private, decentralized asset with a volatile price. The e-Rupee is a digital currency issued and backed by the RBI, and its value is always stable.

Q5: Will the Indian government ban crypto in the future?

The government has not announced a ban. Instead, they are focusing on strict regulation and global cooperation to manage the risks associated with digital assets.

In the growing world of online marketplaces, sales happen fast. However, taking payment is just one part of the job. Truly, the hard part is managing the complex process of settlement and payouts. For any marketplace, giving money to many sellers, dealing with fees, and ensuring rules are followed is a huge job. Therefore, building a smart, automated settlement and payout workflow is essential. It is crucial for growing your business, keeping money accurate, and scaling well.

Many marketplaces, especially new ones, forget how complex payouts are. They often use slow, manual ways to send money. This method quickly fails when sales increase. Consequently, relying on old methods leads to errors, delays, and unhappy sellers. Clearly, a strong, smart workflow turns this problem into a major advantage. It makes sure money moves smoothly and clearly and frees up your team’s time. It also helps build trust with sellers. Ultimately, getting payouts right is key for any platform that wants to succeed in the digital market.

The Core Challenge: Too Many Parties, Too Much Detail

First, we need to know why settlement and payout are so hard for marketplaces. Unlike a simple online shop, a marketplace involves many people in every transaction. You have the buyer, the marketplace itself, and the sellers. Consequently, this multi-party system creates many layers of complexity. It demands careful handling of money, fees, and legal rules. Clearly, ignoring these details can cause big problems, money issues, and legal trouble. Therefore, a smart workflow must solve these main issues.

The Problem of Splitting Money and Following Rules

Firstly, the main hard part is the need to split payments. A buyer’s single purchase must be divided. Some money goes to the marketplace (for fees), and the rest goes to the seller. This requires careful math and tracking. Secondly, different payout times and amounts make things harder. Some sellers want money every day. Others prefer weekly or monthly. Some only get paid after they earn a certain amount. Handling these different needs by hand is almost impossible as you grow.

Furthermore, selling globally and dealing with different money adds extra currency problems. Following many global money rules and tax laws (like KYC and AML) is also a massive task. This is true even for platforms that operate in just a few countries. Additionally, handling refunds, failed charges, and fights complicates things more. These events need changes to money that was already sent out. Lastly, ensuring clear reporting and honesty for everyone is vital. This builds trust and manages expectations. Truly, a smart system must handle all these linked issues to work well and follow the law.

Key Components: What Makes a Payout System Smart

Building a truly smart settlement and payout system for a marketplace needs several core parts to work together. It is not just about sending money. Instead, it is about having a complete system that handles payment starts, checking records, stopping fraud, following rules, and clear reports. Clearly, a full system ensures things are fast, accurate, and ready to grow. Therefore, every part must be planned and linked well.

Essential Tools for Automated and Legal Payouts

Firstly, you need a reliable payment control tool. This system manages incoming payments from buyers. It holds the funds safely. Then, it uses rules to send money out. It often works with many different payment companies, offering backup and choice. Secondly, a strong seller setup and checking system (KYC/AML) is key. This makes sure all people receiving money are real and follow financial rules. This reduces fraud and legal risks right from the start.

Furthermore, an automated fee deduction and splitting engine is very important. This part automatically figures out marketplace fees, bank costs, and other money taken out. It makes sure sellers get the correct final amount. Additionally, a flexible payout timing and method tool lets sellers pick their preferred payment schedule. They can choose how often they get paid and how (bank transfer, digital wallet). This makes sellers much happier. Lastly, complete checking and reporting tools are vital. These tools automatically match sales, check balances, and create clear statements. This gives honesty and makes accounting easier. Truly, linking these parts creates a powerful, fast, and lawful payout environment.

Security and Compliance: Safety and Rules Must Come First

In the detailed world of financial actions, following the rules and reducing risk are essential. This is even more true for marketplaces that manage many people’s money. Truly, a smart settlement and payout system must have strong steps built in. These steps must meet legal needs. They also need to stop fraud and mistakes. Clearly, failing in these areas can bring big penalties and harm your good name. Therefore, taking action early is critical.

Navigating Rules and Stopping Fraud

Firstly, Know Your Customer (KYC) and Anti-Money Laundering (AML) rules must be followed. Your system must automatically collect and check seller IDs. This often means checking documents and using databases. This is not just a law. It is crucial for stopping bad activity on your platform. Furthermore, you must use fraud detection and prevention tools that look at payout patterns. Strange amounts, timings, or bank accounts can signal fraud. These signs should trigger automatic checks or holds.

Secondly, make sure your system follows PCI DSS rules if you handle card data. Or, work only with payment processors that follow these rules. Keeping data secure is basic to building trust. Additionally, manage tax reporting duties well. Based on where you are and where your sellers are, you may need to collect tax IDs and send reports often. A smart workflow does this work automatically. This greatly reduces manual effort and risk. Truly, by adding these security and compliance steps, marketplaces can operate safely and build confidence for everyone involved.

Optimizing for Speed, Clarity, and Growth

While following rules and accuracy are basic needs, a truly smart system also focuses on speed, clarity, and growth potential. In fact, in a crowded marketplace, fast and clear payouts make sellers happy. They also bring in better sellers. Clearly, being able to grow without problems as sales increase is also key for long-term success. Therefore, always making things better in these areas is vital.

Making Things Better for Sellers and the Marketplace

Firstly, to make things faster, use instant or very quick payout options. These are good where they are allowed and cost-effective. Regular bank transfers take days. Fast options like real-time payments or digital wallets can greatly speed up the process. Furthermore, make checking records automatic. This removes slow manual checking. Fast internal work means faster money processing.

Secondly, for clarity, give sellers real-time information about their earnings, fees, and payout history. Use a special seller page for this. Clear, detailed sales reports build trust. They also lead to fewer questions for your support team. Fast messages about when money is coming also help sellers a lot. Lastly, plan your system for growth from the beginning. Pick payment partners and systems that can handle more sales and more sellers without needing big changes. Cloud systems and systems that use APIs are often best for this. Truly, by focusing on speed, clarity, and growth, marketplaces create a great experience for sellers. This helps build a loyal community that drives continuous success.

Best Practices: How to Build Your Smart System

Building a smart settlement and payout workflow is a hard job. But marketplaces can succeed by following simple best practices. Clearly, learning from others and making small changes often will make sure your system is strong and ready for the future. Therefore, a careful plan that mixes technology, process, and user experience is crucial.

A Plan for Successful Payout System Building

Firstly, pick the right payment partners. Choose companies that offer good APIs, global reach (if you need it), support for many currencies, strong security features, and great help. Do not just pick the cheapest. Reliability and features are more important. Secondly, design for easy changes. Your marketplace will change. Your payout system should be able to handle new payment types, fee changes, and new rules easily. A system built with APIs makes changes and linking new tools much simpler.

Furthermore, make things automatic whenever you can. From splitting payments and taking out fees to checking records and tax reporting, automate all repeated tasks. This reduces mistakes and cost. It lets your team focus on smart work. Also, invest in full testing and checking. Test your system well under different situations. Do this before you launch. Use tools to watch your system all the time. These tools should alert you about any issues right away. Lastly, always ask sellers for their thoughts. Their experience is most important. Use their feedback to find problems and make improvements often. Truly, by following these best practices, marketplaces can build a smart, strong, and friendly payout system that supports long-term success.

Frequently Asked Questions (FAQs)

Q1: What is the biggest challenge for marketplaces in managing payouts?

The biggest challenge is often the hard job of splitting payments accurately among many groups. This includes taking out various fees. It also means handling different payout schedules and following money rules in different places. All this must be done while growing fast.

Q2: How can a marketplace ensure compliance with KYC/AML rules for payouts?

Marketplaces ensure compliance by using automated checking systems during seller setup. These systems check and confirm seller identities. They often use document checks and database lookups. This makes sure all people receiving money are real and follow anti-money laundering laws.

Q3: What is the role of a “payment orchestration layer” in a smart payout workflow?

A payment orchestration layer works as a central manager. It smartly guides and controls money coming in and payouts going out and links to many payment companies. It handles payment splitting and fee deductions and often uses logic to pick the best payment route for speed or cost.

Q4: How can marketplaces offer faster payouts without taking on too much risk?

Marketplaces can offer faster payouts by using instant payment networks and digital wallets. They also use carefully managed reserves. While moving fast, it is vital to have strong fraud checks. You must also do KYC/AML checks. This prevents bad transactions and chargebacks.

Q5: What reporting features are essential for a smart payout workflow?

Essential reporting features include real-time dashboards for sellers to see earnings and history. You also need detailed reconciliation reports for the marketplace. These match incoming and outgoing money. Finally, you need automatic tax document creation. Clarity is the most important thing.

In today’s fast-paced digital economy, every transaction tells a story. Indeed, raw payment data, often overlooked, holds an extraordinary wealth of information just waiting to be uncovered. Therefore, payment analytics emerges as a critical discipline, transforming this vast stream of transaction data into actionable growth insights. Truly, it allows businesses to move beyond simple reporting, delving deep into customer behavior, operational efficiency, and revenue opportunities. Clearly, by harnessing the power of these insights, companies can make smarter decisions, optimize their payment strategies, and ultimately drive sustainable growth. Furthermore, ignoring this valuable data means leaving money and opportunities on the table.

Many businesses view payment data merely as a record of financial exchange. However, this perspective severely limits its potential. In reality, payment analytics provides a 360-degree view of your customer’s purchasing journey, from initial interest to successful checkout. This comprehensive understanding enables businesses to identify trends, predict future behaviors, and proactively address challenges. Always remember, the goal is not just to process payments, but to learn from them. This strategic approach turns every swipe, click, or tap into a valuable piece of intelligence, guiding future business decisions with precision and foresight.

The Foundation of Payment Analytics: What It Is and Why It Matters

To begin with, let’s clearly define what payment analytics actually entails. Simply put, payment analytics is the process of collecting, processing, and analyzing data generated from every financial transaction a business handles. This data includes information such as transaction amounts, payment methods, customer locations, timestamps, and even fraud attempts. Consequently, by applying various analytical techniques, businesses can uncover patterns, correlations, and anomalies that are invisible to the naked eye. This deeper understanding is paramount for making data-driven decisions that impact the bottom line.

Why Payment Analytics is Indispensable for Modern Businesses

Naturally, the importance of payment analytics cannot be overstated in the current competitive landscape. Firstly, it offers an unparalleled view into revenue optimization. By understanding which payment methods are preferred, where conversion rates drop, or how different pricing strategies impact sales, businesses can fine-tune their offerings. Secondly, it plays a vital role in fraud detection and prevention. Analyzing transaction patterns helps identify suspicious activities in real time, significantly reducing financial losses and protecting customer trust. Clearly, a robust analytics system can be your first line of defense.

Furthermore, payment analytics dramatically enhances customer experience. By knowing customer preferences and pain points in the payment journey, companies can streamline checkout processes, offer preferred payment options, and provide a seamless experience. This leads to higher customer satisfaction and loyalty. Lastly, it drives operational efficiency. Identifying bottlenecks in payment processing, understanding chargeback reasons, or optimizing vendor relationships can lead to substantial cost savings. Therefore, payment analytics moves beyond mere financial reporting, becoming a strategic tool for continuous improvement and growth.

Key Metrics and Dimensions in Payment Analytics

To truly extract value from your payment data, you must focus on the right metrics and dimensions. Indeed, simply collecting data is not enough; you need to know what questions to ask. Consequently, identifying key performance indicators (KPIs) relevant to payments allows you to measure success, pinpoint areas for improvement, and track progress over time. Therefore, a clear understanding of these metrics is fundamental to any effective payment analytics strategy.

Essential Metrics for Deeper Insights

First, consider conversion rates at various stages of the payment funnel. How many customers initiate a checkout versus how many complete it? Tracking this helps identify drop-off points. Next, examine average transaction value (ATV), which provides insights into customer spending habits. A rising ATV suggests effective upselling or a higher perceived product value. Furthermore, payment method breakdown is crucial. Understanding which payment types (credit card, digital wallet, bank transfer) are most popular among different customer segments enables you to optimize your offerings.

Moreover, chargeback rates are critical for assessing fraud and customer dissatisfaction. A high chargeback rate indicates underlying issues that need immediate attention. You should also track payment success rates, identifying any recurring errors or declines that might be deterring customers. Additionally, transaction volume and frequency over time can reveal seasonal trends and peak periods, informing staffing and inventory decisions. Finally, customer lifetime value (CLV), when viewed through the lens of payment data, offers insights into the long-term profitability of different customer segments. Truly, a holistic view of these metrics empowers businesses to make informed, impactful decisions.

Leveraging Payment Analytics for Revenue Optimization

One of the most immediate and impactful benefits of payment analytics is its ability to directly influence revenue. By scrutinizing transaction data, businesses can uncover opportunities to increase sales, improve conversion rates, and enhance profitability. Clearly, a deeper understanding of payment trends allows for targeted strategies that resonate with customer preferences and overcome potential hurdles in the buying journey. Therefore, every business aiming for growth must prioritize this area.

Strategies for Boosting Your Top Line

Firstly, use payment analytics to optimize your payment mix. By identifying the most preferred payment methods for different demographics or regions, you can ensure these options are prominently displayed and seamlessly integrated. For example, if mobile wallet usage is surging in a particular market, prioritizing that option can significantly boost conversions. Secondly, analyze data to identify and mitigate conversion bottlenecks. Perhaps a specific payment gateway consistently experiences higher failure rates, or customers abandon carts at the final payment step. Pinpointing these issues allows for targeted improvements, such as switching providers or simplifying the checkout flow.

Furthermore, payment analytics assists in dynamic pricing and promotions. Understanding how different price points or discount structures impact payment behavior and overall revenue enables businesses to tailor offers more effectively. For instance, you might discover that a specific payment method user responds better to loyalty rewards. Also, analyze subscription payment data to reduce churn. Identifying patterns in failed recurring payments, such as expired cards, allows for proactive communication and retries, thereby preserving recurring revenue. Ultimately, this strategic application of payment data ensures you’re not just processing transactions, but actively growing your revenue streams.

Enhancing Security and Fraud Prevention with Payment Analytics

In the digital landscape, where cyber threats are constantly evolving, safeguarding transactions against fraud is paramount. Payment analytics plays an indispensable role in strengthening security measures and proactively detecting suspicious activities. Consequently, by analyzing payment data patterns, businesses can build more robust fraud prevention systems, protect their financial integrity, and maintain customer trust. Clearly, neglecting this aspect can lead to significant financial losses and reputational damage.

Building Robust Fraud Detection Systems

Firstly, payment analytics enables the identification of unusual transaction patterns. Fraudulent activities often deviate significantly from normal purchasing behavior. For example, multiple small purchases from different geographic locations in a short period, or unusually high-value transactions from new customers, can be red flags. By establishing baselines of normal behavior, analytics systems can flag these anomalies for further investigation. This real-time detection is crucial for mitigating damage.

Secondly, you can use payment data to enrich fraud models. Integrating data points like IP addresses, device fingerprints, shipping addresses, and customer transaction history provides a more comprehensive picture for machine learning-based fraud detection algorithms. These algorithms learn from past fraudulent and legitimate transactions to predict future risks with high accuracy. Furthermore, analytics helps in reducing false positives. While aggressive fraud detection can block legitimate transactions, payment analytics refines the rules, ensuring that valid customers can complete their purchases without unnecessary friction, thereby improving the customer experience. Ultimately, leveraging payment analytics for fraud prevention transforms your security from a reactive measure into a proactive, intelligent defense mechanism.

Driving Operational Efficiency and Customer Experience

Beyond revenue and security, payment analytics offers profound benefits for streamlining operations and elevating the customer experience. In fact, by understanding the intricate details of how payments flow through your systems and how customers interact with them, businesses can identify inefficiencies and pinpoint areas for service improvement. Truly, an optimized payment journey directly translates into higher customer satisfaction and loyalty.

Streamlining Processes and Delighting Customers

Firstly, payment analytics helps in optimizing payment gateway performance. By monitoring success rates and latency across different providers, businesses can identify underperforming gateways or regions where specific providers excel. This allows for intelligent routing of transactions, ensuring higher success rates and faster processing times. Furthermore, analyzing transaction failure reasons—such as insufficient funds, incorrect card details, or technical errors—enables proactive communication with customers or internal system adjustments, thereby reducing abandoned carts.

Secondly, analytics provides insights into customer payment preferences, which is vital for enhancing the user experience. For instance, if a significant portion of your mobile users prefers digital wallets, making those options easily accessible and intuitive can significantly improve checkout speed and convenience. Conversely, if a particular region heavily relies on bank transfers, ensuring that option is robustly supported is crucial. Moreover, understanding chargeback reasons goes beyond fraud; it can reveal issues with product delivery, unclear billing, or poor customer service, prompting improvements across various operational touchpoints. In sum, payment analytics empowers businesses to fine-tune every aspect of their payment infrastructure, leading to smoother operations and a superior experience for every customer.

Frequently Asked Questions (FAQs)

Q1: What kind of data is included in payment analytics?

Payment analytics includes a wide range of transaction data, such as transaction amounts, timestamps, payment methods used (credit card, digital wallet, bank transfer), customer location, currency, device used for payment, success/failure status, and details related to chargebacks or refunds. It can also incorporate demographic and behavioral data if available.

Q2: How can payment analytics help reduce cart abandonment?

Payment analytics helps reduce cart abandonment by identifying common drop-off points and reasons for transaction failures. By analyzing data on where customers leave the checkout process, which payment methods fail most often, or what technical errors occur, businesses can pinpoint issues and make targeted improvements to streamline the payment flow and improve success rates.

Q3: Is payment analytics only useful for large enterprises?

Absolutely not! While large enterprises often have vast amounts of data, payment analytics is equally beneficial for small and medium-sized businesses (SMBs). Even with smaller transaction volumes, SMBs can gain valuable insights into customer preferences, identify fraud patterns, optimize payment costs, and improve their overall operational efficiency, leading to significant growth.

Q4: How does payment analytics contribute to better customer experience?

Payment analytics enhances customer experience by allowing businesses to understand and cater to customer preferences. By knowing which payment methods are preferred, which parts of the checkout process cause friction, or why transactions fail, companies can optimize their payment offerings, simplify the checkout flow, and provide proactive support, leading to smoother, more satisfying interactions.

Q5: What’s the difference between payment analytics and general financial reporting?

General financial reporting typically focuses on historical data to track overall financial health (e.g., total revenue, expenses, profits). Payment analytics, however, delves much deeper into the details of payment transactions to uncover actionable insights, predict future trends, optimize processes, and identify specific opportunities for growth, fraud prevention, and customer experience improvement.

The world of digital payments is constantly evolving. Every year brings new technologies, new consumer habits, and, crucially, new regulations. For businesses, understanding these changes is not just important; it is essential for managing costs and maintaining profitability. Specifically, the Merchant Discount Rate (MDR) has always been a critical factor in the cost of accepting digital payments. This fee directly impacts a merchant’s bottom line. Recently, 2025 brought about significant shifts in both MDR structures and the landscape of “Zero MDR” policies. These changes have reshaped how merchants, payment processors, and even customers interact with digital transactions. Today, we will break down what exactly changed and what it means for your business.

Understanding the Merchant Discount Rate (MDR)

Before discussing the changes, we should revisit what MDR actually is. The Merchant Discount Rate is the fee charged to a merchant by their bank or payment service provider for processing customer payments made through debit cards, credit cards, or other digital methods. This fee is usually a percentage of the transaction value. Additionally, it often includes a small fixed per-transaction fee. The MDR is not a single fee; instead, it is typically a blend of three main components:

Interchange Fee: This is the largest component, paid by the acquiring bank (merchant’s bank) to the issuing bank (customer’s bank).

Scheme Fee: This fee is paid to the card networks (like Visa or Mastercard) for using their infrastructure.

Acquirer Markup: This is the fee charged by the merchant’s bank or payment processor for their services.

Therefore, understanding these components is crucial to grasping why changes to MDR policies have such a wide-reaching impact on businesses.

The Rise and Fall of Zero MDR Policies

The concept of “Zero MDR” gained significant attention in previous years, especially in markets aiming to boost digital payments. Specifically, a Zero MDR policy meant that merchants would not be charged any fees for processing payments through certain digital channels, particularly debit card or UPI transactions. The government or regulatory bodies often absorbed these costs.

Consequently, the goal was to incentivize merchants to adopt digital payment methods, thereby promoting a cashless economy. While beneficial for merchants in the short term, this policy put immense pressure on payment service providers and banks. Therefore, maintaining the underlying infrastructure and services without a direct revenue stream became unsustainable. These pressures naturally led to policy re-evaluations, culminating in the significant shifts seen in 2025 regarding MDR.

Key Changes to MDR Policies in 2025

The year 2025 brought a series of calculated adjustments to MDR policies, moving away from a blanket Zero MDR approach in many regions. Specifically, these changes typically included:

Tiered MDR Structures: Many regions reintroduced or refined tiered MDR structures. These structures differentiate fees based on transaction value, merchant type (e.g., small business vs. large enterprise), and the payment method used (e.g., credit card, debit card, QR code). Therefore, this aims for a fairer distribution of costs.

Revised Interchange Caps: Governments and regulatory bodies often reviewed and adjusted interchange fees. This component of the MDR is a major driver of overall cost. New caps might aim to reduce overall costs for merchants while still allowing issuing banks to recover some operational expenses.

Emphasis on Digital Infrastructure Costs: The new policies often acknowledge the increasing investment required for secure digital payment infrastructure. Therefore, the revised MDR structures now attempt to ensure payment processors and banks can cover these operational and technological costs.

These changes reflect a balancing act: promoting digital payments while ensuring the sustainability of the payment ecosystem, affecting every aspect of MDR.

Impact on Merchants: Navigating New Costs

For merchants, the changes to MDR policies in 2025 mean a direct reassessment of their payment processing costs. Businesses that previously benefited from Zero MDR policies now face new fees for certain transactions. Therefore, this requires a careful review of their pricing strategies. Small and medium-sized enterprises (SMEs) are particularly affected, as even minor increases in transaction costs can significantly impact their margins. Consequently, merchants must:

Review Payment Mix: Analyze which payment methods their customers use most frequently and understand the associated new MDRs.

Negotiate with Providers: Engage with their payment service providers to understand the updated fee structures and potentially negotiate better rates based on their transaction volume.

Explore Cost-Saving Measures: Consider implementing technologies that optimize payment routing or reduce chargebacks, which indirectly lowers overall payment costs.

Ultimately, proactive management of these new MDR costs is crucial for maintaining profitability in the digital age.

Impact on Payment Service Providers and Banks

The shifts in MDR policies in 2025 have profound implications for payment service providers (PSPs) and banks. For these entities, the reintroduction or adjustment of MDR fees often means a return to a more sustainable revenue model. Previously, Zero MDR policies strained their ability to invest in technology, security, and customer service. Therefore, the new policies generally aim to provide a more predictable revenue stream. Consequently, PSPs and banks can now:

Invest in Innovation: Allocate more resources to developing advanced payment technologies, enhancing security features, and improving user experience.

Expand Digital Infrastructure: Further build out the networks and systems necessary to support a growing volume of digital transactions.

Offer Differentiated Services: Compete on value-added services rather than just trying to absorb costs, which benefits merchants with more choices.

However, they must also effectively communicate these changes to merchants and offer competitive pricing, especially concerning MDR.

The Broader Economic Context and Digital Adoption

The 2025 changes to MDR policies are not isolated; instead, they reflect broader economic trends and the maturing of digital payment ecosystems. As more economies transition towards digital transactions, the initial incentives like Zero MDR become less necessary. The focus shifts to building a self-sustaining and robust payment infrastructure. Therefore, these policy adjustments indicate a move towards greater market efficiency. They ensure that all participants—merchants, consumers, and payment providers—contribute to the cost of maintaining a secure and efficient digital payment network. Consequently, while some merchants may see increased costs, the long-term goal is a more stable and innovative digital payment landscape, driven by fair MDR structures.

Conclusion

The year 2025 marked a pivotal moment in the evolution of MDR and Zero MDR policies, fundamentally altering the economics of digital payments. While the departure from universal Zero MDR might initially present challenges for some merchants, these changes are generally aimed at fostering a more sustainable and equitable digital payment ecosystem. Therefore, businesses must thoroughly understand these new MDR structures. They must also proactively adapt their strategies to manage costs effectively. Ultimately, the ongoing evolution of payment regulations, including adjustments to the Merchant Discount Rate, is a constant reminder that staying informed and agile is paramount for success in the ever-changing digital economy.

Frequently Asked Questions (FAQs)