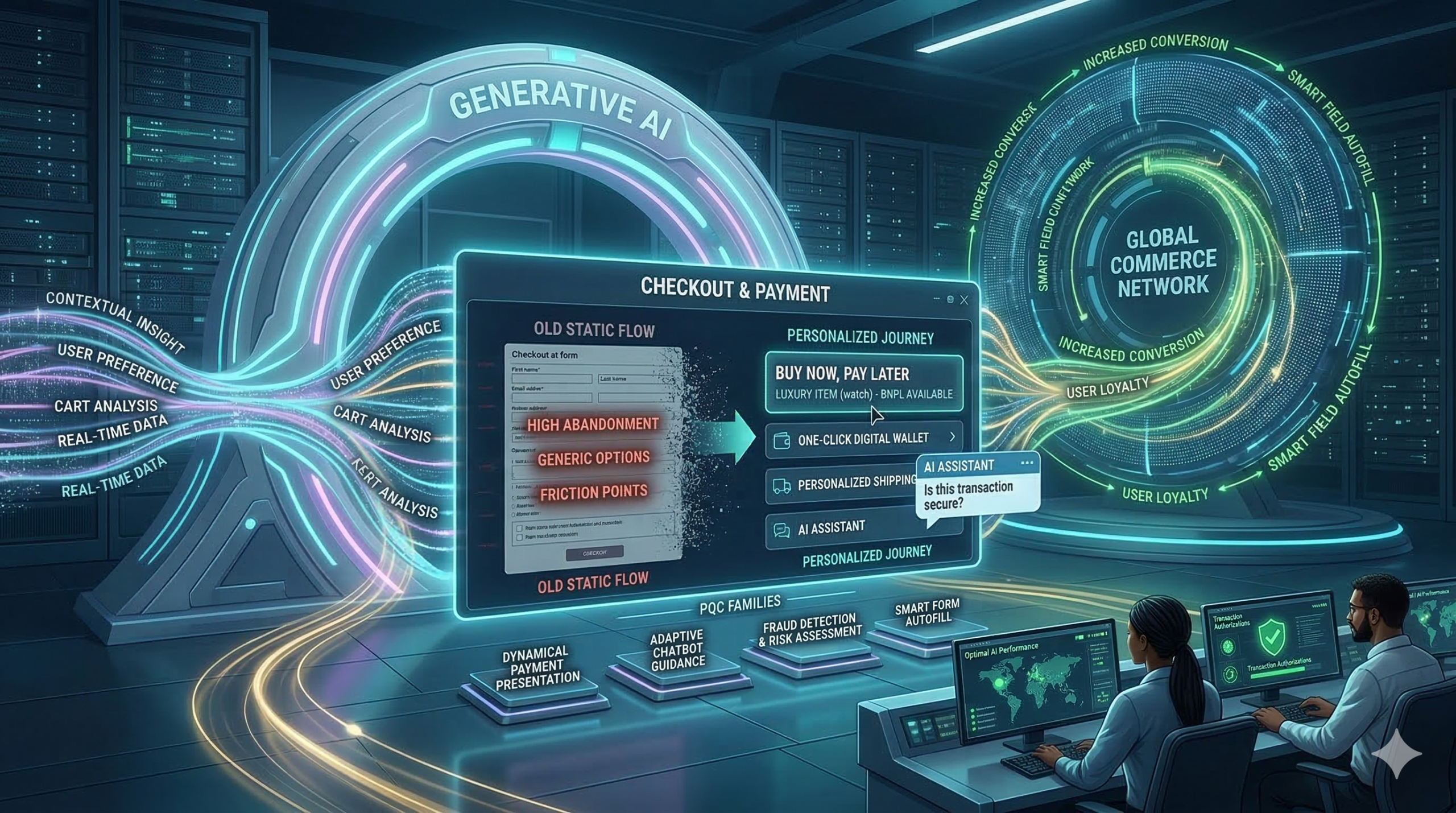

Most online stores lose customers at the final step because traditional checkout pages are often slow and boring. Now, generative ai is changing that forever by creating a personal path for every shopper. Because this technology learns what you like and how you want to pay, buying things online is faster than ever. Furthermore, smart stores use generative ai to turn one-time shoppers into loyal fans. This shift is vital for any brand that wants to grow. Consequently, the payment journey is no longer just a task; it is an experience.

Why Old Checkout Systems Fail

Static forms are the biggest enemy of sales because most shops show the same fields to everyone. Consequently, many people leave their carts empty. This is because the process feels long and hard. Generative ai solves this by making every page unique for the user. For instance, it knows if you are on a phone or a laptop. Furthermore, it predicts which payment method you prefer. Therefore, you spend less time typing and more time enjoying your purchase. In short, ai removes the friction that kills sales.

Real-Time Help with Generative AI

Shopping can sometimes feel confusing, especially when you have questions about shipping or taxes. Standard help pages are often hard to find. However, ai adds a smart assistant to the page to guide you. This bot answers your questions in seconds. Because the bot knows your cart, it gives perfect advice. This builds trust and keeps you moving forward. In addition, ai makes sure you never feel alone while shopping.

Moreover, these bots can offer special deals at the perfect moment. If you hesitate, the generative ai might give you a small discount to help you decide. As a result, shoppers feel valued and safe. Generative ai is not just a tool; it is a digital guide. Because of these benefits, top brands are moving to AI today. Therefore, the checkout flow becomes a conversation instead of a form.

Safer and Faster Payments

Security is the most important part of any sale because hackers are always looking for ways to steal data. Luckily, ai is great at spotting fraud by looking at millions of data points in real-time. If it sees something odd, it stops the threat fast. This keeps your money and data very safe. Because the ai is so smart, it rarely blocks real customers. Thus, generative ai makes payment security much stronger for everyone.

Additionally, generative ai helps with filling out forms by guessing your address with high accuracy. This reduces errors and saves time for the customer. When you use generative ai, the checkout flow feels like magic. You just click and go. Therefore, the risk of a mistake is very low. This is the future of ai in the payment world. Finally, this technology ensures that safety does not come at the cost of speed.

The Big Future of Generative AI

We are only at the start of this change. Soon, every store will use ai to talk to us. It will know our size, our style, and our budget. This means we will see fewer ads we do not like. Instead, we get a tailored world of products. Generative ai makes every transaction feel human. It is the best way to shop in 2026. If you want to stay ahead, you must use generative ai now. In conclusion, the personalized payment journey is the new standard for global trade.

Frequently Asked Questions

1. Is generative ai safe for my credit card?

Yes, it improves security by spotting fraud much faster than older systems.

2. Does generative ai make my phone slow?

No, most of the work happens on fast servers, so your phone stays quick.

3. Why do stores need ai?

It helps them sell more by making the checkout process easy and personal for everyone.

4. Can generative ai help with returns?

Yes, it can guide you through the return process and answer policy questions instantly.

5. Will all stores use generative ai soon?

Yes, it is becoming the global standard for all top e-commerce websites.

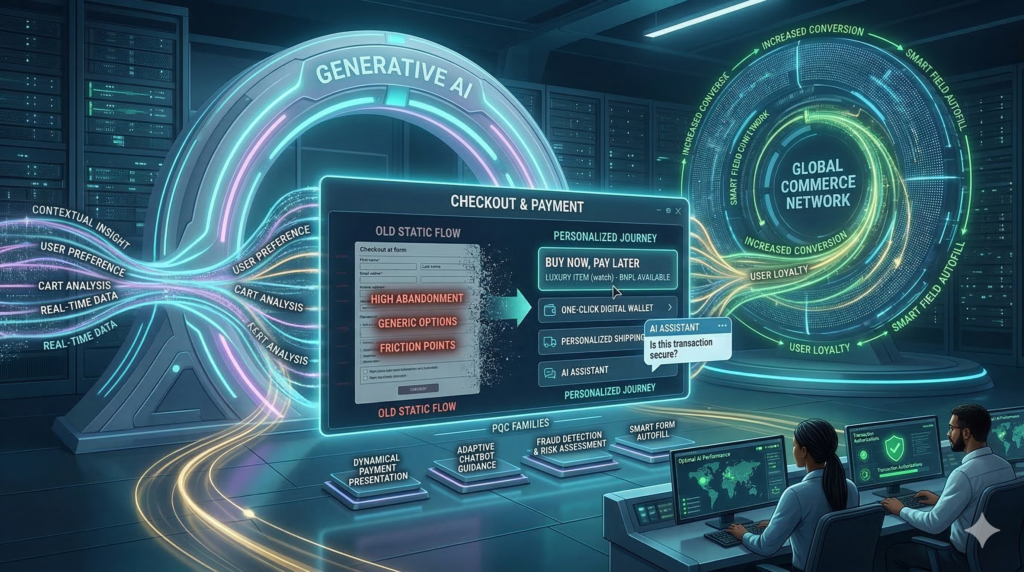

Most online stores lose customers at the final step because traditional checkout pages are often slow and boring. Now, generative ai is changing that forever by creating a personal path for every shopper. Because this technology learns what you like and how you want to pay, buying things online is faster than ever. Furthermore, smart stores use generative ai to turn one-time shoppers into loyal fans. This shift is vital for any brand that wants to grow. Consequently, the payment journey is no longer just a task; it is an experience.

Why Old Checkout Systems Fail

Static forms are the biggest enemy of sales because most shops show the same fields to everyone. Consequently, many people leave their carts empty. This is because the process feels long and hard. Generative ai solves this by making every page unique for the user. For instance, it knows if you are on a phone or a laptop. Furthermore, it predicts which payment method you prefer. Therefore, you spend less time typing and more time enjoying your purchase. In short, it removes the friction that kills sales.

Real-Time Help with Generative AI

Shopping can sometimes feel confusing, especially when you have questions about shipping or taxes. Standard help pages are often hard to find. However, generative ai adds a smart assistant to the page to guide you. This bot answers your questions in seconds. Because the bot knows your cart, it gives perfect advice. This builds trust and keeps you moving forward. In addition, it makes sure you never feel alone while shopping.

Moreover, these bots can offer special deals at the perfect moment. If you hesitate, the generative ai might give you a small discount to help you decide. As a result, shoppers feel valued and safe. It is not just a tool; it is a digital guide. Because of these benefits, top brands are moving to AI today. Therefore, the checkout flow becomes a conversation instead of a form.

Safer and Faster Payments

Security is the most important part of any sale because hackers are always looking for ways to steal data. Luckily, generative ai is great at spotting fraud by looking at millions of data points in real-time. If it sees something odd, it stops the threat fast. This keeps your money and data very safe. Because the generative ai is so smart, it rarely blocks real customers. Thus, it makes payment security much stronger for everyone.

Additionally, it helps with filling out forms by guessing your address with high accuracy. This reduces errors and saves time for the customer. When you use it, the checkout flow feels like magic. You just click and go. Therefore, the risk of a mistake is very low. This is the future of generative ai in the payment world. Finally, this technology ensures that safety does not come at the cost of speed.

The Big Future of Generative AI

We are only at the start of this change. Soon, every store will use generative ai to talk to us. It will know our size, our style, and our budget. This means we will see fewer ads we do not like. Instead, we get a tailored world of products. It makes every transaction feel human. It is the best way to shop in 2026. If you want to stay ahead, you must use generative ai now. In conclusion, the personalized payment journey is the new standard for global trade.

Frequently Asked Questions

1. Is generative ai safe for my credit card?

Yes, it improves security by spotting fraud much faster than older systems.

2. Does generative ai make my phone slow?

No, most of the work happens on fast servers, so your phone stays quick.

3. Why do stores need generative ai?

It helps them sell more by making the checkout process easy and personal for everyone.

4. Can generative ai help with returns?

Yes, it can guide you through the return process and answer policy questions instantly.

5. Will all stores use generative ai soon?

Yes, it is becoming the global standard for all top e-commerce websites.

The world of money is changing very fast. Many nations want to build their own systems, free from old ways. However, the path to a new global order is complex and full of big choices. Because of this, staying ahead means looking toward fresh tech and strong partnerships. Specifically, BRICS and digital payments are now a key topic for leaders worldwide. This offers a clear map for new trade, faster work, and a very modern way to pay. This move is not just about tools for a few banks. In fact, it is a smart strategy for many lands to gain more power. Consequently, understanding this impact helps you see why it matters.

The Current Landscape: Visa and Mastercard’s Dominance

For a long time, two names have ruled how the world pays. Visa and Mastercard have built vast networks across the globe. They process billions of deals every single day with ease. These systems are reliable and trusted by many people everywhere. However, this power also means control rests in just a few hands. Some nations worry about this strong hold on their money flows. They feel that vital services should not be tied to just one or two firms. Furthermore, geopolitical events can sometimes affect these global payment channels. This makes some countries very eager to find new ways to pay. Therefore, the search for an independent path grows stronger.

The BRICS Alliance: A Push for Economic Independence

BRICS is a group of five big nations: Brazil, Russia, India, China, and South Africa. These countries represent a huge part of the world’s people and wealth. They often work together to boost their trade and influence. A key goal for BRICS is to create more economic freedom for its members. They want to reduce their reliance on systems built and run by other blocs. This desire extends to how money moves between them. The idea of a shared payment system is very appealing. It would help them trade more easily without outside interference. Consequently, BRICS and digital payments are a natural fit for their goals. This alliance seeks to build a new financial backbone.

The Rise of Digital Payments and Central Bank Digital Currencies (CBDCs)

Digital payments are quickly changing how we use money. Apps on phones, online wallets, and instant transfers are common now. This shift makes it easier to imagine new global systems. A big part of this trend is the rise of Central Bank Digital Currencies (CBDCs). Many BRICS nations, like China and India, are actively working on their own CBDCs. These are digital forms of a country’s money, issued by its central bank. If BRICS countries can link their CBDCs, it would create a powerful new network. This would allow fast, cheap, and direct payments between their economies. Such a system could bypass older networks entirely. Thus, BRICS and digital payments could form a new standard.

Challenges to Building a Unified BRICS Payment System

Creating a brand new global payment system is not easy. First, there are many technical hurdles to overcome. Each country has its own rules, tech, and banking laws. Making these all work together perfectly takes huge effort. Furthermore, building trust among member states is vital. They must agree on how data is shared and how disputes are handled. There are also security concerns; any new system must be very safe from cyber-attacks. Finally, getting people and businesses to adopt a new method takes time. They are used to the ease of Visa and Mastercard. Despite these challenges, the motivation for a BRICS digital payment alternative is very high.

Potential Impact: A New Global Financial Order?

If BRICS succeeds in creating its own payment system, the impact could be huge. It would give these nations more control over their own money flows. They could reduce fees and speed up cross-border trade. It might also encourage other developing countries to join or adopt the system. This could lead to a more diverse and multi-polar global financial world. Visa and Mastercard would still be very important. However, they would face a serious new competitor. This competition could even push existing systems to innovate more. Consequently, BRICS and digital payments could reshape how we think about international finance. The shift could truly impact global power dynamics.

Conclusion: The Road Ahead

The idea of an alternative to Visa and Mastercard from the BRICS bloc is gaining traction. The rise of digital payments and CBDCs makes this vision more possible than ever. While big challenges remain, the desire for economic independence is a strong driving force. This development is worth watching closely. It could signal a major shift in how global money moves and who controls it. The future of international payments might be far more diverse than it is today.

FAQs

1 What is BRICS?

It’s a group of major emerging economies: Brazil, Russia, India, China, South Africa.

2 Why do BRICS nations want a new payment system?

They want more economic independence and less reliance on existing global payment networks.

3 What are CBDCs?

Central Bank Digital Currencies are digital forms of a country’s national money, issued by its central bank.

4 Could a BRICS system replace Visa/Mastercard?

It might not replace them entirely but could emerge as a significant alternative, especially for cross-border transactions among BRICS and allied nations.

5 What are the biggest challenges?

Technical integration, regulatory harmonization, security, and user adoption across diverse nations.

The world of money is changing very fast as we move into 2026. Therefore, many countries are now testing their own digital versions of cash. Truly, Central Bank Digital Currencies, or CBDC, are becoming a reality for millions of users. Consequently, everyone in the payment world is asking if this is a threat or a giant opportunity.

Some people feel that a search engine will soon show a world without private payment processors. But, the truth is much more complex and interesting for business owners. Always remember, every major shift in finance creates new ways to provide value. This ensures that those who adapt will find more success than those who stay the same. This approach requires a deep look at how digital money moves across borders. It helps you prepare for a future where cash might disappear entirely. It makes your financial strategy much more robust for the years ahead.

Phase 1: What Exactly Are CBDCs and How Do They Work?

First, let us look at what makes a CBDC different from the digital money we use today. Why are governments so interested in this new technology right now? Clearly, it is about giving the central bank more control and transparency over the money supply. Therefore, it is a direct digital claim on the central bank rather than a private bank.

Key Features of a Digital Currency

Here are several things that define a CBDC in the current market:

Direct Issuance: The money comes directly from the government or central bank.

Instant Settlement: Transactions happen in real time without waiting for clearing.

Low Costs: It aims to remove many of the fees found in traditional banking.

Programmability: This allows for smart contracts that trigger payments automatically.

Universal Access: It helps people without bank accounts join the digital economy.

Enhanced Security: Each digital unit is tracked to prevent fraud and theft.

Legal Tender: It must be accepted by law for all debts and taxes.

Truly, this technology could change how every search engine tracks financial data. But, it also brings up big questions about user privacy and data safety. This keeps the debate between speed and privacy very active in 2026.

Phase 2: Why Gateways Might See CBDCs as a Threat

So, why are some payment gateways feeling nervous about these digital coins? Truly, a government-backed system could bypass the need for many private middlemen. Consequently, the traditional fees that gateways charge might be at risk. It acts as a direct competitor to the services that have existed for decades.

Risks Facing Traditional Payment Gateways

Here is how CBDCs could challenge the existing payment model:

Fee Compression: If government digital money is free to use, gateways cannot charge high fees.

Direct Wallets: Users might pay merchants directly from a government app.

Faster Rails: Central banks might build their own fast networks that skip private ones.

Reduced Volume: Traditional credit card use might drop as people switch to CBDCs.

Data Control: Governments might keep the transaction data that gateways used to own.

Strict Rules: New laws might favor the state system over private companies.

Global Shifts: International CBDC links could make cross-border gateways less vital.

Furthermore, this could hurt the search engine ranking of companies that rely on old tech. It makes it harder for slow-moving businesses to stay profitable. This ensures that only the most efficient gateways will survive the next five years. It creates a very competitive environment for everyone in the finance space.

Phase 3: The Massive Opportunity for Smart Gateways

The third phase looks at why CBDCs might actually be a good thing for the industry. Clearly, new technology always creates new needs for the average user. Therefore, smart gateways can act as the vital bridge between the state and the people.

How Gateways Can Thrive with Digital Currency

Firstly, gateways can provide a better user experience. Government apps are often very simple and hard to use for complex tasks. Secondly, they can offer advanced fraud protection. While CBDCs are secure, hackers will always try to find new ways to steal.

Furthermore, gateways can manage the mix of different currencies. Most people will still use credit cards, crypto, and CBDCs at the same time. Also, they can provide better reporting for merchants. Business owners need deep data that a basic government wallet might not show. Lastly, they can help with international trade. Linking different national CBDCs together is a task that gateways are perfect for. Truly, your search engine authority grows when you offer solutions to these new problems. It allows you to become a trusted advisor in a confusing digital landscape. This is the key to winning in the new financial era.

Phase 4: Preparing for the 2026 Financial Shift

The fourth phase is about the steps you must take to be ready for this change. Clearly, you cannot wait for the rules to be fully written before you act. Therefore, you should start integrating digital currency options into your systems now.

Steps to Future-Proof Your Payment Strategy

Firstly, monitor the pilot programs in major countries. Watching how China or Europe handles their digital coins gives you a head start. Secondly, invest in blockchain and ledger technology. These are the foundations that most CBDCs are built upon.

Furthermore, talk to your customers about their needs. See if they are interested in using digital versions of their national currency. Also, stay active in the regulatory discussion. Helping shape the laws can protect your business from bad rules later. Lastly, improve your site speed and mobile features. A fast site helps your search engine ranking and makes digital payments smoother. Truly, being an early adopter is the best way to secure your future. It shows the world that your brand is a pioneer in the digital space. This leads to more trust and higher traffic over the long term.

Best Practices: Balancing Innovation and Safety

Managing digital money requires a very careful and balanced approach. It needs a focus on both new features and old-fashioned security. Clearly, the trust of your users is the most valuable asset you have. Therefore, follow these simple habits to maintain your lead in 2026.

Strategies for Long-Term Digital Currency Success

Firstly, always prioritize the privacy of your users. Even with a state-backed coin, people want to know their data is safe with you. Secondly, keep your systems simple and easy to understand. New financial tools can be very scary for the average person.

Furthermore, update your content frequently. Use your blog to explain how these changes help your customers save money. Also, build partnerships with banks and tech firms. No company can handle the shift to CBDCs entirely on its own. Lastly, track your search engine performance closely. Make sure people can find your guides when they search for digital money help. Truly, a helpful and modern gateway will always be in high demand. It turns a potential threat into a powerful tool for growth. This ensures your brand stays strong regardless of what the central banks do.

Frequently Asked Questions (FAQs)

Q1: Is a CBDC the same as Bitcoin?

No, Bitcoin is a private crypto currency that is not backed by any state. A CBDC is a digital version of a country’s official money and is controlled by the government.

Q2: Will CBDCs help my search engine ranking?

Writing about CBDCs can help your ranking if you provide expert info that users are searching for. It shows you are an authority on the latest financial trends.

Q3: When will CBDCs become common for everyone?

Many countries are already in the pilot phase in 2025. It is likely that CBDCs will be a common payment option in major markets by the end of 2026.

Q4: Can I use a CBDC for international payments?

Yes, one of the main goals of CBDCs is to make international payments faster and cheaper. Gateways will play a major role in linking these different systems.

Q5: Will my private bank account disappear?

No, CBDCs are expected to work alongside traditional bank accounts. Most experts believe we will continue to use a mix of both systems for a long time.